2024 Landed Report: Strong Upgrader Demand Drives Landed Home Transaction, Trend Expected to Continue in 2025

- By Wong Shanting

- 2 mins read

- Private Residential (Landed)

- 26 Feb 2025

2024 saw a rebound in landed home transactions amid more moderate price growth. The rebound in interest was largely driven by rising non-landed home prices, enabling homeowners to sell their properties at higher prices and reduce the capital outlay needed to transition to landed homes.

Landed Property Price Index and Transactions

The Landed Property Price Index recorded its slowest year-on-year (y-o-y) growth of 0.9% in 2024 and is showing signs of stabilising. This marked a significant slowdown compared to the period of rapid price growth seen between 2021 and 2023.

Amid the more moderate price growth, the market saw a rebound in landed home transactions. Landed transactions rose 31.2% y-o-y to 1,687 units in 2024, compared to 1,286 units sold in 2023.

Chart 1: Landed Property Price Index and Transactions

![]()

Source: URA, ERA Research and Market Intelligence

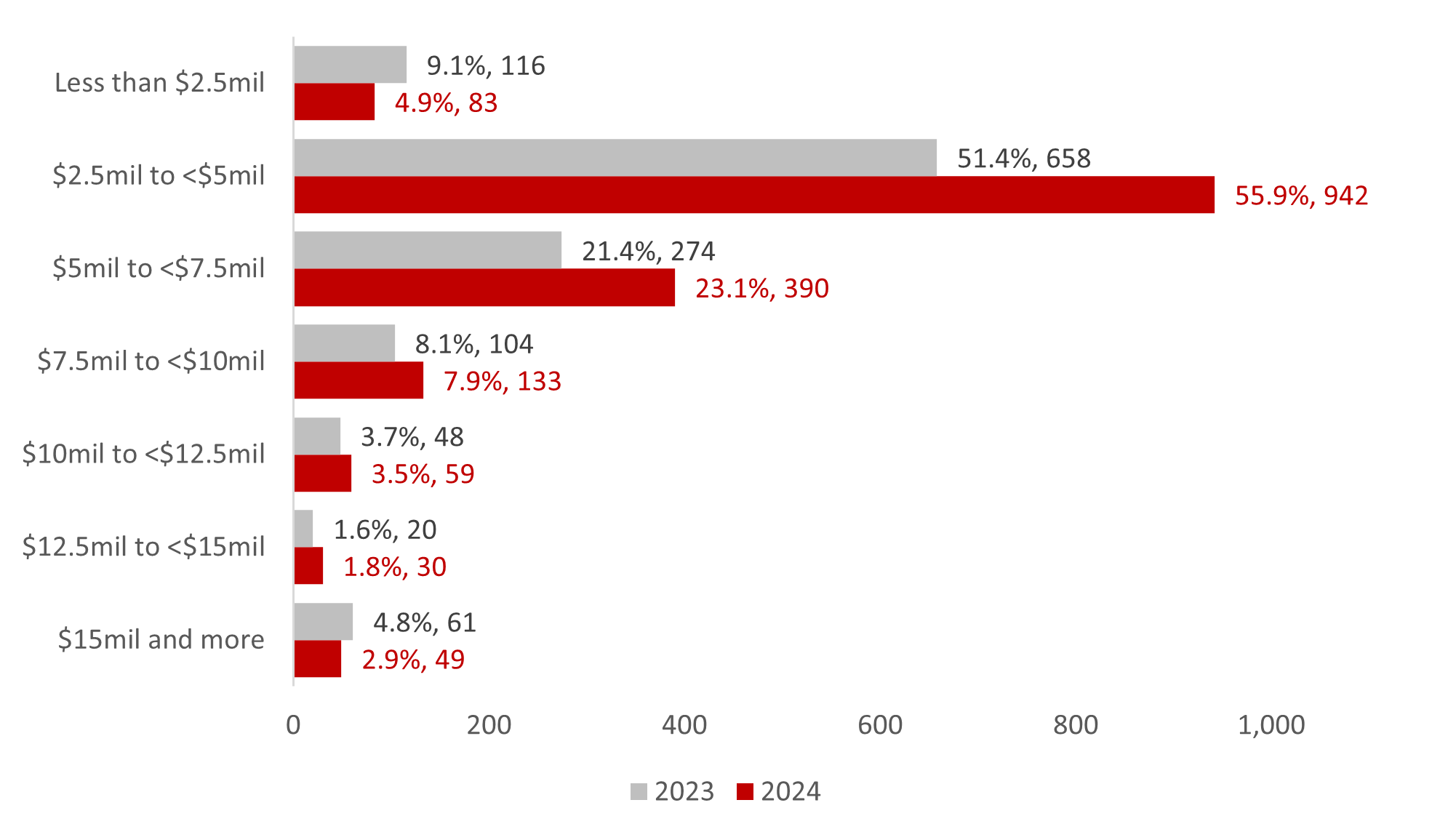

Price quantum

The majority of landed homes sold in 2024 continued to fall within the $2.5mil to $5mil price tag. At least 942 landed homes were sold within the $2.5mil to $5mil price compared to 658 in 2023.

This could be attributed to several reasons. Firstly, landed homes in this price bracket had comparable quantums to non-landed homes, prompting more buyers to make the leap to landed homes instead. Secondly, with the pickup in resale home transactions in 2024, more owners were able to sell their non-landed properties for higher prices and reduce the capital outlay for one to transition to landed homes.

However, with rising prices, a total of 390 landed homes were transacted between the $5mil and $7.5mil price tag in 2024 compared to 274 units in 2023.

Chart 2: Price Quantum 2023 versus 2024

Source: URA, ERA Research and Market Intelligence

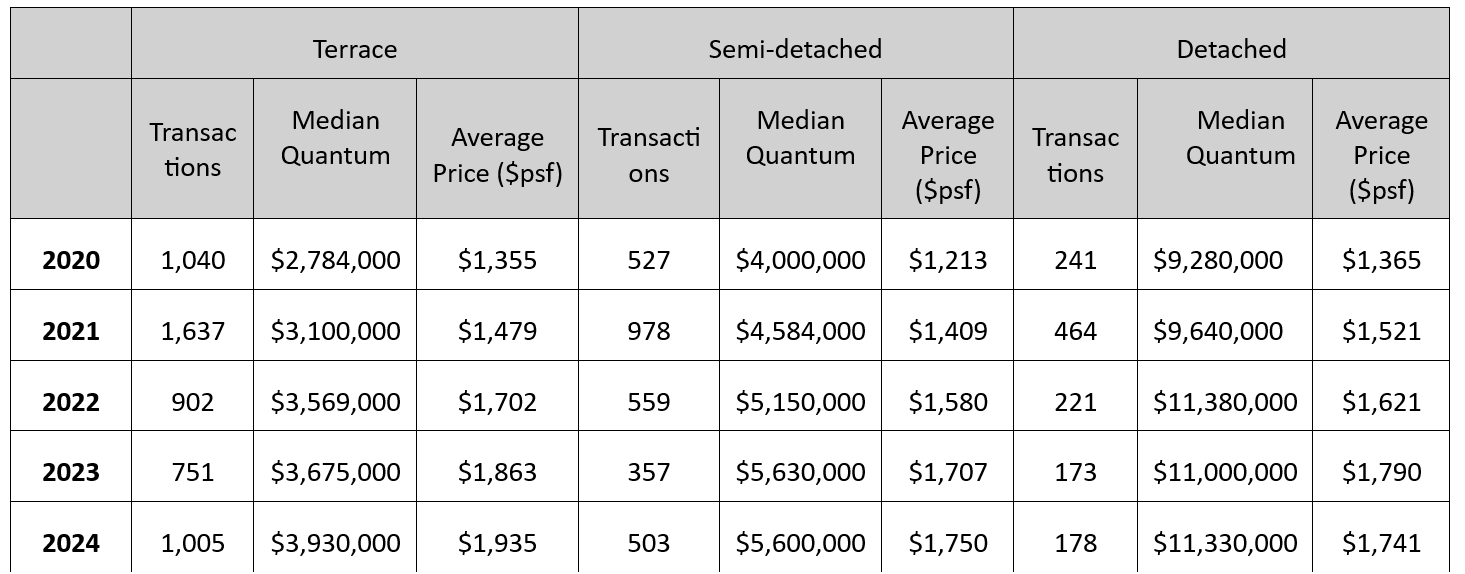

Type of properties

Compared to 2023, more terrace and semi-detached homes were sold in 2024 amid a slower pace of price growth. Terrace and semi-detached homes saw price growth of 3.9% and 2.5% y-o-y, respectively. This is in contrast with the 9.5% and 8.5% year-on-year growth recorded in 2023.

Buoyed by demand, terrace homes saw the steepest growth in median prices growing from $3.675 mil in 2023 to $3.930 mil in 2024. Comparatively, semi-detached home and detached homes saw median prices remaining similar to the previous year.

Table 1: Transaction Volume and Average Price by Landed Property Type

Purchasers address indicator

In conclusion

Recent interest rate cuts and a more positive economic outlook have driven brisk sales in Singapore’s residential property market, with one of the early beneficiaries being the landed segment.

Landed homes saw increased transaction volumes in 2024 and this trend is expected to persist this year, primarily driven by upgrader activity by non-landed property owners.

Despite ongoing global headwinds, ERA remains cautiously optimistic about the landed home segment which is potentially supported by more upgrader activities in 2025.

Assuming stable macroeconomic conditions and no unforeseen negative shocks, ERA expects the landed property market to gain momentum in 2025, with a projected year-on-year price growth of 3-5% and an estimated 1,800 to 2,000 landed transactions.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.