1Q 2025 HDB Quarterly Report: HDB Prices Continue to Grow Despite Lower Demand

- By Ethan Hariyono

- 3 mins read

- HDB

- 2 Apr 2025

Figures are based off the official flash estimates for HDB/URA quarterly statistics, released on 1 April 2025.

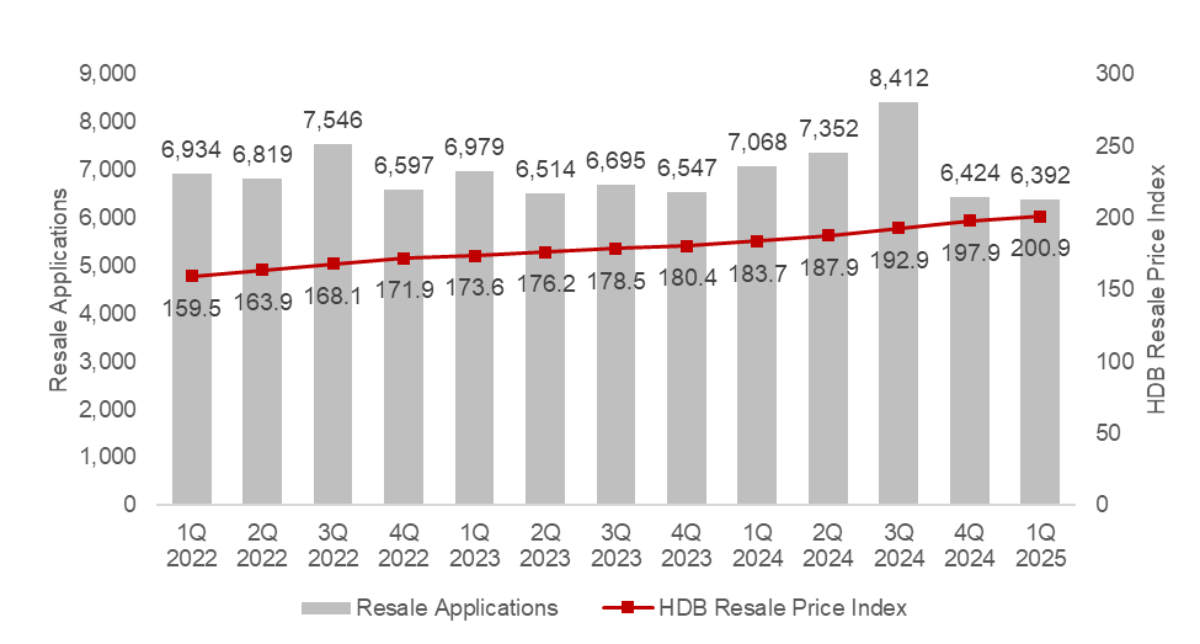

According to the Housing and Development Board (HDB)’s flash estimates, the HDB RPI rose to 200.9, a 1.5% increase quarter-on-quarter (q-o-q) in 1Q 2025.

This is the 20th consecutive quarter of growth of the RPI, which is on track to fall in line with ERA’s forecast of 3-6% annual price growth by the end of 2024.

Chart 1: HDB RPI vs Number of Transactions

Source: HDB as of 27 March 2025, ERA Research and Market Intelligence

Transaction Volume Down Amidst Seasonal Lull

There were a reported 6,392 HDB resale transactions recorded in 1Q 2025. This was a 7.7% decline y-o-y.

The lower transaction volume witnessed in the quarter can be attributed to the seasonal lull and the bumper crop of over 10,000 Build-to-Order (BTO) and Sale of Balance Flats (SBF) offered through an exercise in February. With these many BTO and SBF flats on offer, buyer’s eyes may have been pried away from the HDB resale market.

Compared to 4Q 2025, there were more 3-room and 4-room flats transacted in 1Q 2025, while the number of executive flats sold continues to decline.

February saw the first BTO launch of the year, which offered highlights such as a pair of Plus flat projects in Queenstown, as well as affordable projects in Woodlands and Yishun (Chencharu) – with one of the latter mentioned projects being an integrated housing development, with a bus interchange and commercial segment.

These SBF flats feature shorter waiting times compared to BTO flats. With 4 out of 10 SBF flats are already completed, this allows buyers to move in at a short notice.

The remainder of the SBF projects mostly had drastically reduced wait times and might be appealing to homebuyers who might have less urgent housing needs, offering a more affordable alternative to the resale market.

The SBF exercise offered flats in mature estates and centrally located (prime) locations, but without the new resale restrictions imposed on newer Prime Location Housing (PLH) flats. Combined with a shorter completion runway, these flats drew high application rates and could have stolen some of the thunder away from the resale market.

Applicants of these flats are waiting the results – should they not be able to secure a unit, we could very well see them return to the resale market in 2Q 2025.

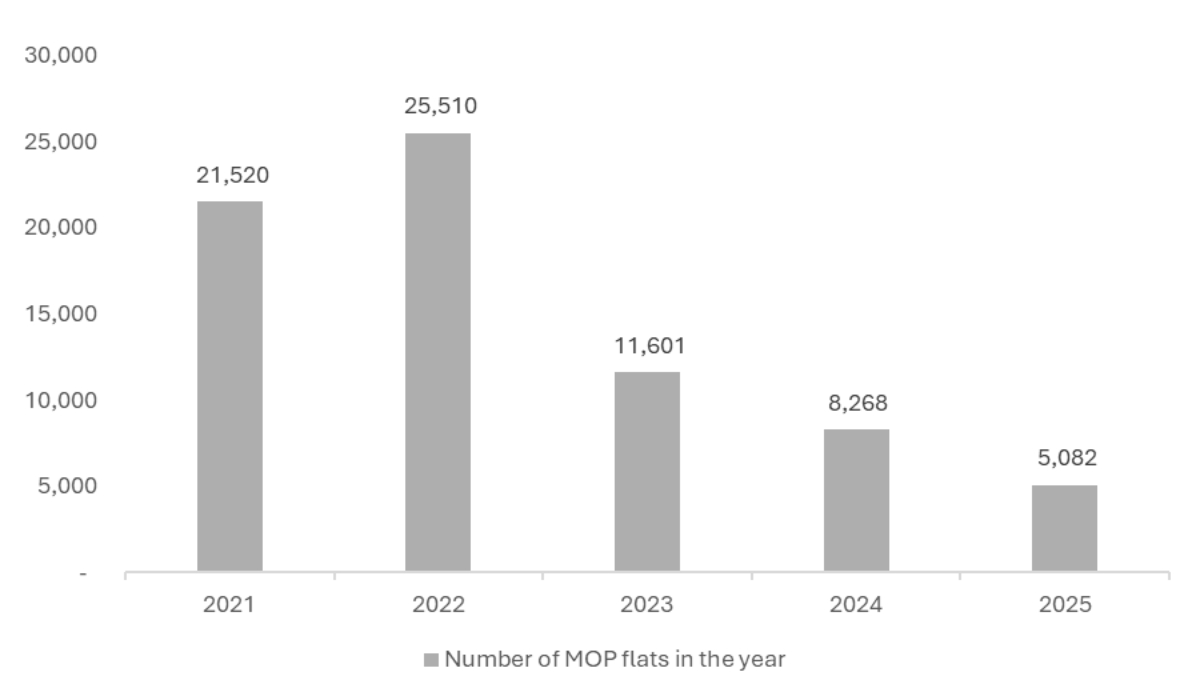

Fewer MOP flats compared to 2024

In 2025, we will see 5,082 HDB flats fulfil their Minimum Occupation Period (MOP). This figure is 38.5% less than what we witnessed in 2024, which already saw stress being placed on resale prices.

This is apparent for resale flats in central locations and mature estates. BTO flats in these locations fall under the new classification of Plus and Prime classification BTO flats may have driven more homebuyers to seek out HDB resale homes instead.

Chart 2: Number of MOP Flats by year

Source: HDB as at 27 March 2025, ERA Research and Market Intelligence

These buyers are unwilling to accept the resale restrictions such as a 10-year Minimum Occupation Period, rental restrictions after MOP, subsidy clawback upon resale and resale income cap that the new classification of flats place on future buyers.

With fewer of these flats being made available, prices for them are steadily increasing, which could discourage buyers with more modest budgets from making their upgrades or purchases.

Likewise, knowing the lack of supply in the market now, homeowners of these flats could have greater holding power and are less likely to sell their units unless a good deal falls into their hands.

Million-Dollar Flat Transactions on the rise

In 1Q 2025, there was an increase in the number of million-dollar flat transactions from 285 in 4Q 2024, to 295 in 1Q 2025. This is a 3.5% q-o-q increase and a 61.2% y-o-y increase from 183-million-dollar transactions in 1Q 2024.

We noted that 271 (or around 78%) of these million-dollar flat transactions consisted of 4-room and 5-room flat transactions. A 5% increase from the previous four quarter average, this shows a trend of 4-room and 5-room flats increasing in price, driving the million-dollar flat market.

Chart 3: HDB Flat Transactions over $1m

Source: HDB as of 27 Mar 2025, ERA Research and Market Intelligence

The percentage of million-dollar flat transactions in 1Q 2025 accounted for 8.9% of all transactions this quarter, doubling 4.6% in 4Q 2024.

Flats in mature estates continue to make up the bulk of the million-dollar flat transaction, highlighting the demand for homes in choice locations.

Apart from private home downgraders, there are increasingly more HDB dwellers willing to shell out a premium for a newly and centrally located flats. They may choose to upgrade within the HDB market itself, opting to purchase larger homes in central locations with longer leases, such as newly-MOP flats. These homes offer outstanding location attributes, with good transport connectivity, amenities and proximity to good schools, making them a great choice.

With the decline in the number of MOP flats in 2025, we expect to see prices of these flats continue to rise amid firm demand.

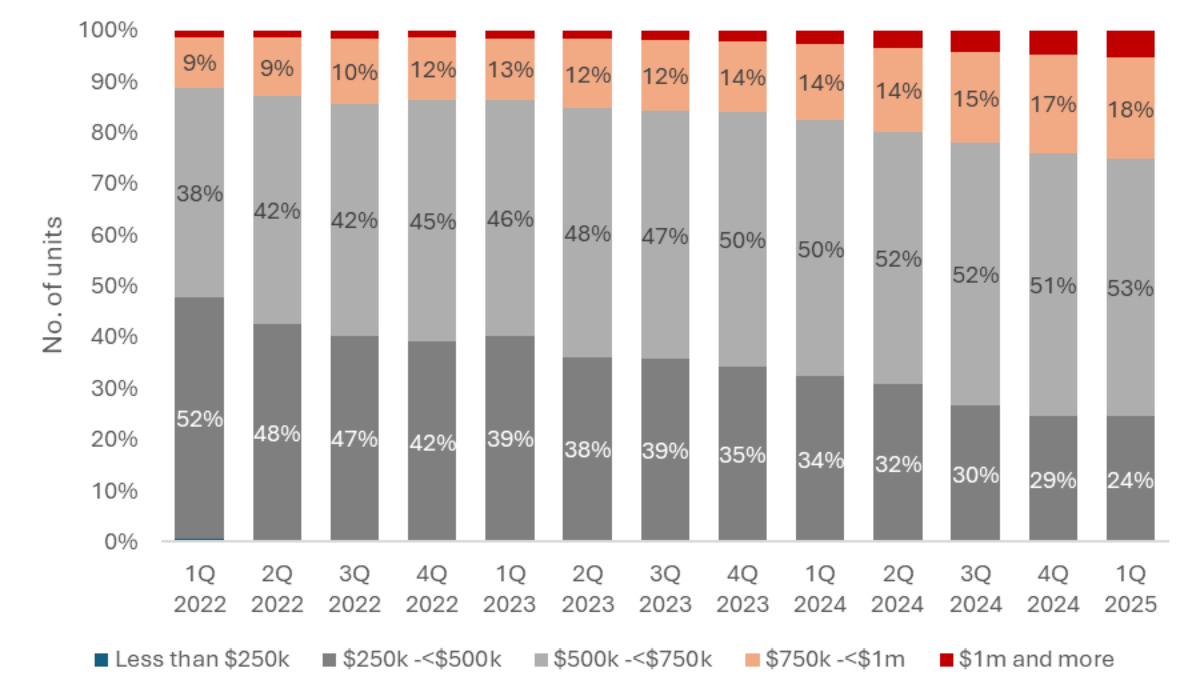

Chart 4: HDB Transactions by Price Ranges

Source: data.gov.sg as of 27 March 2027, ERA Research and Market Intelligence

Despite this, the majority of HDB resale flats remain affordable. Some 53% of the HDB resale transactions in 1Q 2025 fell between $500k and $750k, a comfortable price range for most Singapore homebuyers. Another 24% fell between $250k and $500k. This makes up about three-quarters of HDB resale transactions that still remain affordable and accessible to homebuyers.

ERA’s Outlook and Forecast for the rest of the year

We should see a recovery in transaction volume in the following quarters as applicants of the BTO and SBF exercises that took place in the quarter are likely to look towards the resale market in the following months if they are unable to secure their units. This should, in turn bolster transaction volume in 2Q 2025.

With a reduced supply of MOP flats in 2025, which have been a key driver of price growth in recent years, we should see a moderate price growth, and fewer transactions to close out the year. We anticipate an overall 3% – 6% price growth, with 26,000 – 27,000 resale HDB flat transactions by end-2025.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.