This article was brought to you in conjunction with Hoi Hup Realty and Sunway Developments, and ERA Property Megashow – the premier event for discovering valuable investment opportunities in Singapore.

Terra Hill is a small development with 270 housing units developed through a joint venture between Hoi Hup Realty and Sunway Developments.

The development is located on the incline of Yew Sian Road, with the entrance and the highest point of the development having a 20-metre difference. It has five storeys of residential blocks, with a good elevated view of surrounding infrastructures such as the Port of Singapore Authority (PSA) Pasir Panjang Port, other low-rise housing developments, and lush greenery from parks nearby.

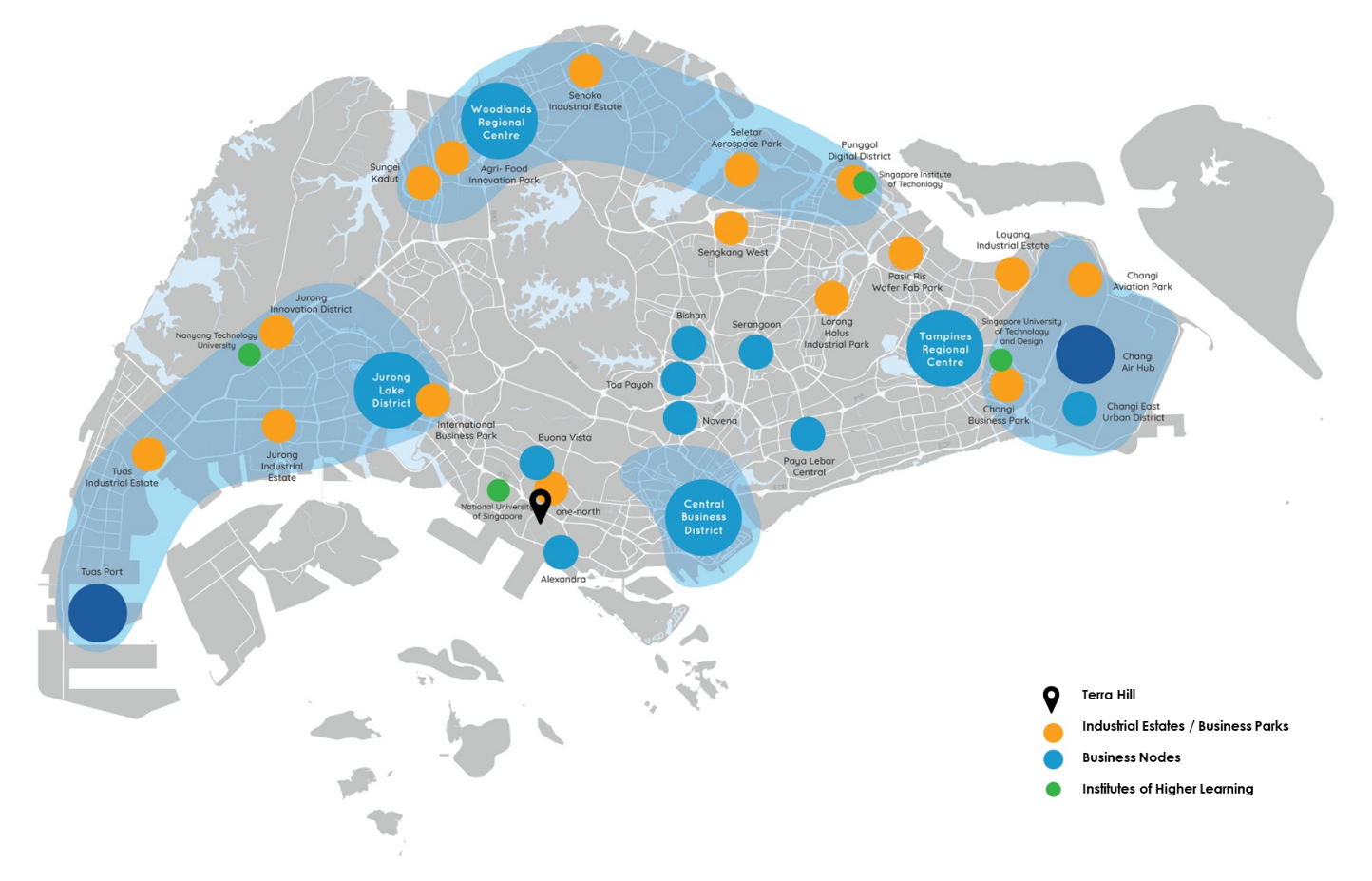

Terra Hill is also the epicentre of several major business nodes, being less than 15 minutes away from these centres by car, which may appeal to professionals looking for a home within the vicinity of their workplaces.

Picture 1: Map of Terra Hill and Singapore’s Work Hubs

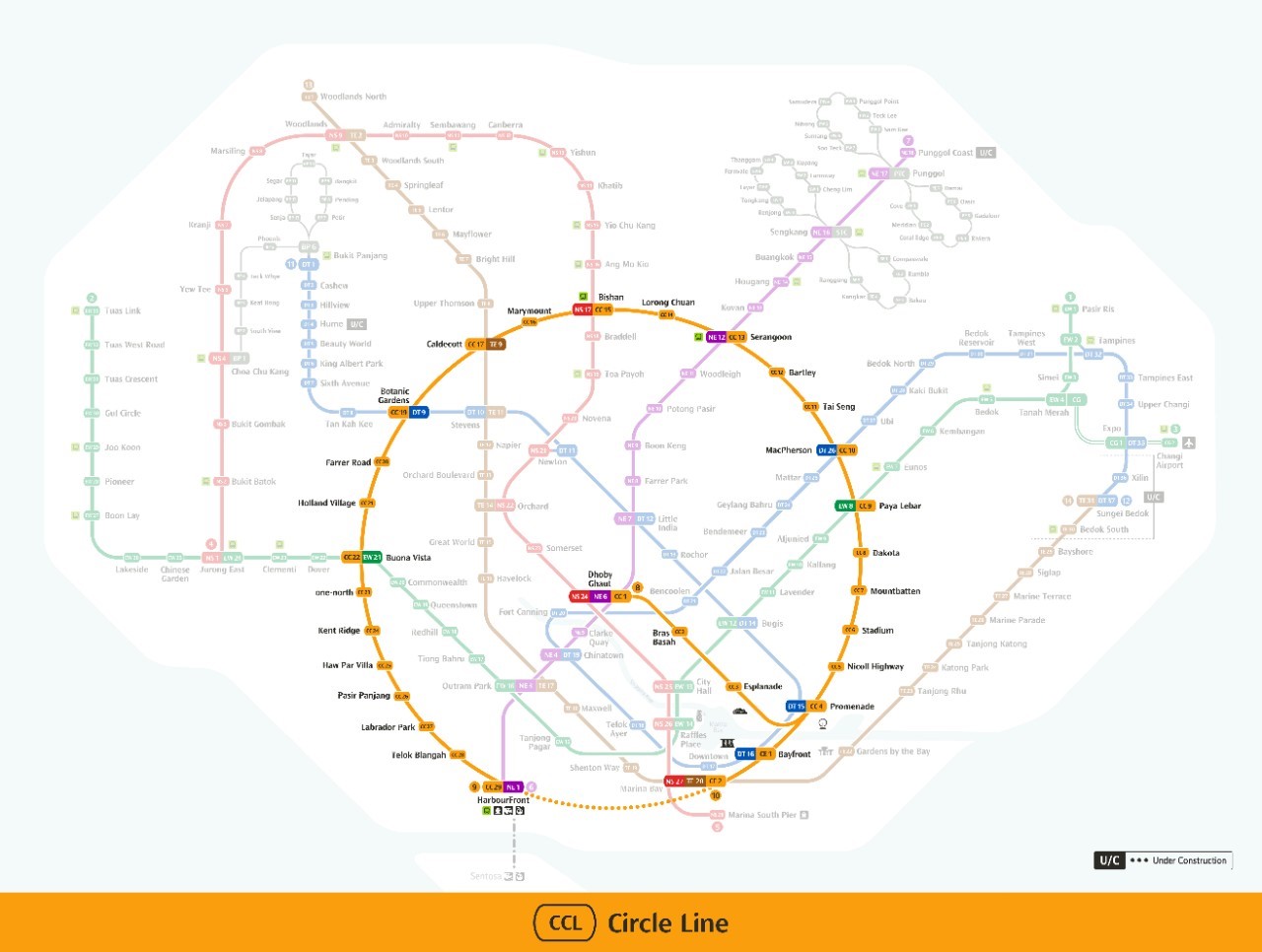

The development is served by the Circle Line, with Pasir Panjang MRT Station being an eight-minute walk away from Terra Hill. Residents will be connected to Harbourfront MRT and bus Interchange, Buona Vista MRT Interchange and the northern and eastern parts of Singapore through these interchanges.

By 2026, the Circle Line will be completed with three stations being built between Harbourfront and Marina bay MRT stations, closing the circle on the MRT line. This will increase connectivity to several major business nodes including the Central Business District.

Picture 2: Circle MRT Line

Source: Land Transport Authority, ERA Research and Market Intelligence

For residents who mainly drive, the West Coast Highway and the Ayer Rajah Expressway (AYE) are two major expressways that serve the area and connects residents to the rest of the island. A new road connecting South Buona Vista Road to Portsdown Avenue will be built to connect both expressways, making driving in the area easier.

Picture 3: New Road linking West Coast Highway to Ayer Rajah Expressway

Source: Hoi Hup Sunway, ERA Research and Market Intelligence

Sitting on the former site of Flynn Park Condominium, the new and improved condo development has a wider variety of unit types ranging from two bedroom to five-bedroom penthouses, with high quality facilities and installations from reputable brands such as De Dietrich, Gessi, Laufen, and Samsung.

Now, let’s delve into the three reasons why you should buy a Terra Hill property.

Reason 1: 270 exclusive freehold units

Freehold land in Singapore is already limited, and with the high demand for freehold housing from Singaporeans and foreigners, the 270 units in Terra Hill are rare and exclusive, being the one of the two latest freehold launches in the Rest of the Central Region (RCR). Residents will enjoy indefinite exclusivity and tranquillity within the estate. Additionally, properties surrounding Terra Hill include landed housing and other low-rise private developments, adding to the tranquil ambience.

Reason 2: Exit Strategy for owners (Greater Southern Waterfront Development)

As part of the URA Master Plan, the Greater Southern Waterfront will be transformed into a major gateway and location for urban living along Singapore’s southern coast. The waterfront will include over 9,000 new housing units, both public and private, more offices spaces, job opportunities, more entertainment and leisure options. This will be accomplished through the repurposing and revitalisation of current structures such as the Pasir Panjang Terminal. This waterfront precinct is six times the size of Marina Bay, and residents of Terra Hill will be able to see the transformation of the area over time from their homes.

Picture 4: Former Keppel Club site to be redeveloped into HDB flats

The construction of these HDB flats will provide a supply of potential future upgraders for owners of Terra Hill, adding another dynamic element to its existing exit strategy. They will have plenty of new public and private housing options to right size or upgrade to after the development of the Greater Southern Waterfront.

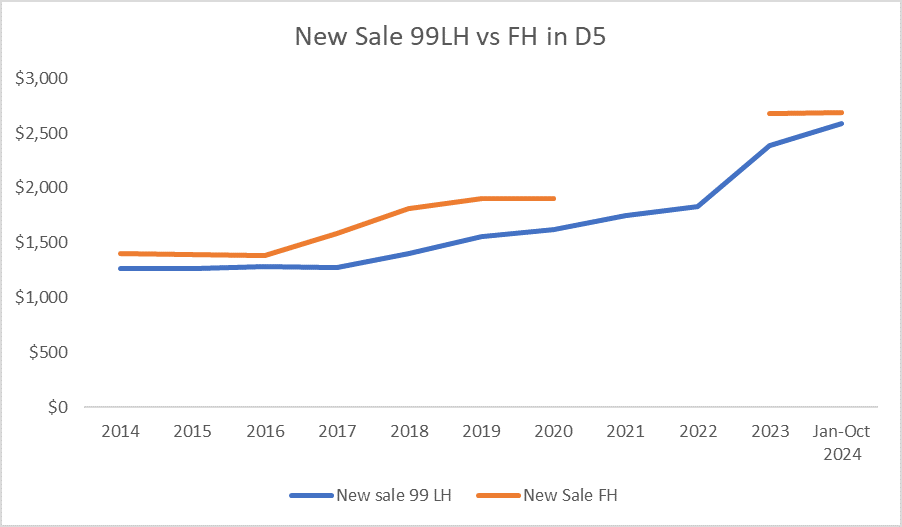

Reason 3: Freehold but has comparable prices to leasehold properties nearby

Given the rarity of freehold units in the RCR and Singapore, the price of units in Terra Hill are generally lower compared to other developments in its region, which make this a very affordable option for those looking for a freehold property in the city fringe.

Chart 1: New Sale Leasehold (99 LH) vs Freehold Properties in District 5 (D5)

Source: URA, ERA Research and Market Intelligence as of 19 Nov 2024

As the price gap between freehold properties and leasehold properties in the area is decreasing, buying Terra Hill would be a good deal since the price paid for this property would be similar to that of a leasehold property in the same area.

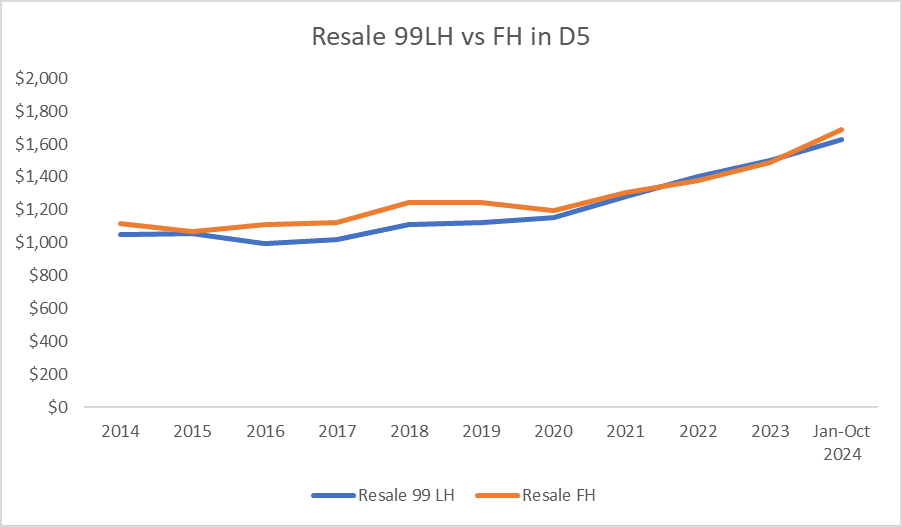

And this is not only seen for new sale properties, but also resale properties in D5. Although the average price of a resale freehold property is still more expensive compared to a leasehold property, it is more valuable to buy the freehold property since the prices are very similar, yet the tenures drastically differ.

This could be due to the freehold developments being generally older than the leasehold developments in the area, with Terra Hill being one of just two new launches in D5 in the past two years.

Chart 2: Resale Leasehold vs Freehold Properties in D5

Source: URA, ERA Research and Market Intelligence as of 19 Nov 2024

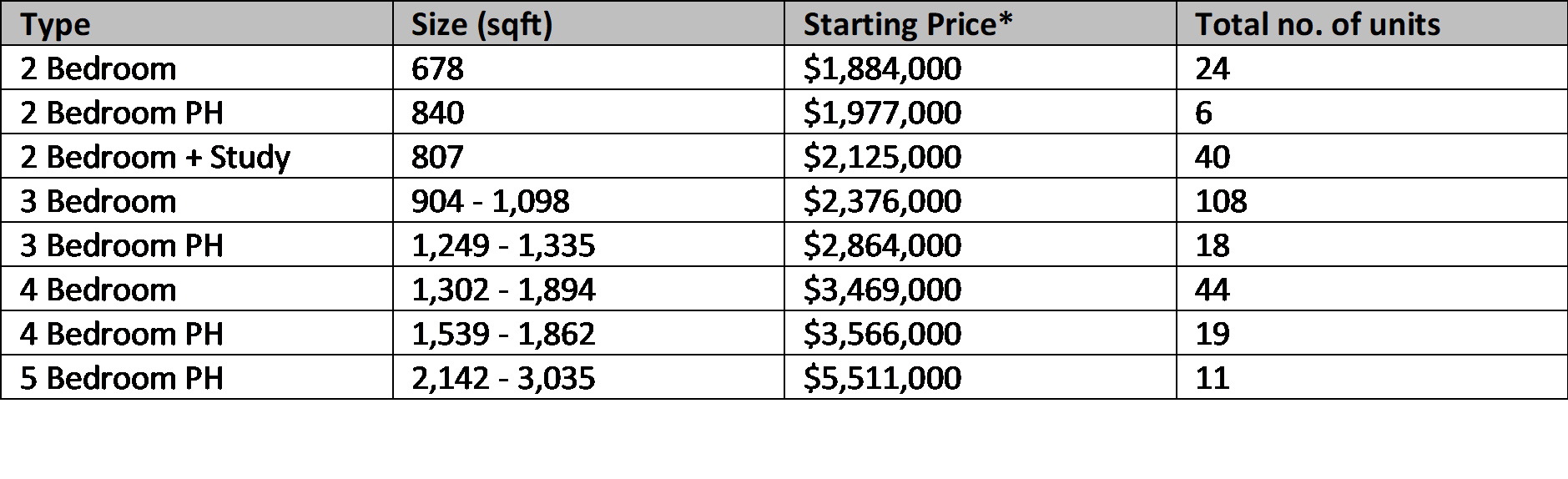

Here are the units available at Terra Hill.

Consisting predominantly of three-room apartments, Terra Hill’s target audience may likely be investors, young couples or retirees looking to right size from a bigger house. For those who wish to rent instead of buy, rental rates in D5 are comparable with the RCR, with the number of rental contracts in D5 seeing a general increase in the last five years. Expats who work in the city or in key nodes should definitely consider renting Terra Hill, given the comparable rates.

Table 1: Unit types available at Terra Hill

Source: ERAPro, ERA Research and Market Intelligence as at 19 Nov 2024

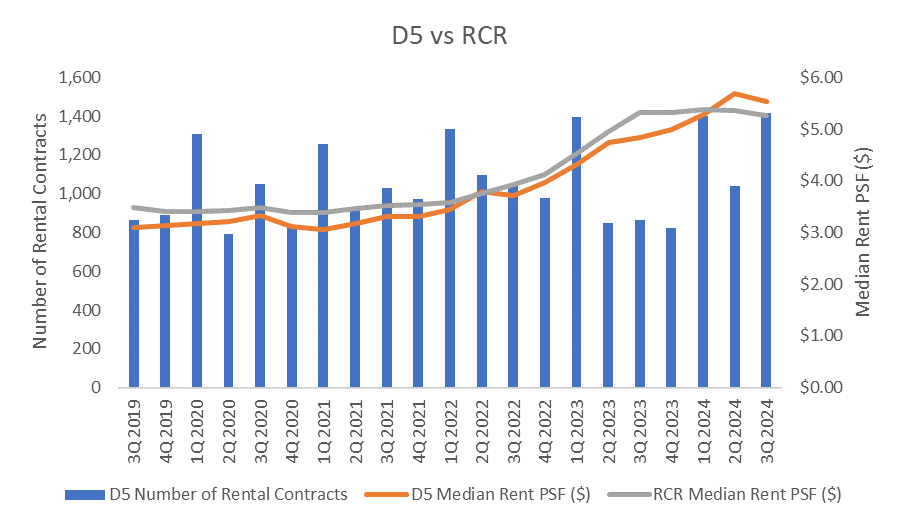

Chart 4: D5 vs RCR Median Rents

Source: URA, ERA Research and Market Intelligence as of 19 Nov 2024

Now, let’s take a look at some unit types Terra Hill has to offer.

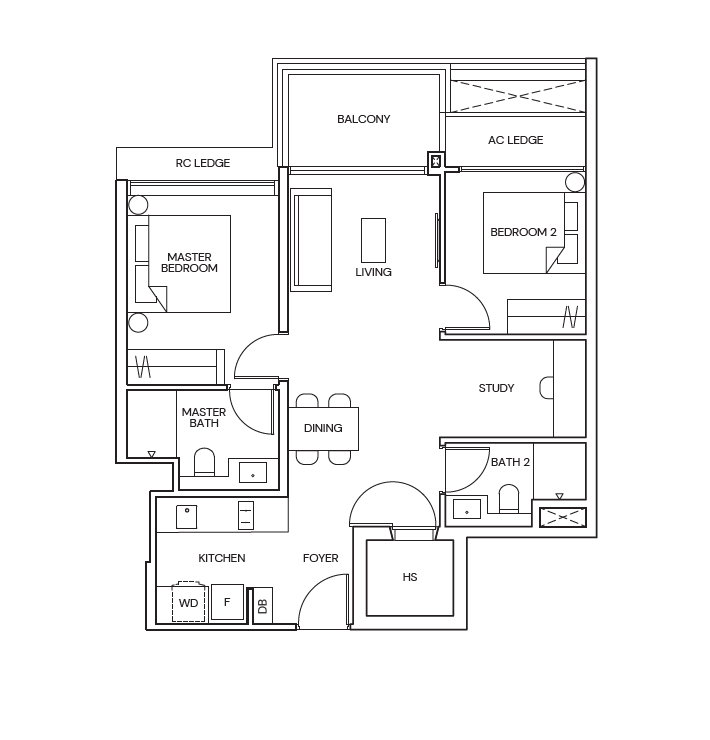

Two Bedroom + Study Floorplan

Built in a “dumbbell” layout, the two-bedroom + study layout offers an open kitchen concept, which may help eliminate underused space within the house. The study is placed in a corner that opens to the living and dining area, offering some privacy. Similarly, the bedrooms are placed at opposite sides of the apartment which offer privacy to the occupants of each room. The apartments in this particular type of units (B3) also have a balcony, which other two-bedders in the development do not have.

Starting from $2,125,000, investors, Dual-Income-No-Kids (DINKs) or individuals looking to buy or rent a small space may be keen to purchase this type of unit.

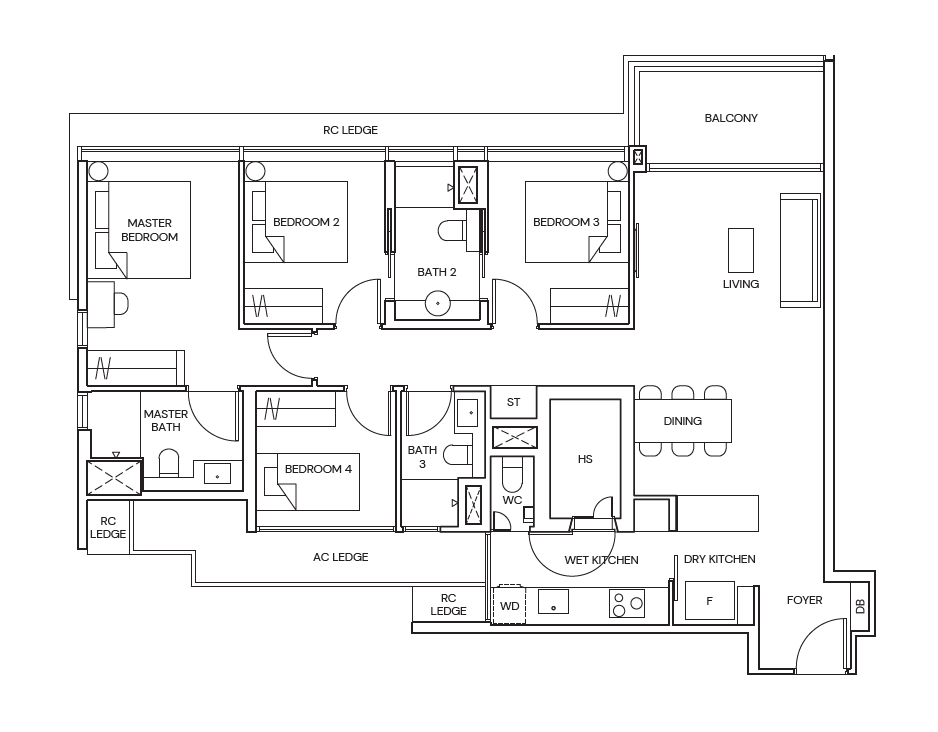

Four Bedroom Floorplan

Under the prestige collection of units, which are limited to the four to five-bedroom penthouse residences, a private lift lobby will serve individual units, together with several other prestigious fittings in the units.

One other special thing about the four and five room units in Terra Hill is that they have both a dry and wet kitchen, which can help to keep the place organised. Unlike the two- and three-room apartments, the four-bedroom apartments are built in a “corridor” layout, where all the rooms are connected through a common corridor. The bedrooms are placed together at a corner of the apartment, with bathrooms nearer to the bedrooms to increase convenience to the occupants of the room.

Despite the smaller living space, this type if unit may appeal to larger families. These units are priced from $3,503,000.

Interested in learning about Terra Hill? Connect with an ERA Trusted Adviser today for more information.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

URA dropped ten sites on the Confirmed List. Could this lead to a potential housing glut?

On the 25th June 2024, the Urban Redevelopment Authority (URA) announced a list of ten sites on the Confirmed List for their Government Land Sales (GLS) program. These will comprise nine residential sites, inclusive of an executive condominium (EC) plot, and a residential and commercial plot.

This is part of an active effort by the government to stabilise property prices and manage long-term housing demand. We are positive that this will give homebuyers more choices in the future, especially with sites in sought-after locations like Bayshore Road and Chuan Grove.

Overall, these ten sites could yield an estimated 5,050 residential units – a similar figure to the 5,450 units offered in 1H 2024’s Confirmed List of GLS sites.

A total supply of 11,110 private residential units in 2024 (including 610 units from the activated Reserve List site tendered out in May 2024) will be the highest supply introduced in a single year since 2013.

The sites available under the Confirmed List are as follows.

Table 1: Confirmed List 2H 2024

| Site | Type of Site |

Area (ha) |

Proposed GPR |

Estimated No. of Residential Units |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (sqm) |

Estimated Launch Date |

Agency |

| Tampines Street 95 (EC) | Residential |

2.25 |

2.5 |

560 |

0 |

– |

Aug-2024 |

HDB |

| Faber Walk | Residential |

2.58 |

1.4 |

400 |

0 |

– |

Sep-2024 |

URA |

| Lentor Gardens | Residential |

2.06 |

2.1 |

500 |

0 |

– |

Oct-2024 |

URA |

| River Valley Green (Parcel B) | Residential |

1.17 |

3.5 |

580 |

0 |

500 |

Oct-2024 |

URA |

| Bayshore Road | Residential |

1.05 |

4.2 |

515 |

0 |

– |

Nov-2024 |

URA |

| Media Circle (Parcel A) | Residential |

0.81 |

3.7 |

345 |

0 |

400 |

Nov-2024 |

URA |

| Media Circle (Parcel B) | Residential |

0.97 |

4.3 |

485 |

0 |

400 |

Nov-2024 |

URA |

| Chuan Grove | Residential |

1.58 |

3.0 |

550 |

0 |

– |

Dec-2024 |

URA |

| Holland Link | Residential |

1.72 |

1.4 |

240 |

0 |

– |

Dec-2024 |

URA |

| Chencharu Close | Commercial & Residential |

2.94 |

3.2 |

875 |

0 |

13,000 |

Sep-2024 |

HDB |

Source: URA, ERA Research and Market Intelligence

Among the sites, the Tampines Street 95 EC site and Chuan Grove are located within established residential enclaves that have previously seen resilient housing demand. This could draw higher interest from developers.

In addition to this, the URA has also placed an additional nine sites on their Reserve List as part of the 2H 2024 GLS program, should developers feel the need to bid for extra sites based on market demand. The Reserve List comprise five residential sites, one commercial site, two white sites, and a hotel site.

In total, they offer a potential 3,090 residential units, as well as 99,350 sqm gross floor area of commercial space, and 530 hotel rooms.

Table 2: Reserve List 2H 2024

| Site | Type of Site |

Area (ha) |

Proposed GPR |

Estimated No. of Residential Units |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (sqm) |

Estimated Launch Date |

Agency |

| Senja Close (EC) | Residential |

1.01 |

3.0 |

295 |

0 |

0 |

Available |

HDB |

| Marina Gardens Lane | Residential |

0.61 |

5.6 |

400 |

0 |

0 |

Oct-2024 |

URA |

| Woodlands Drive 17 (EC) | Residential |

2.58 |

1.7 |

435 |

0 |

0 |

Oct-2024 |

HDB |

| Holland Plain | Residential |

1.58 |

1.8 |

275 |

0 |

0 |

Dec-2024 |

URA |

| River Valley Green (Parcel C) | Residential |

1.15 |

3.5 |

470 |

0 |

0 |

Dec-2024 |

URA |

| Punggol Walk | Commercial |

1.00 |

1.4 |

0 |

13350 |

0 |

Available |

URA |

| Marina Gardens Crescent | White |

1.73 |

4.2 |

775 |

6000 |

0 |

Available |

URA |

| Woodlands Avenue 2 | White |

2.75 |

4.2 |

440 |

78000 |

0 |

Available |

URA |

| River Valley Road | Hotel |

1.02 |

2.8 |

0 |

2000 |

530 |

Available |

URA |

Source: URA, ERA Research and Market Intelligence

A total of 17 new projects are set to launch in 2H 2024, tallying to an estimated 8,300 new homes.

There are eight more sites currently open for tender, and another one set to launch this month. This bumper crop of GLS sites in 2H 2024 will further bolster the existing ample land supply.

However, prevailing factors like the high-interest rate environment, economic uncertainty, and slower new home sales amidst tighter homebuyer affordability may encourage developers to bid prudently.

Let’s go over the location analysis for the ten GLS sites on the confirmed list.

Tampines Street 95 (EC) – 560 units

Source: URA

In contrast to the plot at Tampines Street 94 (previously launched in 1H 2024), the newly released site at Tampines Street 95 is earmarked for development as an EC project.

Being near its sister plot, this puts the site at Tampines Street 95 within range of Tampines West MRT station, Bedok Reservoir Park, as well as future retail options at Tampines Street 94. This confluence of amenities, coupled with its designation as an EC site, will likely make Tampines Street 95 an attractive proposition for developers and future buyers alike.

Faber Walk – 400 units

Source: URA

This site is between AYE, Pandan River and the Faber Walk landed enclave. It will be a low-rise development of up to five storeys, comprising of 400 units. While there are no MRT stations in the vicinity, is it only a 5-minute drive to Clementi MRT Station. Despite being next to AYE, residents will enjoy privacy in this tranquil living environment along Pandan River. The adjacent site (now Waterfront@Faber) was previously awarded for $687 psf ppr in June 2013. We may see muted response due to the location of the site.

Lentor Gardens – 500 units

Source: URA

Even though the Lentor Gardens GLS site is the last site available in the Lentor Hills estate, much of the area’s housing demand has been absorbed by earlier launches. Furthermore, it is the furthest site from Lentor MRT station making it less advantageous compared to neighbouring plots. Thirdly, the upcoming Upper Thomson site awarded to GuocoLand and Hong Leong will also provide prospective homebuyers with more options.

River Valley Green (Parcel B) – 580 units

Source: URA

The launch of the River Valley Green (Parcel B) site comes hot off the heels of the closure of Parcel A’s tender last week. The site, which is an estimated yield of 580 units, borders Great World MRT and is also near Great World City and River Valley Primary School. However, despite its remarkable locational attributes, it remains to be seen whether developers will exhibit interest for Parcel B, given the saturation of new launches in the area for the next two years.

Bayshore Road – 515 units

Source: URA

The Bayshore Road site is the first to be launched in the area since 1997. With a potential yield of 580 residential units, it will join upcoming HDB projects in shoring up Bayshore’s nascent future as a new waterfront neighbourhood. The site’s proximity to the newly operational Bayshore MRT station and the expansive views of East Coast Park from future high-rise units are also compelling selling points. We expect to developers to put in competitive bids for the site, especially with Bayshore’s promising future and the scarcity of newer private residential developments in the area.

Media Circle (Parcel A) and (Parcel B) – 345 and 485 units

Source: URA

Source: URA

Straddling each side of Portsdown Road, both the Media Circle (Parcel A) and Media Circle (Parcel B) sites are poised to bolster the future housing supply in one-north with a total of 830 estimated residential units; this is in line with URA’s plans to enhance the area as a vibrant mixed-use district. This could also make shorter office-to-home commutes a reality for residents working in the vicinity.

Additionally, unlike the Media Circle plot launched in 1H 2024, both new sites are not required to include a Serviced Apartments II (SA2) component. Without the mandatory requirement to include long-stay serviced apartments, developers will likely be more motivated to bid for these parcels in the face of diminished risk.

Chuan Grove – 550 units

Source: URA

This site can potentially yield 550 homes in high-rise tower blocks. It will likely draw competitive bids being on the edge of the city fringe with amenities and schools while being a 3-minute walk to Lorong Chuan MRT Station. The existing Chuan Park site that was sold enbloc is scheduled to launch in 2H 2024.

Holland Link – 240 units

Source: URA

The GLS site at Holland Plain consists of an estimated 240 units and is located amidst a predominantly landed housing enclave. Considering its exclusive location, the site is likely to be developed as high-end luxury homes to support housing needs for the residents in the vicinity.

Chencharu Close – 875 units

Source: URA

Chencharu’s status as Yishun’s newest residential precinct will translate into new convenience-driven amenities for residents, both existing and new. Close to 2,000 private residential units are slated for development in Chencharu; this figure is inclusive of its first-ever mixed-use site where 875 private homes could be potentially built, accompanied by a bus interchange and hawker centre.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.