99-to-1 Shareholding: Legit Arrangement or Illegal ABSD Loophole? Issues Explained!

- By Stanley Lim

- 4 mins read

- Property News

- 8 Jul 2024

If you’ve been paying notice to the latest news about Singapore’s property market, you’d likely have seen headlines such as “IRAS to claw back S$60 million from buyers who used ’99-to-1’ loophole to avoid ABSD” and “Why using ’99-to-1’ is illegal in avoiding Additional Buyer’s Stamp Duty” making the rounds recently.

Naturally, these announcements have generated much buzz online, while also drawing much attention to the 99-to-1 arrangement, its legality, as well as the ongoing crackdown on Additional Buyer’s Stamp Duty (ABSD) tax avoidance by the Inland Revenue Authority of Singapore (IRAS).

But what exactly does this all mean for private homebuyers locally?

To shed light on the issue, we had Eugene Lim (Key Executive Officer) and Nicholas Poa (Senior Vice President, Legal and Compliance) explain more, as well as answer the burning question on everyone’s mind: “What exactly are the situations where IRAS has clawed back ABSD for properties that are held in a 99-to-1 shareholding arrangement?”

Can you explain what 99-to-1 shareholding arrangements are?

Eugene (E): So, before we dive into exactly what 99-to-1 shareholding arrangements are, we must first talk about property co-ownership in Singapore.

Essentially, there are two ways that property can be held. The first is joint tenancy, whereby both parties co-own a property equally – there are no distinct shares. Joint tenancy is common amongst parties who are family or between husbands and wives.

The other form of co-ownership is tenancy-in-common. Under such arrangements, each co-owner holds a prescribed number of shares in the property. In a straightforward scenario, this proportion can be equal, whereby Party A holds 50% of the property and B holds the other 50%.

However, it’s up to the owners to decide how they’d want to split the shares in a tenancy-in-common arrangement, whether it’s by a 50:50 ratio, or 99:1.

Nicholas (N): So, the bottom line that we want to highlight here is that co-owning a property in any proportion – even in a 99-to-1 structure – under tenancy-in-common isn’t illegal.

You can think of tenancy-in-common as being like a commercial joint venture, but for residential property. Each owner holds a proportionate share, often based on their financial contribution.

It’s just like partners in a business where each person’s share is separate and distinct, and they are each entitled to make independent decisions about their assets.

For example, under tenancy-in-common, each co-owner is free to pass on their share of the property to chosen beneficiaries. This is unlike joint tenancy where property ownership automatically vests in the surviving co-owner when one of them passes away.

If 99-to-1 shareholding arrangements aren’t illegal, why then did the authorities classify some cases as tax avoidance?

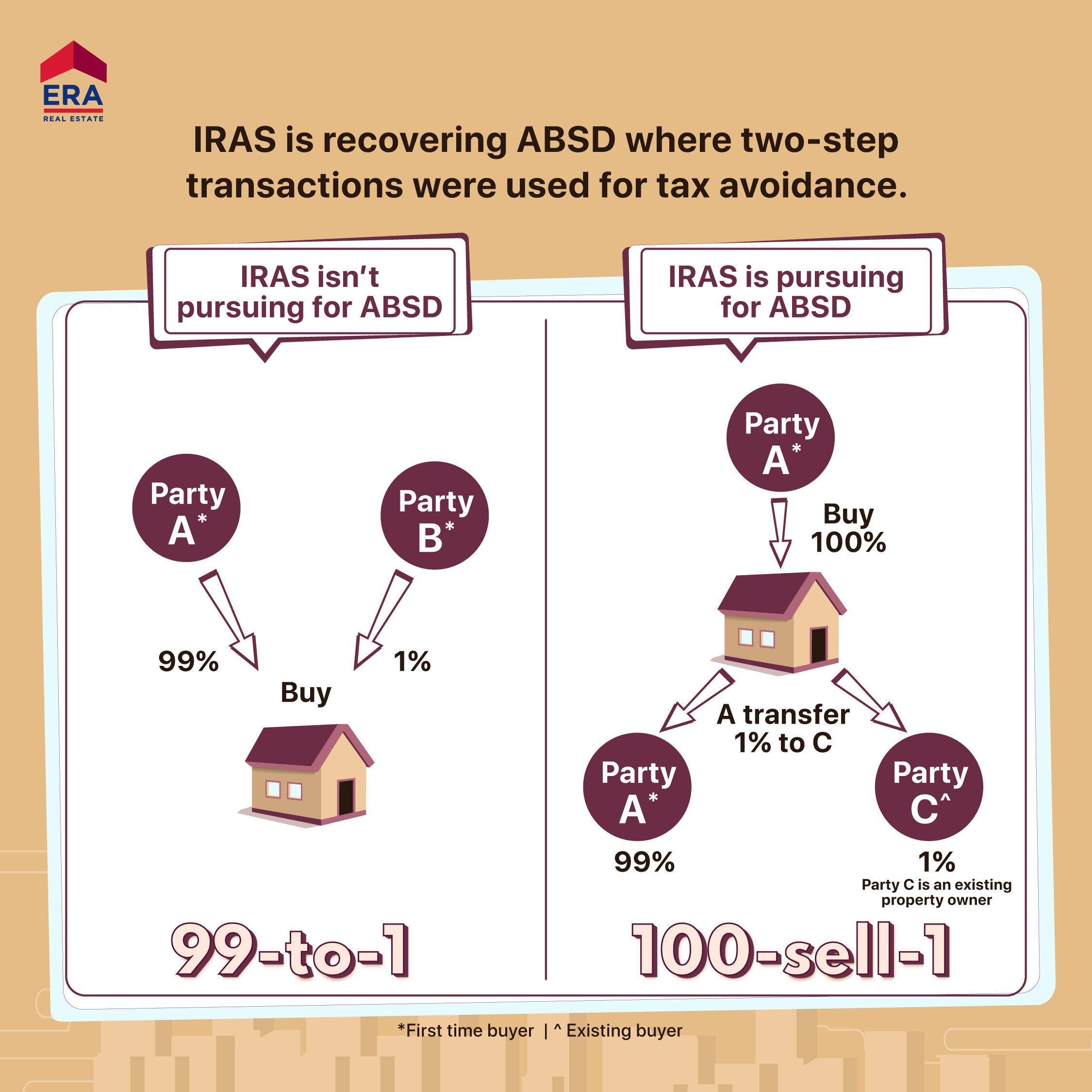

N: The type of cases that IRAS has cracked down on are ‘two-step’ transactions that are structured to avoid ABSD.

‘Two-step’ transactions work by splitting up a single purchase into two (or more) steps to reduce the amount of ABSD paid, and they involve at least one co-owner who already owns and/or has a stake in another residential property.

For instance, instead of purchasing a new house as co-owners from the outset, Party A buys 100% of the property as a first-timer, after which they will sell 1% of their share to Party B – who is an existing property owner – within a very short period.

In doing so, Party B avoids paying ABSD on the full purchase price of the new property. Instead, they pay ABSD only on the 1% share which was transferred.

E: That’s exactly how the ABSD loophole works. Considering this explanation, perhaps it’s more accurate to describe such two-step purchases as ‘100-sell-1,’ as opposed to the ’99-to-1′ phrase often used by the media to refer to schemes that exploit the ABSD loophole.

That’s because ‘100-sell-1’ more correctly illustrates the exact method that exploits the ABSD loophole, whereas ’99-to-1’ is potentially misleading since it conveys the wrong impression that all 99-to-1 holding arrangements are illegitimate.

Are there any legally valid uses of 99-to-1 shareholding arrangements?

N: Broadly speaking, there are three legitimate commercial reasons for holding a property in a designated ownership split, regardless by a 99:1 proportion or any other ratio.

The first reason would be to ensure fairness when a property is co-owned under tenancy-in-common from the start, allowing each co-owner to own a share of the property proportionate to the amount that they invested.

Second, would be to maximise loan eligibility. Using the example of Party A and B again, if Party A were to purchase a property by themselves, their loan eligibility will be evaluated solely based on Party A’s income.

However, with co-ownership, both owners’ incomes will be assessed, allowing them to secure a bigger loan while also reducing the amount of cash needed for their downpayment.

Finally, the third legitimate use of co-ownership is for future planning. If co-owners – such as married couples – wish to expand their property portfolio, they’ll be able to exit their first property more easily with a 99:1 arrangement.

This exit process is sometimes referred to as decoupling, and it usually starts off when the co-owner with a minority stake in the property transfers his share to the majority co-owner. As a result, the minority co-owner is no longer a property owner at the point that they purchase a new property, allowing them to be treated similarly as a first-time homebuyer.

I’d also want to highlight that even though decoupling makes use of the 99-to-1 shareholding structure, it’s also quite different from the ‘100-sell-1′ scheme.

For decoupling, both co-buyers don’t own any other property when purchasing their first home in a shareholding structure. In other words, they won’t have any ABSD obligations in the first place.

Furthermore, decoupling involves purchasing a property jointly with a predetermined shareholding structure from the beginning, meaning that there isn’t a second step where a minority stake is sold soon after the purchase.

Considering the recent scrutiny by IRAS, how should homebuyers approach 99-to-1 shareholding arrangements going forward?

N: It goes without saying, but homebuyers should exercise extreme caution before engaging in any 100-sell-1 arrangements going forward.

As of May 2024, the Government has made its stance clear on disregarding two-step transactions with 99-to-1 ownership structures as it will be clawing back approximately S$60 million from cases that constitute tax avoidance.

Furthermore, IRAS has also announced that it will be implementing a 50 per cent surcharge that’ll be applied on the payable ABSD amount.

E: Hence, if you’re considering buying a property using any shareholding structures, it’s important that you must consult with a qualified tax advisor or legal professional before you proceed with the transaction. Doing so will give you a better understanding of ABSD laws, and possibly save you from potential pitfalls.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.