1Q 2025 URA Private Residential Report: Private Home Prices Display More Moderate Pace of Growth

- By Stanley Lim

- 5 mins read

- Private Residential (Non-Landed)

- 2 Apr 2025

Figures are based off the official flash estimates for URA quarterly statistics, released on 1 April 2025.

SINGAPORE, 01 April 2025 – As reflected in the latest flash estimates released by URA, the All-Residential Property Price Index exhibited a modest increase of 0.6% quarter-on-quarter (q-o-q) in 1Q 2025, while the total transaction volume of private homes inched down 15.3% over the same timeframe.

Favourable Economic Conditions Fuel Homebuying Activity

Recent months have seen the return of homebuyers to the new launch market, supported by favourable economic conditions, as reflected across various indicators and moderated interest rates.

On the whole, Singapore put up a better-than-expected financial showing last year. According to the Ministry of Trade and Industry, the national economy expanded by 4.4% in 2024, more than double of the 1.8% growth recorded for 2023. That said, while the market remains cautiously optimistic on growth prospects amid the escalating trade tension.

Singapore’s property market remains propped up by domestic demand. Good jobs, rising income and low unemployment rates have made private homes more accessible for Singaporeans. Moreover, the rising HDB resale prices will continue to help pave the way for Singaporeans to upgrade to private homes.

Moreover, interest rates had also begun tapering in the latter half of 2024, following a trio of rate cuts by the U.S. Federal Reserve (Fed) during September, November and December. This brought the Fed’s target interest rate range down to 4.25% to 4.50%, lowering borrowing costs and raising consumer optimism. Locally, core inflation rates also eased to an average of 2.7% last year, down from 4.2% in 2023.

While market conditions are encouraging and favourable for home buyers, some buyers may remain cautiously optimistic amid geopolitical headwinds. Singapore’s position as a key Asia-Pacific hub could prove advantageous, as its neutrality and strategic location may continue to attract interest even amid escalating trade tensions and the risk of a global economic slowdown.

All-Residential Private Home Prices and Transactions

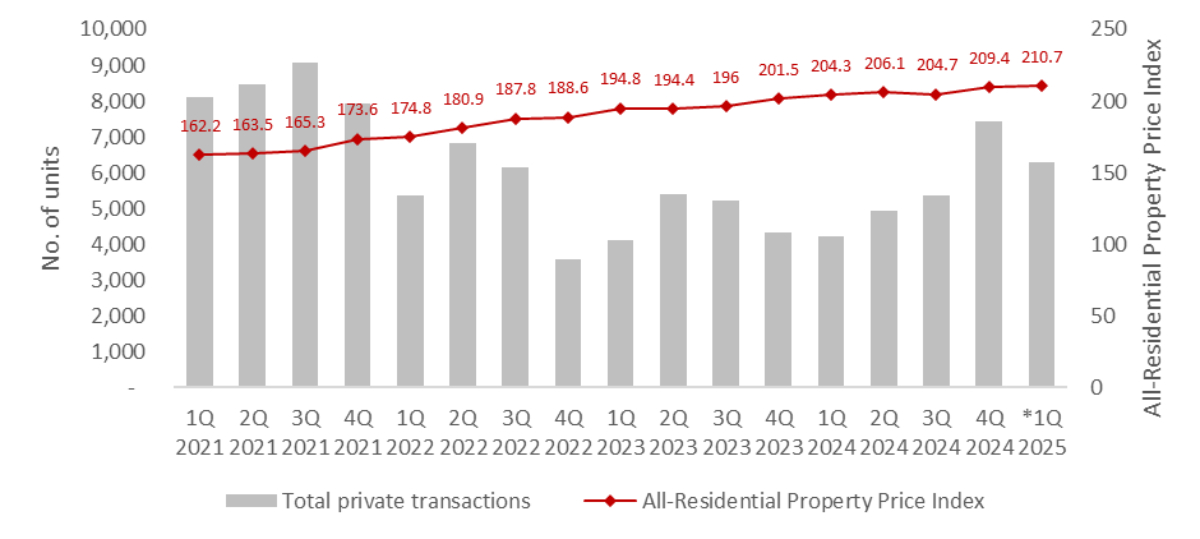

As reflected in the latest flash estimate figures released by URA for 1Q 2025, overall private home prices rose moderately on the quarter, pushed further upwards by the solid performances of new launches debuting in the opening months of the year. In relation, the All-Residential Property Price Index was observed to have risen moderately by 0.6% quarter-on-quarter (q-o-q), carrying forward the upwards momentum demonstrated in 4Q 2024 when it rose 2.3% q-o-q.

However, despite the strong start to the year observed in the new sale market, overall transaction numbers of private homes exhibited a decline, dragged down by a downtick in the number of secondary market transactions. In 1Q 2025, the total transaction volume of private homes (up to mid-March) was 6,299 units, which is 15.3% less than the 7,433 units sold in 4Q 2024.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

Source: URA, ERA Research and Market Intelligence (*Based on flash estimates.)

Also, according to flash estimates released by the Urban Redevelopment Authority (URA), the non-landed RCR property index showed the most pronounced growth among regional sub-markets, with a moderate yet notable 1.0% q-o-q increase.

Similarly, the non-landed CCR and OCR property price index saw 0.6% and 0.3% q-o-q growth. These increases were largely driven by higher price benchmarks achieved at recent new home launches across all market segments.

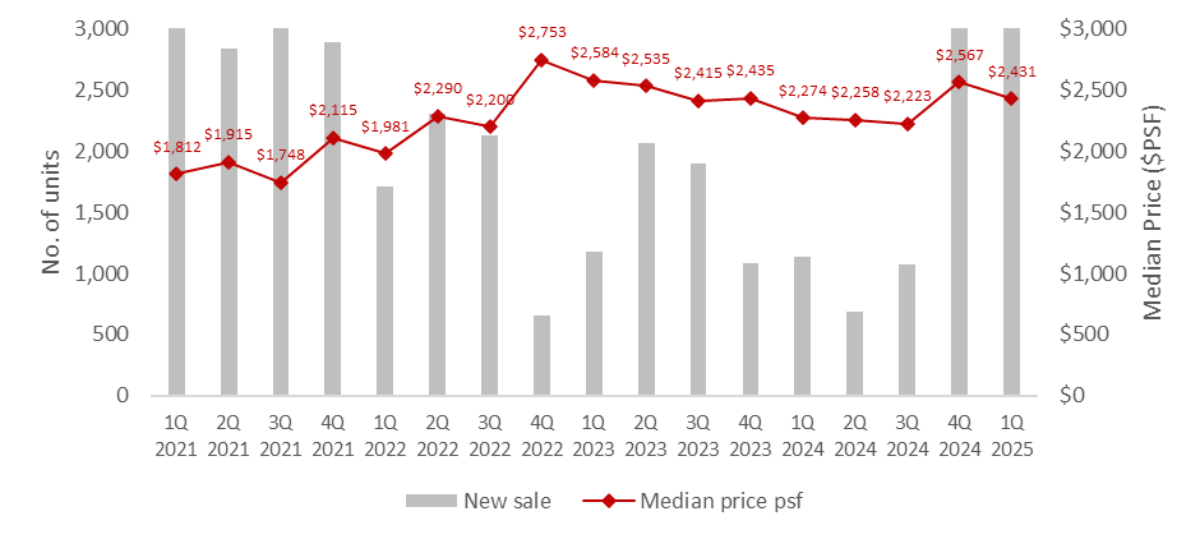

New Sale (Non-Landed Homes, Excluding ECs)

The private residential market maintained its upward momentum in 1Q 2025, with primary sales continuing their strong performance from the previous quarter. According to caveats as of 26 March 2025, new sale transactions in 1Q 2025 dipped 3.1% quarter-on-quarter (q-o-q) to 3,268 units per URA caveats (reflecting a higher base in 4Q 2024). 1Q 2025’s sales volume remained above all quarterly new home sales recorded between 4Q 2021 and 3Q 2024. This resilience was driven by several blockbuster launches taking place in either underserved locations lacking in new non-landed private residential supply or in established towns with strong amenities and transport links.

In January 2025, The Orie, the first launch in Toa Payoh since 2015, was launched and achieved outstanding performance. During its launch weekend, it moved 668 units (75%) at a median price of $2,704 psf, setting a new benchmark for the RCR.

February saw the launch of Parktown Residences, an integrated mega-development of over 1,193 units at Tampines, and ELTA, a 501-unit project at Clementi Ave 1. They sold 1,041 (87%) and 326 units (65%) during their launch weekend respectively.

Lentor Central Residences, in the new Lentor Hills cluster, is another popular up-and-coming housing estate. Despite being the sixth launch, its performance was still stellar. 445 units (93%) was snapped up at launch.

Stellar sales performance and buzz from the newly launched projects have also created interest in existing projects. Buyers who were unsuccessful in getting their desired unit may look towards other similar-priced projects. Thus, Pinetree Hill, Hillock Green and SORA also saw an uplift in units sold. One Bernam, one of the few existing launches located in the Downtown Core, was fully sold this quarter.

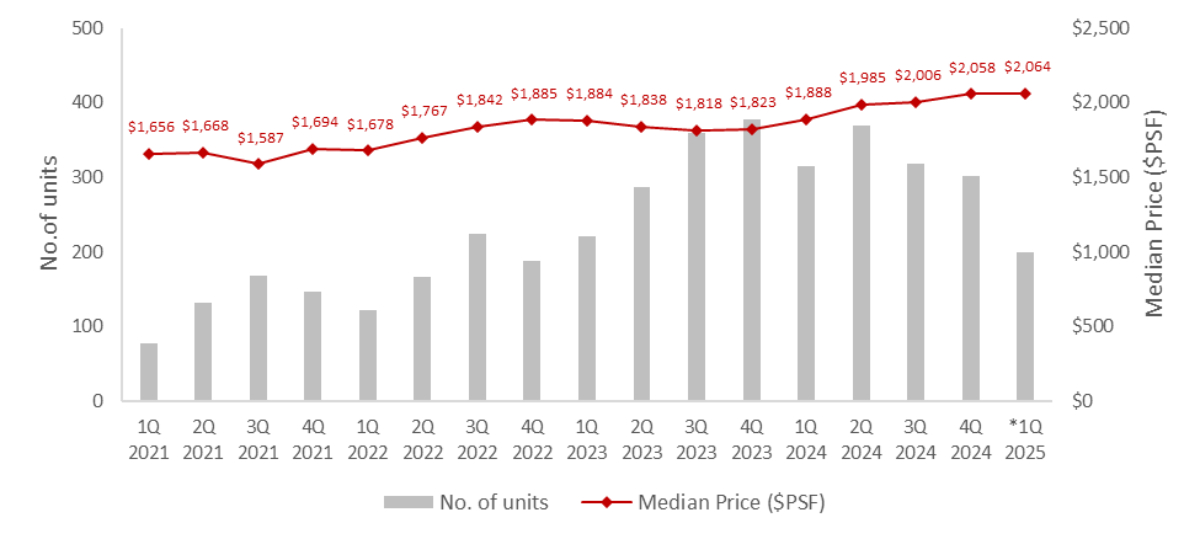

Chart 2: New Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 Mar 2025, ERA Research and Market Intelligence

Table 1: Top 10 Best-Selling Projects in 1Q 2025

Source: URA, ERAPro as of 26 Mar 2025, ERA Research and Market Intelligence

Executive Condominium

1Q 2025 saw a single EC launch with Aurelle of Tampines’s debut in March 2025 – the project saw 90% of its 760 units sold at an average price of $1,766 psf on launch day. According to caveat data, this resulted in a 54.7% q-o-q increase in EC sales by developers who sold 817 units in total over 1Q 2025. Notably, Aurelle of Tampines is also just 200m away from Parktown Residences, offering buyers an alternative option.

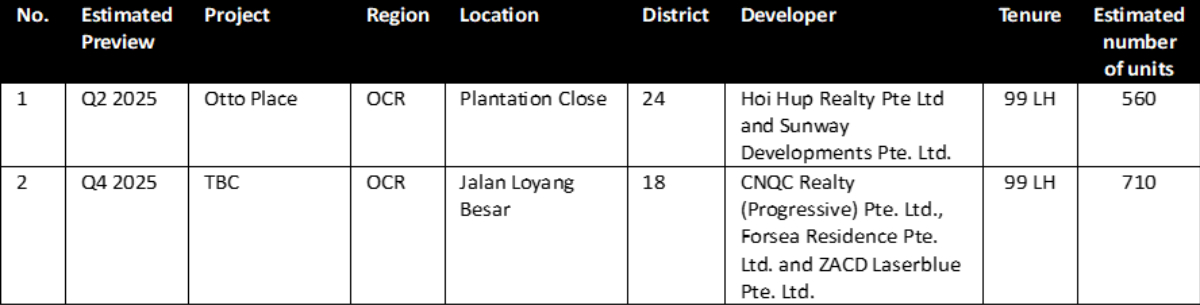

Following Aurelle of Tampines’s strong performance, the current supply of new EC homes is fairly limited. As of 26 March 2025, there are fewer than 130 units available across five projects island wide. Though there are another two projects at Plantation Close (Otto Place) and Jalan Loyang Besar slated to be launched this year, this incoming supply might still fall short of demand.

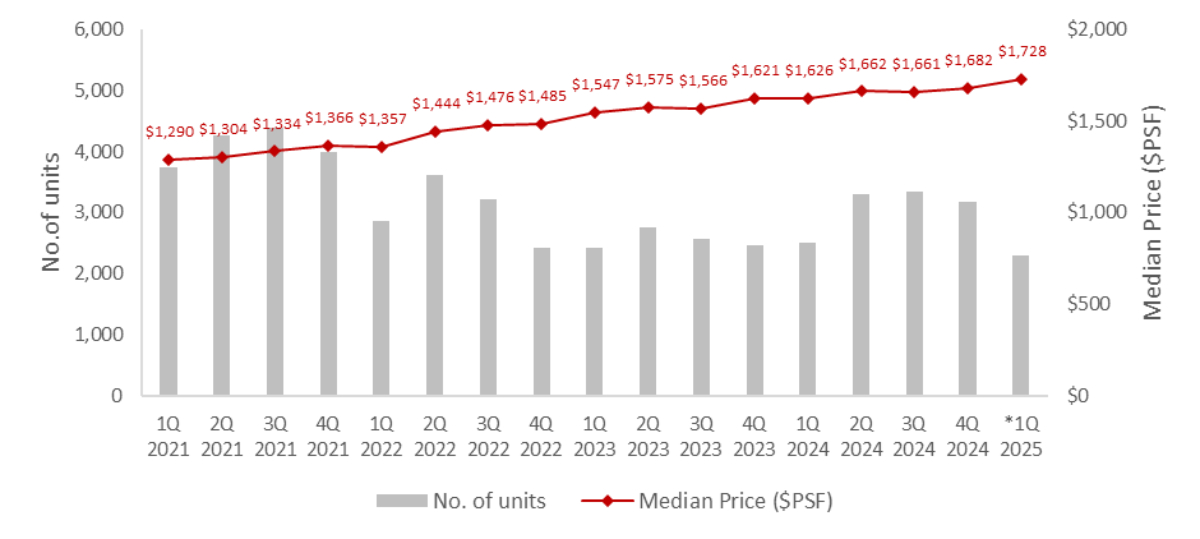

Resale and Sub-Sale (Non-Landed Homes, Excluding EC)

Based on URA caveat as of 26 March 2025, resale transactions accounted for 39.8% of all non-landed private home sales (excluding ECs) in 1Q 2025, corresponding to a total of 2,294 resale units changing hands over the quarter. Compared to the last period, which saw 3,173 resale transactions in 4Q 2024, this represents a 27.7% q-o-q decline in the number of resale units sold.

Chart 3: Resale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 Mar 2025, ERA Research and Market Intelligence

This finding also marks a continuation of 4Q 2024’s decline in resale transactions for non-landed private homes (excluding ECs), whereby a 4.9% q-o-q downtick was observed last quarter.

These successive downticks in resale volume could plausibly be due to competition posed by the new sale market, as well as the tapering number of private home completions. At present, URA’s full-year estimates for completions of private homes (excluding ECs) stand at 5,846 units for 2025, which is notably lower than the equivalent of 8,460 units for 2024.

Conversely, this relative scarcity of new completions could have fuelled price growth in the resale market, as available inventory diminishes. This resulting upwards price pressure dovetails with the slight 2.7% q-o-q uptick in median unit prices observed for 1Q 2025.

Chart 4: Sub-Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 March 2025, ERA Research and Market Intelligence

Sub-sales, on the other hand, made up 3.5% of all non-landed private home sales (excluding ECs) in the quarter, clocking a total of 199 transactions based on available caveat data. On the quarter, this represents a 34.1% q-o-q decline from the 302 transactions recorded for 4Q 2024. Median unit prices in the sub-sale market also edged up by 0.4% q-o-q, reaching $2,064 psf.

These movements in the sub-sale market were likely shaped by the same factors influencing resale trends, namely the robust uptake of new launches and declining secondary stock.

Market Outlook

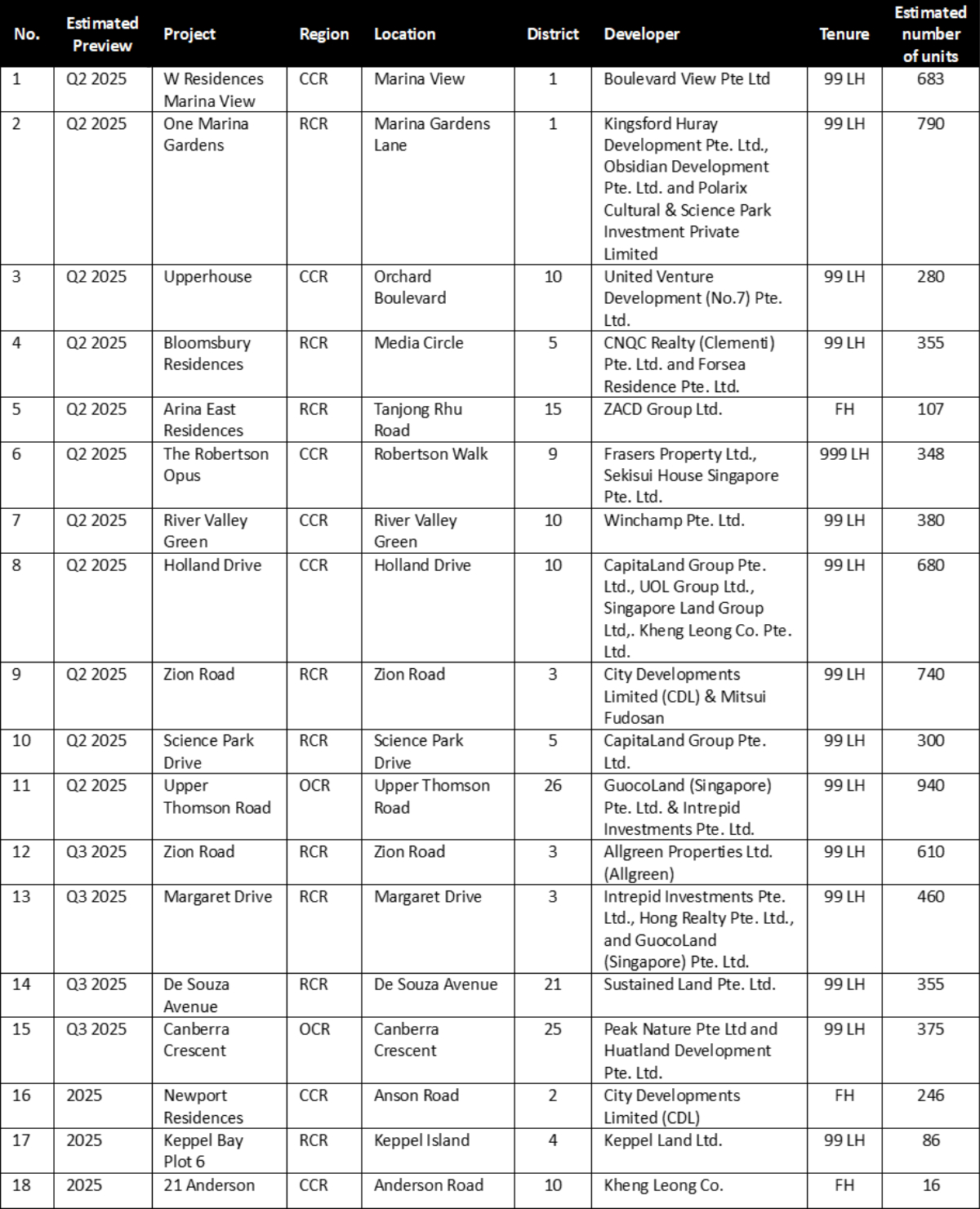

The coming months will likely see launches in the CCR and RCR, such as One Marina Gardens, Bloomsbury Residences (in Media Circle) and Upperhouse in Orchard Boulevard. One Marina Gardens and Bloomsbury Residences will appeal to astute buyers or investors who take a long-term view on the market as these locations undergo masterplan transformation. Separately, Upperhouse at Orchard Boulevard aims to attract well-heeled, lifestyle-driven buyers, with its location beside the Orchard Boulevard MRT station serving as an added advantage.

These buyers tend to take a more deliberate approach when evaluating investment opportunities, so sales for these projects may progress at a more measured pace, reflective of the discerning nature of these buyers.

Building on the recent momentum in new home sales, ERA has revised our earlier projection of 7,000 and 8,000 new home sales to 8,500–9,500 units for the whole of 2025.. In conjunction, sub-sale and resale transactions are also expected to reach between 1,100 to 1,300 units and 14,000 to 15,000 units respectively by the close of 2025.

Table 2: Upcoming launches in 2025

Source: ERA Project Marketing

Executive Condominium

Source: ERA Project Marketing

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.