Singapore’s Central Area was actually one of the first few areas where homes were introduced. In the 1970s, HDB mixed-use developments such as Tanjong Pagar Plaza, Bras Basah Complex and People’s Park (Chinatown). Later, more HDBs were added including those at Everton Park and most recently, Pinnacle@Duxton (completed in 2009). These places were highly sought after due to their central locations, and had amenities to serve the residents’ needs.

However, over the past two decades, Singapore’s Central Business District (CBD) has evolved from a primarily office-focused area into a more livable space. Initially, it was home to large offices, the CBD was only alive between 9 to 6 on weekdays.

Recently, the CBD has seen a shift toward residential and mixed-use developments. The Urban Redevelopment Authority (URA), through its 2014 and 2019 Masterplans and the 2019 CBD Incentive Scheme, has introduced more parks, community spaces, and homes. Developers are encouraged to convert older office buildings to mixed-use developments to inject a larger live-in population. This initiative aims to build a larger residential population and diversify amenities in the CBD, offering developers bonus gross floor area as an incentive.

“We can make our CBD not just a place to work, but also an attractive and vibrant place to live and play.” – Lawrence Wong, 2019

Today, our CBD is a much more vibrant space, offering a day-to-night environment. It continues to attract weekend crowds for various reasons—for food, exercise, or shops featuring curated activities and workshops. The wider streets are pedestrian-friendly, lined with cafes, al-fresco dining options, and convenience stores, some with adjacent cycling paths and park connectors. Public squares and gardens contribute to placemaking efforts and foster more interactions.

Nightlife culture is also thriving in the CBD, with bars and restaurants catering to the working crowd and weekend revellers. The foreign tenants and short-term travellers seeking accommodations in these centrally located areas adds to the vibrancy, offering a unique atmosphere and experience.

Public events held in the CBD on a Car-free Sunday

“You can’t be more centrally located than being located in the centre”

Location is the keyword when one talks about real estate. Usually, properties located near city centres are the most valuable, because it comes with amenities and activities.

Therefore, Build-To-Order (BTO) HDB flats in these prime locations in and around the CBD are over-subscribed. Resale flats in the Central Area still sees high demand despite shorter remaining leases (less than 60 years). This is a testament that Singaporeans desire to live in the CBD.

Why so? Because for those working in or around the CBD, living there makes the most sense. Residents enjoy the quick commutes, saving valuable time. Wouldn’t you want to live within walking distance of your workplace? Some buildings in the CBD even offer bicycle parking and end-of-trip facilities.

Additionally, residing in the heart of Singapore makes it easier to access other parts of the island. The CBD boasts 13 MRT stations across all six lines, providing excellent connectivity to virtually anywhere.

“People talk about wanting amenities – downtown is the amenity.”

Imagine this: after a long day of work in Tanjong Pagar, you take a short 10-minute walk home and stop by a supermarket for a quick grocery run before picking up your child from preschool. On the way home, you decide between a bike ride to Gardens by the Bay, a boxing class at the gym across the road, or unwinding at one of the bars beneath your condo. On remote workdays, you visit your regular coffee joint for a quick breakfast followed by a couple of productive hours there. Do you see yourself having this lifestyle?

Beyond the convenience from the location, residents of the CBD actually enjoy the lifestyle of having everything around you. From food options to amenities to green spaces, places of worship and leisure spots, most things can be found within walking distance away.

While remote work may make it seem like city living is no longer relevant, hybrid employees may find it more productive to work in third places in CBDs such as cafes and coworking spaces.

Amenities

Many believe the CBD lacks amenities for residents, but on the contrary, it offers a wide range of options. Fitness enthusiasts have access to numerous gyms, including specialized ones for climbing, martial arts, yoga, and even quick 30-minute lunchtime workouts. For those seeking a break from the urban environment, parks like Pearl’s Hill City Park, Fort Canning Park, and Gardens by the Bay provide nearby green spaces for jogging or cycling after work.

Everyday needs are well-served by malls such as Icon Village, 100 AM, Tanjong Pagar Plaza, and Chinatown Point, offering supermarkets, clinics, pharmacies, and personal care services. Families with young children benefit from the many childcare centers and preschools in areas like Tanjong Pagar, Telok Ayer, Clarke Quay, and Marina Bay.

Newer CBD developments also feature public spaces designed for community activities. Examples include Guoco Tower’s Urban Park, Capitaspring’s sky garden, and IOI Central Boulevard Towers’ Central Green garden that enhances livability.

Guoco Tower’s sheltered outdoor space that is used to host events, attracting people to gather and hang out.

Aplenty of Food Options

In the past, food places in the CBD are only open till lunch time on weekdays. Today, you find that they are widely available, catering to every budget and occasion. Whether you are just looking for daily sustenance, a leisurely weekend brunch or want to have a nice meal out for a celebration, there is something for everyone. A common misconception is that food is costly in the CBD. While that holds true for some of the classiest restaurants or hip and trendy bars, there are actually eight NEA-run hawker centres inS the CBD. They provide affordable food and drink options.

Moreover, regardless of what cuisine you are looking for, you can probably find it there. Coffee houses and bars are also scattered around and are widely available.

Maxwell Food Centre, a hawker centre in the heartof the CBD

While city living offers plenty, it may not be for everyone

With all these desirable attributes, does living in the city still make sense for everyone? Definitely not. It still lacks schools for families with school-going children. Cantonment Primary School is the only one in the CBD, along with few enrichment centres.

Furthermore, those working in the CBD may not necessarily want to live there. It can be difficult to disconnect from work during time off. Some may be put off by the weekday crowds, with too much ‘buzz’ and ‘commotion’ around. Others might find the demographics and community in the CBD unsuitable, as it is largely made up of expats, tenants, and leisure travellers. As a result, residents may not feel as connected, and the community may not be as close-knit.

City living also comes with higher cost of living. With higher rents in the city centre, food and services are likely to cost more compared to suburban areas.

While CBD living caters to many, there is still a lack of stock in the market. Currently, there are only 12,957 private residential units in the CBD. This amounts to just 3.8% of all homes island-wide, or just slightly above the entire District 20 (Ang Mo Kio, Bishan, Thomson). The lack of homes could be turning aspiring CBD homeowners away as they seek to find their dream home.

Shifting the focus (and homes) back to the city centre

Over the years, the success of URA’s decentralisation strategy coupled with the improved public transport network and more comprehensive amenities, have driven people to stay further outskirt.

Singaporeans are also hesitant to live in the CBD with the lack of housing options that has driven home prices higher. However, the allure of living in city centre remains given its convenience.

More importantly, the idea of living in the CBD is not a new one. It was simply set aside as Singapore focused on developing its financial hub. With URA’s push for to transform the CBD into a work-live-play location, more homes have been progressively been planned for the CBD and we may see more Singaporeans returning to live in the city centre in time to come.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Freehold land parcels were last sold prior to the introduction of GLS Programme in 1967, mostly taking place before Singapore’s independence. If all Government Land Sale (GLS) sites have a 99-year leasehold (99-LH) tenure, then why are there 999-year leasehold (999-LH) or freehold developments?

In land-scarce Singapore, selling residential land on a 99-year lease allows the government flexibility to reallocate land in the future, and to meet the evolving needs of society.

Freehold Land is a Rare Commodity

Currently, new freehold developments are available as property developers purchase freehold land via the collective sale of older projects. Such new projects are rare and remain highly sought after, as they are not subject to lease decay. This makes them an attractive option for buyers looking to purchase a property for their own stay, or as a legacy asset.

Given a quiet en-bloc market with an abundance of sites released in the 2024 GLS Confirmed List, new freehold condos are becoming increasingly scarce. Developers are unlikely to pay a sizable amount for a freehold site that comes with more encumbrances and costs (e.g. demolition), especially with the wide array of sites available under the GLS scheme. With a slow en-bloc market, particularly for freehold sites, there will be a dearth of new freehold units available in the near future. Only 603 freehold units are expected to be launched in the coming months.

When purchasing any property, buyers often have to face an iron triangle – a form of ‘give-and-take’ regarding the attributes of a property. In this case, the balance lies between the age of a property, its locational attributes (e.g. the availability of MRT stations), and lastly affordability. Freehold developments are often on the pricier end, which might make the ‘perfect’ freehold property more elusive to attain.

This coincides with ERA’s recently concluded My Dream Home Survey, which found that homebuyers prioritise affordability, size of the property and proximity to public transportation as key considerations for their next home purchase. Among survey participants keen on owning a private property as their next home, over 55% indicated a preference for new launches.

Where are FH condos usually located?

Freehold condos are spread across island-wide. However, there is a higher concentration of them in the city centre (e.g. Orchard, River Valley, Bukit Timah, Newton and Novena) or the city fringe (e.g. Katong, Joo Chiat, Marine Parade, Upper Bukit Timah). In line with Singapore’s urban development, these more centrally located areas were developed first, before moving outwards. Naturally, being centrally located, these developments would command higher prices.

While freehold properties are also found in suburban areas such as in Serangoon or Pasir Ris, their supply is more limited. These areas were developed much later, with land sold with leasehold tenures under the GLS programme.

Furthermore, MRT stations were also planned after the GLS Programme was introduced. Therefore, much of the land near MRT stations would have a leasehold tenure, barring those sold prior to the stations being planned.

Terra Hill, a freehold development located just 400m from Pasir Panjang MRT Station

ERA estimates approximately some 44% of non-landed homes to be of freehold or 999 leasehold status, relatively well distributed across market segments. But with the introduction of GLS program, this has helped ramped up the supply of leasehold homes, particularly in the Outside Central Region (OCR). Even though the supply of freehold units in the OCR has remained largely the same, the proportion of such homes in the region has dwindled to 28% due to the growing number of leasehold properties over time.

Table 1: Breakdown of Units by Tenure

Source: URA, ERA Research and Market Intelligence

Why do buyers prefer a new development despite the freehold tenure?

While older resale condos are typically more affordable than freehold properties in the same location, they could come with higher renovation and maintenance costs.

The older unit and development might not be well-maintained, and having outdated building designs and dreary façades could make them unappealing. Additionally, aging facilities that are under-utilized or poorly maintained due to wear and tear might be unpleasant to use or even pose safety risks.

Freehold property owners pay a premium for perpetual ownership. Unless the maintenance cost of their unit or the development becomes too high, it is unlikely that they will want to sell, whether individually or via a collective sale.

If the development’s age is a concern, or if buyers prefer a newer property, they may need to scour the market to find what they are looking for, or pay close attention to the en-bloc market. After all, freehold developments are becoming harder to come by as the years go on.

Entry Price

Are freehold properties still affordable? Despite commanding a premium, freehold properties are still alluring to many buyers as they offer perpetual ownership. Without the threat of lease decay, freehold properties also retain their value better over time.

Chart 1: Median Price psf for Freehold vs 99-Leasehold

Source: URA as of 7 Aug 2024, ERA Research and Market Intelligence, FH transactions include 999-LH

Furthermore, with the closing gap in prices between freehold and leasehold properties, prospective homebuyers may find freehold homes to be a more attractive purchase.

In the 2019, the median price gap between freehold and leasehold properties was 9.8%. As of 2H 2024, this has narrowed to 1.3%.

Table 2: Median Price psf of Freehold Condos in 1H 2024

Source: URA as of 6 Aug 2024, ERA Research and Market Intelligence

There were 2,264 freehold condominium units that changed hands in 1H 2024, with the average age and price psf of unit being 14.8 years and $1,953 psf respectively.

43.0% of these transactions were for homes between 10 to 20 years old, as buyers consider the trade-off between age and affordability. The lower psf would mean buyers have a relatively newer and larger home for the same price quantum.

Chart 2: Freehold Condominium Transactions in 1H 2024

![]()

Source: URA as of 31 Jul 2024, ERA Research and Market Intelligence, New sale project’s age based on estimated TOP date

Should buyers be concerned with the slower price growth of Freehold Properties?

We often see 99-LH properties outperforming freehold/999-LH property in terms of profitability. This is a result of lower frequency of transactions for freehold homes.

Freehold property owners are likely to be living there long term. They lack the urgency to sell them as there is no lease decay. Moreover, as the government continues to roll out 99-LH GLS sites, there are more 99-LH properties transacted which leads to more price movement. These newer developments are sold at higher prices, which leads to faster and higher price growth.

Hence, prices of freehold developments may experience more gradual growth as the proportion of transactions are comparatively lower than 99-LH developments. However, in the long term, freehold developments provide better value retention, as they are not subject to lease decay.

Conclusion

Are freehold properties right for you?

If you are willing to pay more for the freehold tenure, then you should have the intention to hold onto it for the long term. If you are looking to cash out the profits from your property after a few years (e.g. Upon new home completion or the end of the 3-year Sellers’ Stamp Duty period), then there is little difference between buying a freehold and 99-LH property.

What are my options?

There are still many opportunities in the market for new freehold developments that cater to most budgets, or locational preferences.

For value buys, you can consider Kassia in Flora Drive, with a price starting from just $1,830 psf. Those who want to be in the city fringe can consider The Arcady at Boon Keng, just a short walk from Boon Keng MRT Station. In the West Coast, Terra Hill offers a compelling proposition being nestled in a tranquil landed enclave, yet near an MRT station. The Continuum offers East-siders a mega-development, that comes with more comprehensive facilities in a popular area.

For those looking to live in a quiet and exclusive enclave can consider buying a boutique development. There are four new developments available, with three in the east and one in the west. Comparatively, they are priced lower than the larger freehold developments nearby.

Table 3: List of Available Freehold Developments

| Development |

Region/Area |

No. of Units |

Price psf from ($) |

Distance to nearest MRT Station |

| Kassia |

OCR/Pasir Ris |

276 |

1,838 |

1.8km to Tampines East |

| The Shorefront |

OCR/Pasir Ris |

23 |

1,779 |

1.8km to Pasir Ris |

| The Arcady at Boon Keng |

RCR/Boon Keng |

172 |

2,419 |

500m to Boon Keng |

| Terra Hill |

RCR/Pasir Panjang |

270 |

2,251 |

400m to Pasir Panjang |

| The Continuum |

RCR/East Coast |

816 |

2,592 |

800m to Dakota |

| Ardor Residence |

RCR/East Coast |

35 |

2,114 |

1.2km to Marine Parade |

| Straits at Joo Chiat |

RCR/East Coast |

16 |

2,080 |

1km to Eunos |

| The Hillshore |

RCR/Pasir Panjang |

59 |

2,227 |

2.1km to Pasir Panjang |

Source: ERApro as of 3 Sep 2024, ERA Research and Market Intelligence

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

In recent months, land bids for Government Land Sales (GLS) sites have fallen, with noticeably lower participation by developers. In the first five months of 2024, the average number of developers bidding for awarded sites with residential use fell to 2.4, down from 3.4 in 2H 2023 and the peak of 8.6 in 2021.

Chart 1: Average number of bidders for GLS sites*

Source: URA, ERA Research and Market Intelligence, *Sites zoned ‘Residential (Non-landed)’, ‘Residential and Commercial’, ‘Residential with Commercial on 1st storey’ and ‘White’

Land bids in recent months have been comparatively lower than those for previously sold sites that share similar locational attributes. The media has reported that some sites sold were sold at prices “below analyst’s predictions”. Moreover, the Marina Gardens Crescent site was not awarded as the $984 per square feet per plot ratio (psf ppr) was “too low”.

Below are some examples of recent GLS residential sites that sold for up to 32.0% less than some neighbouring developments.

Table 1: Recent GLS sites awarded previously and recently in similar locations

Source: URA, ERA Research and Market Intelligence 1. The site is zoned Residential with Commercial at 1st Sty. 2. Sites are in different districts, but are just 150m apart.

Could this change signal waning demand for GLS sites? Are developers exercising more caution? Will new launch prices finally fall?

Below, we explore the answers to these questions through the lens of 4 recent GLS sites, alongside the reasons why developers are unlikely to cut new launch prices.

Reason #1: The floor area harmonisation rule reduces sellable floor area in a development

Applying to all residential and industrial GLS sites launched for sale from 1 September 2022 onwards, the new Floor Area Harmonisation rule will see the following changes implemented:

- The Urban Redevelopment Authority, Singapore Land Authority, Building and Construction Authority and Singapore Civil Defence Force will measure all floor areas to the middle of the wall

- All strata areas will be included in Gross Floor Area (GFA).

- All voids will be excluded from the strata area.

As a result of these changes, spaces like air-con ledges and voids are no longer included as sellable spaces. But developers are unlikely to lower selling prices, even if they pay less for land. To put things into perspective, developers do incur expenses building void spaces and aircon ledges and hence they are likely to incorporate related costs into the selling price.

Table 2: Land prices for projects launched before and after the floor area harmonisation rule

Source: URA, ERA Research and Market Intelligence* Site is zoned Residential with Commercial at 1st Sty.

A case in point is Lentor Mansion, where units launched after the floor area harmonisation rule are priced higher per square foot than units of similar size and design at Lentor Modern. This is despite Lentor Mansion’s lower land cost of $985 psf ppr, compared to Mentor Modern’s $1,204 psf ppr (18.2% difference).

Table 3: Price difference for 2-bedroom units at Lentor Modern and Lentor Mansion

Source: URA, ERA Research and Market Intelligence

Reason #2: Developers expected to undertake higher risks for some sites

Higher Additional Buyer Stamp Duty (ABSD)

Since the Cuscaden Road site was awarded in May 2018, there has been three rounds of ABSD hikes on foreign buyers, raising the original rate to a hefty 60%. With developments in the Core Central Region (CCR) typically seeing more foreign buyers, developers are becoming more conscious about waning demand. Hence, they are lowering their bids to account for the current market conditions.

Image 1: Timeline of increases in ABSD for foreign buyers (non-Singapore permanent resident)

Source: IRAS, ERA Research and Market Intelligence

As demand from foreign buyers was high before July 2018, the developer of Cuscaden Reserve was more bullish in their bids.

However, with the market now cooled, developer sentiments are substantially dampened, resulting in the top bid for the Orchard Boulevard site being 32% lower than Cuscaden Reserve’s.

Depending on market conditions, further revisions to the ABSD rate could happen.

Consequently, developers must factor in such regulatory risks that could affect sales of units; this might involve setting aside funds for marketing or contingency costs.

Business risks arising from a new rental housing typology

Driven by evolving demographics and rising demand for rentals amongst Singaporeans, the URA recently introduced a new class of long-stay serviced apartments (SA2) in several of their newly released GLS sites.

With a minimum stay of three months, SA2s are intended to cater to tenants in need of housing for a period lasting longer than a typical hotel stay, but shorter than the usual 1-year lease for local rentals. Potential tenants for SA2 apartments may include foreigners on extended job stints, some younger Singaporeans who may choose to rent as a start, and homeowners waiting out their home completion or renovation.

Developers undertaking SA2 projects are required to either have hospitality expertise or to partner with parties with relevant capabilities. Furthermore, being an untested market, it may be challenging for developers to determine the demand for properties built under this new rental housing typology.

Zion Road, Parcel A (Source: Google Maps)

The Zion Road (Parcel A) site is the first site to pilot the new SA2 flats. It was sold for $1 billion ($1,202 psf ppr), 30.6% lower than the site sold at Jiak Kim Street (now Rivière), which sold for $955.4 million or $1,733 psf ppr in 2018.

Nevertheless, even with the comparatively lower land cost, developers for Zion Road (Parcel A) are not expected to reduce selling prices. On the contrary, they could even factor in holding costs and possible vacancies of the SA2 units, given uncertainty about their future profitability.

Larger projects may present higher risk of unsold units

Treasure at Tampines (Source: Sim Lian)

Although large residential projects offer enticing benefits like larger total revenues and potentially lower construction costs due to economies of scale, they can also be fraught with risks for developers who choose to tender for larger GLS sites. The Zion Road (Parcel A) site has a maximum GFA of 85,577 sqm, potentially yielding 735 units (excluding SA2 units). Meanwhile, the 455-unit Riviere’s GFA is only 51,231 sqm, 40.1% less.

This heightened risk traces back to Singapore’s policy of imposing ABSD on unsold units. Under this regulation, developers who fail to sell all units within five years of acquiring a GLS site face a hefty penalty of up to 35% of the land cost.

This need to manage risk associated with unsold stock makes developers unwilling to lower selling prices, even with lower land costs. Instead, they are more likely to maintain prices in exchange for managing common challenges associated with large projects. These challenges include longer construction runways and more rigorous project requirements.

Reason #3: Surge in construction demand could drive construction and labour costs higher

At present, Singapore’s construction industry is experiencing strong demand for public and private projects. The total projected contract value is between $32 billion and $34 billion in 2024, the highest since 2015.

Chart 2: Construction demand in Singapore

Source: data.gov.sg, ERA Research and Market Intelligence

Key contributors to construction demand include private sector projects from GLS site tenders and the expansion of Singapore’s two integrated resorts. Similarly, public projects like HDB Build-to-Order (BTO) flats, the Cross-Island MRT line, Changi Airport Terminal 5, and Tuas Port have also significantly contributed to this growth in demand.

This momentum is expected to continue with the Building and Construction Authority forecasting a steady rise in demand to reach between $31 billion and $38 billion per year from 2025 to 2028. This translates into an increase of between 4.7% to 28.4% on the 10-year average of $29.6 billion.

With the increased volume of construction, competition for labour and materials has intensified. The Tender Price Index, which tracks the price movement of construction components such as materials and manpower, has grown by 32.4% between 2020 and 2023.

Although labour pressure has eased with approximately 40% more work permits issued for the construction, marine shipyard, and process industries, skilled labour shortages could remain a significant constraint.

Other cost pressures, such as higher-for-longer interest rates, persistent inflation, higher Goods & Services Tax, and heftier property taxes due to higher land values, also make price cuts from developers unlikely.

Additional Costs for Sustainability Considerations

In line with the cost-push factors highlighted above, developers could also incur extra expenditure due to certain requirements for the awarded GLS sites. These requirements incur additional consultancy and surveying fees for special impact assessment studies which adds to the developers’ costs. Examples of recent GLS sites necessitating special impact assessments are Upper Thomson (Parcel B).

Image: Upper Seletar Reservoir

Due to Upper Thomson (Parcel B)’s proximity to the Central Catchment Nature Reserve, developers must incorporate biodiversity-sensitive strategies as part of their proposed developments. This is to ensure Springleaf’s rich biodiversity is protected, as well as to strengthen ecological connectivity along the Khatib Nature Corridor.

Additionally, the site houses a conserved building, the former Seletar Institute, and an open communal space that must be restored and integrated into the resulting residential development.

So, what could cause new home prices to fall?

In the event that new home prices decline, we posit two reasons that could result in such an outcome.

A major economic shock leading to a decline in household income

Major economic shocks, leading to job losses and declining household income, may trigger price corrections in Singapore’s property market. This is evident from past cycles where the property market saw adjustments during the three major financial crises since the 1980s. Since then, the Government has implemented multiple rounds of cooling measures, as well as tightened borrowing conditions to encourage financial prudence.

Chart 3: GDP growth versus Property Price Index

Source: Singstat, ERA Research and Market Intelligence

Singapore starts experiencing a decrease in population

Like many developed countries, Singapore is experiencing an aging population with more than half of Singapore’s residents aged 65 years or older. Currently, the country’s working population is bolstered by non-residents who play a vital role in sustaining an aging workforce. Unless the government tightens its foreign labour policy, Singapore is unlikely to see a substantial population decline in the medium term, a factor that could influence housing demand, and by extension, new home prices.

Chart 4: Total Population versus Proportion of Singapore Residents (65 years and older)

Source: Singstat, ERA Research and Market Intelligence

Conclusion: Lower land costs may not necessarily translate into lower selling prices for upcoming new launches in the foreseeable future

While lower prices for GLS sites in the past year may appear to point towards lower new launch prices on the horizon, this is unlikely to be the case in the current market, as well as for the foreseeable future.

Although comparatively lower GLS site prices were observed in the past year, as seen through the examples above, this trend is unlikely to persist in the current market or the near future.

At present, lower land bids by developers can be attributed mostly to growing project costs and risk premiums. This is especially so for larger projects and those incorporating new home typologies or criteria.

Due to these factors, developers are more cautious about their land bids, and more selective about the sites they are bidding on. However, developers are expected to keep prices for new launches steady – as they undertaking greater risks while balancing buyer’s affordability.

Furthermore, with more GLS sites being awarded since 2021, many developers now possess ample land stock and are focusing on selling their existing new home supply. Unless the upcoming GLS sites possess attractive qualities (e.g. proximity to amenities or good schools nearby), they will be unlikely to attract a large number of bids by developers, much less aggressive ones. This raises the likelihood of GLS land prices staying stable for the foreseeable future.

This stability in land prices, suggests that private home prices are likely to remain steady; this aligns with URA’s goal of meeting homebuyer demand and achieving market stability, thus ensuring a healthy, well-balanced property market going forward.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Picture this: You end a long day of work, and step foot into the mega-development you call home. You are immediately greeted by the familiar sights and sounds of children frolicking about, enjoying their playtime in the estate gardens and the splash pools as the sun sets.

Their parents, who are watching closely, are chatting among themselves. Meanwhile, other residents are seated in an airy alfresco pavilion, catching up with their friendly neighbours over a delicious potluck dinner.

Not everyone may find such a view welcoming – but if you are drawn to the dynamic and vibrant nature of large, urban communities – life in a mega-development may just be the thing for you.

The Treasure@Tampines is an example of a mega-development condo, with over 2,000 units

What is a mega-development condominium?

Mega-developments are condominiums that house 800 or more units. A prime example of a mega-development is the Treasure @ Tampines, home to an astounding 2,203 units.

Mega-developments are generally seen as a fantastic option for owner-occupation properties. The expansive land area permits upscale amenities, while the significant number of units maintains a lower maintenance cost.

There are two current mega-developments available, located in District 15. Furthermore, 2024 will see a further three expected mega-development launches. These include a project in the Rest of Central Region (RCR) and two in the Outside Central Region (OCR). All three developments have 99-year tenures.

Table 1: Current and upcoming Mega-developments launching (2024)

Source: ERA Research and Market Intelligence, ERA Project Marketing

Today, we explore the pros and cons behind living in a mega-development, and who are the buyers that will find value staying in one.

Mega-developments offer more facilities – at a lower maintenance cost

There is an age-old saying: “The bigger, the better.” To a certain extent, this is true for large-scale residential projects in Singapore, particularly mega-developments.

Mega-developments occupy large sites, allowing for more common facilities. To illustrate, the Treasure @ Tampines houses 128 facilities, including an aqua aerobic pool and a trampoline courtyard. By contrast, the Alps Residences, another project within the same district (D18), has only 31 facilities.

Even though residents of mega-developments get to enjoy a wider selection of facilities, the maintenance fees payable tend to be on the lower end, as they benefit from economies of scale, with more residents contributing to maintenance fees.

We conducted a study comparing the maintenance fees payable for three notable mega-developments to another three mid-sized developments within the same districts. Firstly, the three mega-developments offer up to an impressive 128 facilities. Secondly, residents of mega-developments could pay between 7% – 26% lower maintenance fees than mid-sized developments.

Table 2: Comparison of maintenance fee and number of facilities

Source: ERA Research and Market Intelligence

Mega-developments offer a vibrant and dynamic environment

Life in a mega-development is always vibrant and lively – there is never a dull moment as there is always something going on in the estate!

Mega-development condominiums offer a wide range of amenities. From common amenities such as swimming pools and exercise areas to unique offerings like jamming studios and virtual golf rooms, mega-developments have something for everyone.

This creates opportunities for interaction among community members. Young children will have no shortage of peers to socialise with at the many playgrounds and child play areas. Adults can enjoy the many fitness facilities and communal areas for work-from-home arrangements. Seniors in particular benefit from the vibrant community and activities to keep themselves active and occupied. This makes mega-developments a fantastic choice for multi-generational families.

Mega-developments feature a vibrant community, especially for young children

Mega-developments are a fantastic property choice for people who enjoy hosting. From barbecue pits to tennis courts, the countless facilities found in a mega-development are sure to make guests of all ages feel welcome and entertained.

There are also regular events and activities organized by the management corporation of these large developments. Fancy joining a Easter egg hunts or a Mid-Autumn Festival walk around the development and bonding with your neighbours at the same time? One can expect higher participation rate than in a regular condominium. This will provide management with more resources to plan these events, resulting in more frequent and larger scale events that provide fun and enrichment for residents.

Mega-developments make a worthwhile investment property

Mega-developments typically see a high number of transactions. This is due to the sheer number of units of various sizes and configurations available.

Given the size of these mega-developments, the likelihood of a transaction happening in the development is higher, as there are more units available. With higher sales frequency, we can expect healthier price growth.

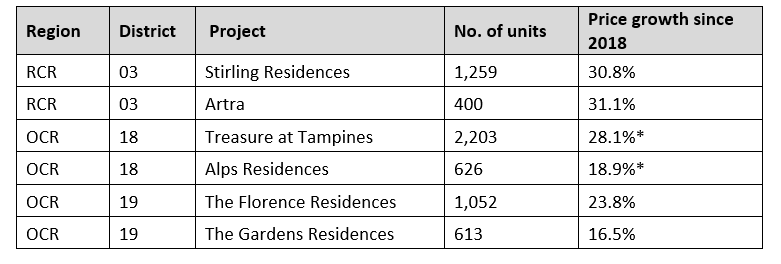

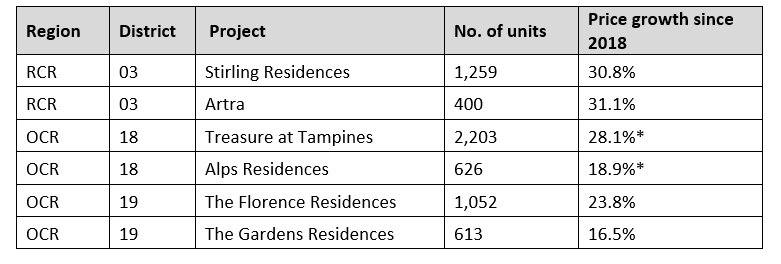

Comparing our three earlier examples of mega-developments and smaller developments in the same district, we can conclude that mega-developments generally see better price growth.

Table 3: Comparison of Price Performance

Source: URA as of 17 May 2024, ERA Research and Market Intelligence *From 2019, when Treasure at Tampines was launched

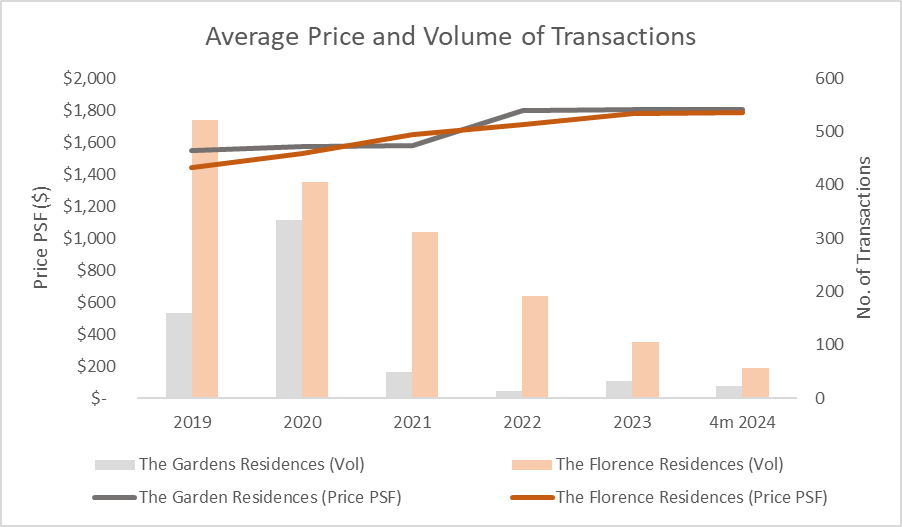

A deeper dive comparing the two District 19 projects, The Gardens Residences and The Florence Residences (mega-development) further illustrates this. We can observe how the sheer number of units and transactions a mega-development can contribute to a healthy price growth.

Chart 1: Example of Mega-developments vs a smaller development in District 19

Source: URA as of 17 May 2024, ERA Research and Market Intelligence

While mega-developments offer many upsides, there are a few cons that might make them unsuitable for some property buyers.

Privacy-conscious homebuyers may find mega-developments unsuitable

The first and most obvious drawback is the lack of exclusivity. Mega-developments may not be for you if you prefer a more private and quieter environment, as there is an almost perpetual state of activity going on, with people walking around, children playing, and noise being made.

There is also a higher likelihood of units being bought and sold within mega-developments. This leads to people constantly shifting in and out, and regular renovations, which might feel disruptive for residents.

The high level of activity in mega-developments could be disruptive to those who prefer a quieter, more privacy-conscious lifestyle

Buyers that idealise a private and quiet atmosphere would find something like a boutique development, which has less than 100 units more desirable to live in, as compared to the sprawling size of a mega-development.

Facilities might end up under-utilised or under-maintained

While mega-developments pride themselves on the large number of facilities they have to offer, they are not always in use by residents. This is especially true for less-used facilities (such as virtual golf rooms, or jamming studios), which often find themselves under-utilised and under maintained.

Due to the large number of residents using the facilities in mega-development condos, they require more frequent upkeep.

Popular facilities such as swimming pools or children’s playgrounds that see regular usage are also likely to degrade faster, requiring more frequent upkeep.

Due to the large size of these projects, it is not uncommon to see run-down areas, a side-effect of the struggle to keep such a large estate in good condition. This is especially true the older these developments get.

Mega developments are crowded and sometimes inconvenient

The larger number of people that stay in mega-developments results in more competition to use popular facilities. Tennis courts and function rooms often have to be booked in advance through an online process with limited slots. Free-use facilities such as lap pools and gyms are often be packed, especially during peak hours.

Residents might have to find themselves visiting these facilities at weird timings just to avoid the crowd, which takes away the convenience factor of having in-house facilities.

The large number of residents often results in long wait times for the lift

This aforementioned waiting time caused by crowds also spills into other common areas, notably lifts and parking areas. Lifts in mega developments are often slow, due to the sheer number of people that use them. Bear in mind that with more residents comes more food delivery riders, couriers, and movers, who all share the use of the same lifts.

Those who drive to work also feel the brunt of the crowd when leaving the compound in the morning. With a large number of people trying to leave the condo through the same egress points, residents are bound to run into ‘traffic congestion’ even before exiting the premises.

Is a Mega-Development Right for Me?

Based off these aforementioned factors, we can conclude that mega-developments are fantastic, value-for-money properties, both for owner-occupancy and as an investment property.

They make an excellent choice for families with children, as they have the most to benefit from the diverse range of facilities available right at their doorstep. Fancy the idea of an entire day of entertainment – without the need to leave the front gate!

The lively atmosphere inside these mega-developments also make them a fantastic option for older folks who are downgrading. Chock full of activities and amenities, they provide seniors with the activity level, friends and community needed to keep them engaged and to prevent them from feeling lonely.

Mega-development homes are fantastic choice for multi-generational families

These facilities have proven to evolve along with the needs of its many residents. A fantastic example of this are newer developments creating communal spaces that are conducive towards and can function as co-working spaces for people with remote working arrangements – a trend that is common these days.

Facility bookings are often done via smartphone apps nowadays, which adds to the ease of access and convenience that residents of these mega-developments can enjoy.

Offering a fantastic value proposition alongside a multitude of lifestyle factors built into the property itself, it is no wonder why mega-developments are on the rise, and why you should strongly consider one as your next property purchase.

To find out more about the upcoming mega-development launches, speak to an ERA Trusted Adviser today.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

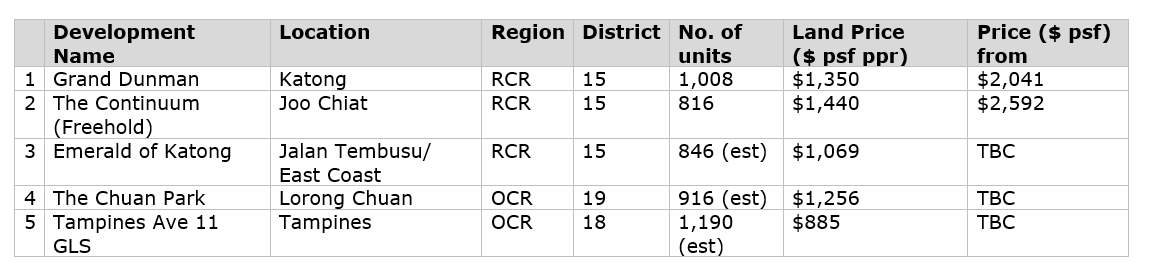

District 15 possesses a unique blend of heritage, convenience and quietness. It has always been lauded by Easties as one of the best places to live in Singapore.

Being a location well loved by both locals and expats alike, District 15 has always been a popular district among homebuyers. This is due to the allure and unique lifestyle offered by the seafront living experience.

If you have always dreamed of living along the East Coast, here’s your chance! There are several District 15 New Launch condos available on the market right now – which could end up becoming your dream home.

Table 1: New projects on sale in District 15

| Development | Street | Tenure | No. of Units | Price PSF starting from ($) |

| Grand Dunman | Dunman Road | 99-LH | 1,008 | $2,041 |

| Straits at Joo Chiat | Joo Chiat Place | FH | 16 | $2,080 |

| Ardor Residence | Haig Road | FH | 35 | $2,114 |

| Tembusu Grand | Jalan Tembusu | 99-LH | 638 | $2,174 |

| Claydence | Still Road | FH | 28 | $2,300 |

| Atlassia | Joo Chiat Place | FH | 39 | $2,388 |

| The Continuum | Thiam Siew Avenue | FH | 816 | $2,592 |

| Meyer Blue | Meyer Road | FH | 226 | Yet to launch |

| Emerald of Katong | Jalan Tembusu | 99-LH | 846 | Yet to launch |

Source: ERApro as of 14 May 2024, ERA Research and Market Intelligence

What’s There in District 15?

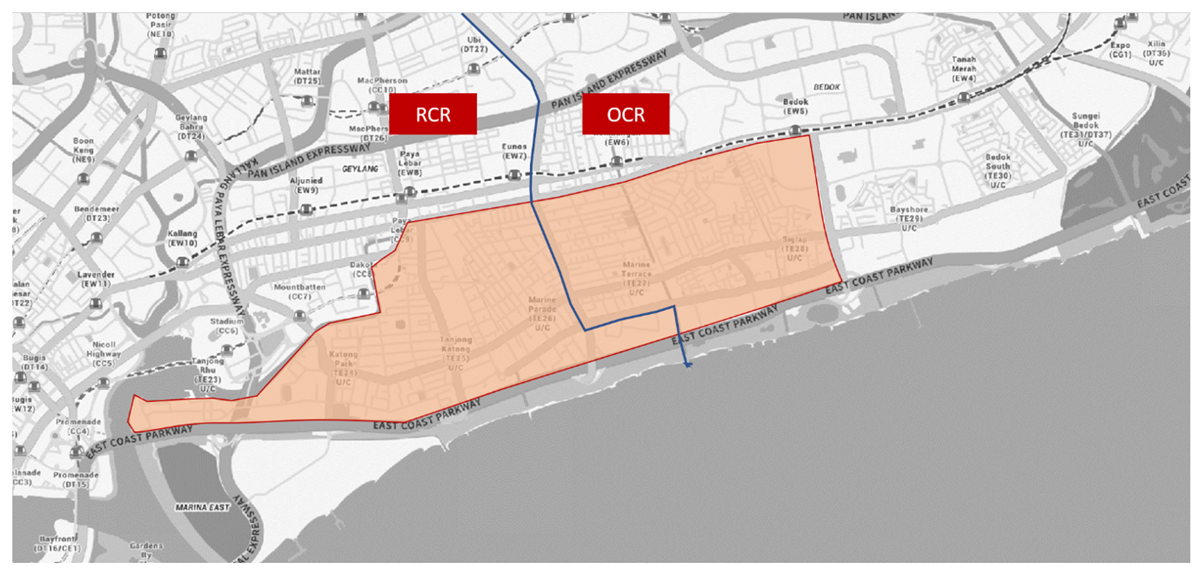

When someone says they live in a property with a sea view, areas such as “East Coast”, “along Siglap” or “the Marine Parade area” come to mind. These areas fall under District 15, where residents staying in high floor units often get to enjoy an immaculate view of Singapore’s South-Eastern coastline and East Coast park.

Source: Map data ©2019 Google, ERA Research and Market Intelligence

While people often associate East Coast Park with District 15, it does not include the entire 18km of reclaimed coastline. Located in both the Outside Central Region (OCR) and the Rest of Central Region (RCR), its locale includes Amber Road, East Coast, Joo Chiat, Katong, Marine Parade, Meyer, and Tanjong Rhu.

There is also a large landed enclave and many small developments scattered across the district, creating a quiet and exclusive atmosphere. In addition, much of the land at Meyer Road and Amber Road has a 999-year or freehold lease, a legacy from the 1800s. At the same time, these areas are within walking distance of amenities, making District 15 a highly coveted estate to live in.

Amenities and Conveniences in District 15

District 15 is home to the famous and history-rich areas of Joo Chiat and Katong. Populated by colonial shophouses, these iconic buildings are now famous for their lifestyle offerings amongst locals and the expat community, with cafes, bars, restaurants, and well-known eateries. There are also several popular schools in the district, such as Victoria School and CHIJ Katong Convent.

Great for nature, exercise and pet lovers

District 15 is a fantastic area to stay in if you are a pet lover. Areas such as Joo Chiat and Tanjong Katong are home to a variety of pet stores and vet practices. This ensures that your animal companions’ needs are always cared for.

There is also a high density of dog-friendly cafes and restaurants in the area. East Coast Park is another highlight for dog owners, as it is not only a fantastic place to walk your dog, but also houses the largest dog run in Singapore. A dog swimming pool, and a pet megamart can also be found there.

The park comes to life, especially on evenings and weekends. From cyclists and fitness enthusiasts, the vast park is home to people of all interests. There are also a variety of food options available, notably seafood restaurants, where families in the area often go to for their meals.

District 15 is seeing improved connectivity in 2024

Previously, the East Coast area used to be ‘neglected’ in terms of connectivity, without access to an MRT line. Partly due to reclaimed land requiring time to settle, there were only bus services to shuttle residents to their workplaces in the city centre or other parts of Singapore.

However, the eastern region of the Thomson-East Coast Line (TEL) will soon be ready by June 2024. It will connect passengers from Bayshore in the East to Woodlands in the North via the Central Business District.

Future plans

It is likely that further changes will come to the area in the future. This is part of the Government’s proposed “Long Island” plan to marry coastal protection measures with new homes, coastal parks, and recreational spaces.

Along the East Coast Parkway, east of District 15, Bayshore will be developed as a smart and sustainable car-lite estate with amenities and recreational spaces. Homes will have sea views. The East Coast Green Corridor will run through this town. This will provide residents with another 20km of upcoming coastal and waterfront parks.

Price Performance

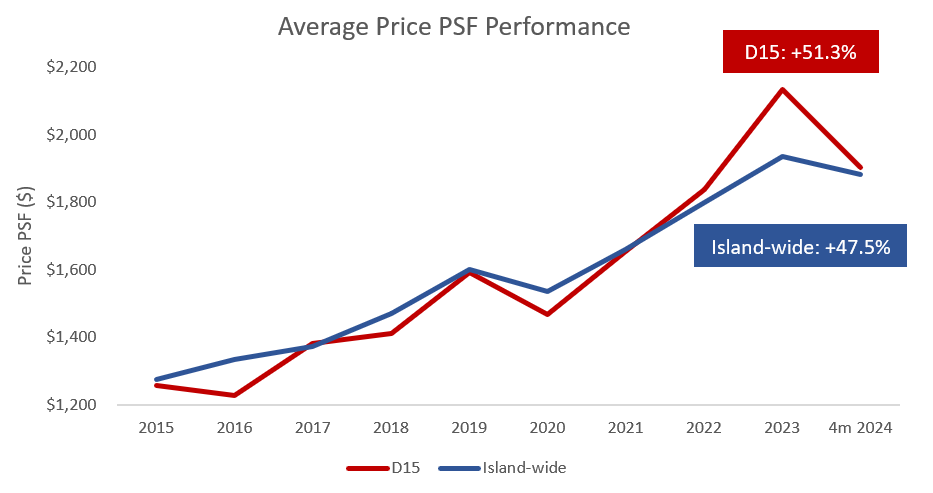

District 15 has outperformed island-wide, in terms of average price per square foot (psf) of units transacted (see Chart 1). Historically, there has been a high demand for homes in District 15 due to its unique location. This has led to people flocking to buy both new and resale properties there.

Chart 1: Price performance of non-landed properties in District 15.

Source: URA as at 14 May 2024, ERA Research and Market Intelligence

We can also expect to see further price uplifts from the MRT effect, with Phase 4 of the TEL set to be opened in June 2024.

As District 15 becomes more connected through enhanced transportation infrastructure and improved amenities, both current owners and potential buyers can anticipate a significant increase in property value and quality of life.

Conclusion

Based on ERA’s proprietary data between 2021 and April 2024, 56.8% of buyers of District 15 new launches were previously living in the East.

For those who live in the East and proclaim “East side, best side”, many of their reasons to support this claim can be traced back to District 15.

If you would like to become an Eastie too, now is the perfect time to make your wish come true. The current inventory of new launch condominiums available will suit the criteria of any buyer. It includes exclusive boutique developments of as small as 16 units (the Straits at Joo Chiat) to sprawling mega developments that house up to 1,008 units (Grand Dunman).

The majority of these new launches are also freehold properties, which is a definite plus for most buyers. To find out more, check out the ERA Projects Online Gallery here, or speak to an ERA Trusted Adviser today!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.