Freehold land parcels were last sold prior to the introduction of GLS Programme in 1967, mostly taking place before Singapore’s independence. If all Government Land Sale (GLS) sites have a 99-year leasehold (99-LH) tenure, then why are there 999-year leasehold (999-LH) or freehold developments?

In land-scarce Singapore, selling residential land on a 99-year lease allows the government flexibility to reallocate land in the future, and to meet the evolving needs of society.

Freehold Land is a Rare Commodity

Currently, new freehold developments are available as property developers purchase freehold land via the collective sale of older projects. Such new projects are rare and remain highly sought after, as they are not subject to lease decay. This makes them an attractive option for buyers looking to purchase a property for their own stay, or as a legacy asset.

Given a quiet en-bloc market with an abundance of sites released in the 2024 GLS Confirmed List, new freehold condos are becoming increasingly scarce. Developers are unlikely to pay a sizable amount for a freehold site that comes with more encumbrances and costs (e.g. demolition), especially with the wide array of sites available under the GLS scheme. With a slow en-bloc market, particularly for freehold sites, there will be a dearth of new freehold units available in the near future. Only 603 freehold units are expected to be launched in the coming months.

When purchasing any property, buyers often have to face an iron triangle – a form of ‘give-and-take’ regarding the attributes of a property. In this case, the balance lies between the age of a property, its locational attributes (e.g. the availability of MRT stations), and lastly affordability. Freehold developments are often on the pricier end, which might make the ‘perfect’ freehold property more elusive to attain.

This coincides with ERA’s recently concluded My Dream Home Survey, which found that homebuyers prioritise affordability, size of the property and proximity to public transportation as key considerations for their next home purchase. Among survey participants keen on owning a private property as their next home, over 55% indicated a preference for new launches.

Where are FH condos usually located?

Freehold condos are spread across island-wide. However, there is a higher concentration of them in the city centre (e.g. Orchard, River Valley, Bukit Timah, Newton and Novena) or the city fringe (e.g. Katong, Joo Chiat, Marine Parade, Upper Bukit Timah). In line with Singapore’s urban development, these more centrally located areas were developed first, before moving outwards. Naturally, being centrally located, these developments would command higher prices.

While freehold properties are also found in suburban areas such as in Serangoon or Pasir Ris, their supply is more limited. These areas were developed much later, with land sold with leasehold tenures under the GLS programme.

Furthermore, MRT stations were also planned after the GLS Programme was introduced. Therefore, much of the land near MRT stations would have a leasehold tenure, barring those sold prior to the stations being planned.

Terra Hill, a freehold development located just 400m from Pasir Panjang MRT Station

ERA estimates approximately some 44% of non-landed homes to be of freehold or 999 leasehold status, relatively well distributed across market segments. But with the introduction of GLS program, this has helped ramped up the supply of leasehold homes, particularly in the Outside Central Region (OCR). Even though the supply of freehold units in the OCR has remained largely the same, the proportion of such homes in the region has dwindled to 28% due to the growing number of leasehold properties over time.

Table 1: Breakdown of Units by Tenure

Source: URA, ERA Research and Market Intelligence

Why do buyers prefer a new development despite the freehold tenure?

While older resale condos are typically more affordable than freehold properties in the same location, they could come with higher renovation and maintenance costs.

The older unit and development might not be well-maintained, and having outdated building designs and dreary façades could make them unappealing. Additionally, aging facilities that are under-utilized or poorly maintained due to wear and tear might be unpleasant to use or even pose safety risks.

Freehold property owners pay a premium for perpetual ownership. Unless the maintenance cost of their unit or the development becomes too high, it is unlikely that they will want to sell, whether individually or via a collective sale.

If the development’s age is a concern, or if buyers prefer a newer property, they may need to scour the market to find what they are looking for, or pay close attention to the en-bloc market. After all, freehold developments are becoming harder to come by as the years go on.

Entry Price

Are freehold properties still affordable? Despite commanding a premium, freehold properties are still alluring to many buyers as they offer perpetual ownership. Without the threat of lease decay, freehold properties also retain their value better over time.

Chart 1: Median Price psf for Freehold vs 99-Leasehold

Source: URA as of 7 Aug 2024, ERA Research and Market Intelligence, FH transactions include 999-LH

Furthermore, with the closing gap in prices between freehold and leasehold properties, prospective homebuyers may find freehold homes to be a more attractive purchase.

In the 2019, the median price gap between freehold and leasehold properties was 9.8%. As of 2H 2024, this has narrowed to 1.3%.

Table 2: Median Price psf of Freehold Condos in 1H 2024

Source: URA as of 6 Aug 2024, ERA Research and Market Intelligence

There were 2,264 freehold condominium units that changed hands in 1H 2024, with the average age and price psf of unit being 14.8 years and $1,953 psf respectively.

43.0% of these transactions were for homes between 10 to 20 years old, as buyers consider the trade-off between age and affordability. The lower psf would mean buyers have a relatively newer and larger home for the same price quantum.

Chart 2: Freehold Condominium Transactions in 1H 2024

![]()

Source: URA as of 31 Jul 2024, ERA Research and Market Intelligence, New sale project’s age based on estimated TOP date

Should buyers be concerned with the slower price growth of Freehold Properties?

We often see 99-LH properties outperforming freehold/999-LH property in terms of profitability. This is a result of lower frequency of transactions for freehold homes.

Freehold property owners are likely to be living there long term. They lack the urgency to sell them as there is no lease decay. Moreover, as the government continues to roll out 99-LH GLS sites, there are more 99-LH properties transacted which leads to more price movement. These newer developments are sold at higher prices, which leads to faster and higher price growth.

Hence, prices of freehold developments may experience more gradual growth as the proportion of transactions are comparatively lower than 99-LH developments. However, in the long term, freehold developments provide better value retention, as they are not subject to lease decay.

Conclusion

Are freehold properties right for you?

If you are willing to pay more for the freehold tenure, then you should have the intention to hold onto it for the long term. If you are looking to cash out the profits from your property after a few years (e.g. Upon new home completion or the end of the 3-year Sellers’ Stamp Duty period), then there is little difference between buying a freehold and 99-LH property.

What are my options?

There are still many opportunities in the market for new freehold developments that cater to most budgets, or locational preferences.

For value buys, you can consider Kassia in Flora Drive, with a price starting from just $1,830 psf. Those who want to be in the city fringe can consider The Arcady at Boon Keng, just a short walk from Boon Keng MRT Station. In the West Coast, Terra Hill offers a compelling proposition being nestled in a tranquil landed enclave, yet near an MRT station. The Continuum offers East-siders a mega-development, that comes with more comprehensive facilities in a popular area.

For those looking to live in a quiet and exclusive enclave can consider buying a boutique development. There are four new developments available, with three in the east and one in the west. Comparatively, they are priced lower than the larger freehold developments nearby.

Table 3: List of Available Freehold Developments

| Development |

Region/Area |

No. of Units |

Price psf from ($) |

Distance to nearest MRT Station |

| Kassia |

OCR/Pasir Ris |

276 |

1,838 |

1.8km to Tampines East |

| The Shorefront |

OCR/Pasir Ris |

23 |

1,779 |

1.8km to Pasir Ris |

| The Arcady at Boon Keng |

RCR/Boon Keng |

172 |

2,419 |

500m to Boon Keng |

| Terra Hill |

RCR/Pasir Panjang |

270 |

2,251 |

400m to Pasir Panjang |

| The Continuum |

RCR/East Coast |

816 |

2,592 |

800m to Dakota |

| Ardor Residence |

RCR/East Coast |

35 |

2,114 |

1.2km to Marine Parade |

| Straits at Joo Chiat |

RCR/East Coast |

16 |

2,080 |

1km to Eunos |

| The Hillshore |

RCR/Pasir Panjang |

59 |

2,227 |

2.1km to Pasir Panjang |

Source: ERApro as of 3 Sep 2024, ERA Research and Market Intelligence

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

For almost anyone doing it for the first time, buying a home in Singapore can be a confusing process. Throw in a bunch of acronyms, like ABSD (Additional Buyer’s Stamp Duty) and MOP (Minimum Occupation Period), and things can get baffling real quick. However, if you’re intending to take out a loan on a new home purchase, two terms that you’ll absolutely need to know are TDSR and MSR.

In their full form, TDSR stands for ‘Total Debt Servicing Ratio’, whereas MSR means ‘Mortgage Servicing Ratio’, and they’re both Government initiatives to promote responsible borrowing. Below, we explain how TDSR and MSR came about, their purpose, and how to determine your housing affordability using both ratios.

What exactly are TDSR and MSR? And how did they come to be?

Introduced by the Monetary Authority of Singapore (MAS) in 2013, the TDSR is a framework applying to all property loans extended by banks to borrowers. Its rollout is to promote prudency amongst individuals taking loans, so that they don’t end up borrowing more than they could afford.

Therefore, the TDSR, which limits debt repayments to a certain percentage of gross monthly income, is first and foremost a safety net. When the TDSR was first introduced in 2013, borrowers were allowed to spend up to 60% of their gross monthly income on loan servicing.

Subsequently, that limit was tightened to 55% in 2021. Put differently, this means that under TDSR guidelines, a borrower should have a total debt value of under 55% of his or her monthly salary to be able to take out a mortgage.

Similarly, for the MSR, it places a cap on the percentage of monthly income that borrowers can use for mortgage repayments. In 2013, the MSR threshold was set at 30% for HDB flat purchases that are financed by bank loans, and it has stayed that way since.

How are TDSR and MSR applied differently for home purchases?

If there’s a key difference between TDSR and MSR that’s worth highlighting, it’s that TDSR applies to all types of housing loans, whereas MSR applies only to loans for buying an HDB flat OR an Executive Condominium (EC) that still hasn’t completed its MOP.

Hence, supposing that you’re a homebuyer who wishes to take out a home loan for an HDB flat or EC purchase, you’ll have to comply with both the MSR and TDSR limits. The differences of both ratios are summarised in the table below.

Table 1: Summary of the differences between TDSR and MSR

| TDSR | MSR | |

| Definition | Refers to the portion of a borrower’s gross monthly income that goes towards repaying the monthly debt obligations, including the loan being applied for | Refers to the portion of a borrower’s gross monthly income that goes towards repaying all property loans, including the loan being applied for |

| Properties that this loan applies to | All property types | HDB flats and ECs only |

| Threshold | 55% of borrower’s gross monthly income | 30% of borrower’s gross monthly income |

| Debt Obligations included | All debt obligations (e.g. Car loans, student loans) | Only property loans (Including the one being applied for) |

| How it is calculated | TDSR = (Total monthly debt)/(Gross monthly income) x 100% | MSR = (Total monthly mortgage repayment(s))/(Gross monthly income) x 100% |

It’s also worth bringing up (again) that both TDSR and MSR account for different financial considerations. TDSR factors in all of a borrower’s unsettled debt, including loans taken out for housing, cars, education, credit cards, and so forth.

In comparison, MSR is more straightforward as it’s solely calculated on a borrower’s monthly income. For borrowers buying an HDB or EC unit, their household monthly income will first be assessed using the MSR on their loan quantum to calculate the maximum amount they can repay monthly.

Thereafter, buyers will be further subject to a second round of assessment, which will consider all their debt repayments are within the TDSR limits. Should the borrowers have outstanding debts such as car loans, it may affect the amount they borrow and they may not get the maximum MSR loan amount.

How do you calculate MSR based on your household income?

In general, a borrower’s MSR can be derived by dividing their total monthly mortgage repayments by their gross monthly household income.

Assuming Party A has a gross monthly income of $10,000, his MSR calculations would be so…

$10,000 x 30% = $3,000

In another scenario, if Party A has an existing debt of $4,000 and a gross monthly income of $10,000, his MSR calculations would be so…

Maximum MSR loan amount = $10,000 x 30% = $3,000

Maximum TDSR loan amount = $10,000 x 55% = $5,500

Maximum MSR loan amount that can be taken to meet TDSR limit = $5,500 – $4,000 (Existing debt) = $1,500

In other words, even though Party A’s maximum mortgage affordability is $3,000 (based on the current MSR threshold of 30%), their existing debt of $4,000 limits their borrowing capacity to just $1,500.

To gauge the estimated loan quantum a household can secure based on MSR, one can refer to the sensitivity analysis table below. With a monthly household income of $16,000, a family can afford a home of up to $1.01mil, which works out to the price of a 2-room condo in the OCR.

Table 2: MSR Sensitivity Analysis- Based on Value Of Property on Household Income and Mortgage Rates for a 25 Year Loan

| Interest Rates | |||||

| Household Income | Monthly Payment | 3.00% | 3.50% | 4.00% | 4.50% |

| $10,000 | $3,000 | $633,000 | $600,000 | $569,000 | $540,000 |

| $11,000 | $3,300 | $696,000 | $660,000 | $626,000 | $594,000 |

| $12,000 | $3,600 | $760,000 | $720,000 | $683,000 | $648,000 |

| $13,000 | $3,900 | $823,000 | $780,000 | $739,000 | $702,000 |

| $14,000 | $4,200 | $886,000 | $839,000 | $796,000 | $756,000 |

| $15,000 | $4,500 | $949,000 | $899,000 | $853,000 | $810,000 |

| $16,000 | $4,800 | $1,013,000 | $959,000 | $910,000 | $864,000 |

| $17,000 | $5,100 | $1,076,000 | $1,019,000 | $967,000 | $918,000 |

| $18,000 | $5,400 | $1,139,000 | $1,079,000 | $1,024,000 | $972,000 |

| $19,000 | $5,700 | $1,202,000 | $1,139,000 | $1,080,000 | $1,026,000 |

| $20,000 | $6,000 | $1,266,000 | $1,199,000 | $1,137,000 | $1,080,000 |

Source: ERA Research and Market Intelligence (*Rounded to the nearest thousand)

How do you calculate TDSR?

Similar to MSR, it’s possible to derive a borrower’s TDSR with the help of a formula, which is as follows…

So, for instance, if Party B earns a fixed income of $10,000 a month and owes $2,000 in car loans as well as $1,000 in credit card loans, their maximum remaining capacity for monthly mortgage payments, based on the current TDSR threshold of 55%, would be…

Maximum loan based on TDSR limits = $10,000 X 55% = $5,500

Maximum remaining borrowing capacity = $5,500 – car loan ($2,000) – credit card loan ($1,000) = $2,500

However, if a borrower’s income varies from month to month, their TDSR can be slightly trickier to calculate. And that’s because they’re only permitted to use 70% of their gross monthly income for TSDR calculations. Or as MAS puts it: “financial institutions are required to apply a haircut of at least 30% to all variable income (e.g. bonuses) and rental income”.

Therefore, if we’ve Party C who has a similar debt situation as Party B, along with a gross monthly income of $10,000 – consisting of a fixed component of $7,000 and $3,000 in commissions – their TDSR calculations will look like this…

Maximum loan based on TDSR limits = [$7,000 + ($3,000 X 70%)] X 55% = $5,005

Maximum remaining borrowing capacity: $5,005 – car loan ($2,000) – credit card loan ($1,000) = $2,005

To gauge the estimated loan quantum a household can secure based on TDSR, we can refer to the sensitivity analysis table below. Under TDSR, a family earning a monthly household income of $16,000 can purchase a home of up to $2.4mil which is a rough cost for a sizable 3-bedroom OCR condo presently.

Table 3: TDSR Sensitivity Analysis– Max Value of property value based on household income and mortgage rates for a 25 Year Loan

| Interest Rates | |||||

| Household Income | Monthly Payment | 3.00% | 3.50% | 4.00% | 4.50% |

| $10,000 | $5,500 | $1,547,000 | $1,465,000 | $1,390,000 | $1,320,000 |

| $11,000 | $6,050 | $1,702,000 | $1,612,000 | $1,529,000 | $1,452,000 |

| $12,000 | $6,600 | $1,856,000 | $1,758,000 | $1,668,000 | $1,584,000 |

| $13,000 | $7,150 | $2,011,000 | $1,905,000 | $1,807,000 | $1,716,000 |

| $14,000 | $7,700 | $2,165,000 | $2,051,000 | $1,946,000 | $1,848,000 |

| $15,000 | $8,250 | $2,320,000 | $2,198,000 | $2,084,000 | $1,980,000 |

| $16,000 | $8,800 | $2,475,000 | $2,344,000 | $2,223,000 | $2,111,000 |

| $17,000 | $9,350 | $2,629,000 | $2,491,000 | $2,362,000 | $2,243,000 |

| $18,000 | $9,900 | $2,784,000 | $2,637,000 | $2,501,000 | $2,375,000 |

| $19,000 | $10,450 | $2,939,000 | $2,784,000 | $2,640,000 | $2,507,000 |

| $20,000 | $11,000 | $3,093,000 | $2,930,000 | $2,779,000 | $2,639,000 |

Source: ERA Research and Market Intelligence (*Rounded to the nearest thousand)

Scenarios where the TDSR Ratio is not applied

Although it’s safe to say that TDSR and MSR will almost certainly be applied to the majority of home loan calculations, there are certain scenarios where borrowers can be exempted from TDSR rules too. For example, TDSR is currently waived for owner-occupiers when they refinance their housing loans. Likewise, bridging loans where the outstanding balance will be repaid within 6 months are also exempted from TDSR rules.

Kassia, a condominium at Loyang/Changi

The same applies to mortgage equity withdrawal loans too, provided the Loan-to-Value ratio, combined with any other loans secured against the same property, does not exceed 50%. Lastly, another important term to know is the Loan-to-Value ratio.

Loan-to-Value Ratio

The LTV ratio is the percentage of the property value an individual is allowed to borrow to finance their home mortgage. Implemented by the government, this ratio serves to limit how much money can be borrowed by individuals to ensure the borrower is able to repay all their loans and not over-leverage.

The LTV limit for an individual with no existing housing loans is capped at either 75% or 55%, with a minimum cash down payment of 5% or 10% respectively. The table below will delineate the differences in LTV limits based on the number of outstanding housing loans.

Table 4: LTV Limits Applied based on Outstanding housing loans

| Number of Outstanding Housing Loans | LTV Limit | Minimum Cash Down Payment |

| 0 | 75% or 55% | 5% (for 75% LTV) or 10% (for 55% LTV) |

| 1 | 45% or 25% | 25% |

| 2 or more | 35% or 15% | 25% |

Source: MAS, ERA Research and Market Intelligence

The lower LTV limit should be applied if the loan tenure exceeds 30 years, or 25 years for HDB flats, or if the loan period extends beyond the borrower’s age of 65 years. For HDBs, the maximum loan an individual can take to finance their flat has been tightened.

With effect from 20 August 2024, the Loan-to-Value (LTV) limit for HDB loans will be lowered from 80% to 75%, akin to mortgage loans granted by financial institutions. The revised HDB LTV limit will apply to complete resale applications received by HDB on or after 20 August 2024.

A complete resale application is one where HDB has received both the sellers’ and buyers’ portions of the application. For applicants who were successful in the June BTO exercise, the LTV limit for their housing loans will not be affected and will remain at 80%.

Keen to learn more about how this applies to your homebuying journey? Or about TDSR and MSR in general? Feel free to speak to an ERA Trusted Adviser today!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Have you ever dreamed of staying in a place not dominated by towering high-rises but filled with greenery and low-rise houses instead? A place with its own unique flair and personality, where heritage and modern lifestyle blend seamlessly? Areas like Katong or Tiong Bahru might come to mind, but they can be a bit too upscale for some. What if we told you there’s a hidden gem in District 19 that offers the same charming living experience?

Welcome to the quaint estate of Serangoon Garden, one of Singapore’s most distinct housing areas.

A Brief History

Serangoon Garden is a residential estate and a subzone in the Serangoon planning area, located in District 19.

In the 1950’s the estate now known as Serangoon Gardens was built to provide housing for workers and their families in the area, such as teachers, labourers and airmen. These townhouses and bungalows, with their distinctive red roof tiling became synonymous with the area – a distinctive trait that a good number of houses retain, even today.

As the area became populated, amenities and conveniences were built into the area, such as shops, eateries started showing up, and a recreational clubhouse, Serangoon Gardens Sports Club.

Serangoon Garden Today: Amenities and Landscape

Serangoon Garden has kept most of its landscape and architecture from the olden days, retaining its iconic look and feel, while offering modern conveniences to its residents.

Serangoon Garden Circus, where most of the shops were situated still stands, with their tenants hosting a wide range of food and services catered to the modern tastes of residents.

The recreational clubhouse, now known as Serangoon Gardens Country Club, still stands, with members from the estate frequenting it for sports and recreational activities, as well as classes and enrichment activities for their children.

The street food vendors that used to run their businesses out of carts along Serangoon Garden Way were also given a hawker centre to set up stalls and operate out of in 1972.

The hawker centre, now known as Chomp Chomp Food Centre, is famous today for its selection of local food (famous dishes there include BBQ stingray and Hokkien Mee) and is one of the more well-known and frequented hawker centres in Singapore.

Why Is Serangoon Gardens Such a Popular Estate?

Serangoon Gardens is one of the most popular and recognisable estates in Singapore, and for good reasons.

Kampong Spirit

It is not uncommon to find people that have stayed there their whole lives, with their homes being passed down generations over the last 70 or so years of its existence. This gives the estate a warm, kampong feel with the community fostered between the residents of the estate that residents have fondly dubbed “the feel of an old English village”.

A cosmopolitan village

In addition to this expatriates, particularly those from Australia or France, tend to rent homes in Serangoon Gardens, due to its proximity to the Australian and French international schools.

With an established community of foreigners and expatriates, there has been an increase in the number of businesses catered to the needs of these communities. You can find cafes and eateries at Serangoon Garden Circus serving western fare, as well as grocery stores such as Little Farms and a French grocer.

The presence of these establishments within the landed enclave gives the neighbourhood a distinct, cosmopolitan vibe that can be likened to that of Holland Village.

A Wealth of Amenities

In comparison to other landed estates or enclaves in Singapore, Serangoon Garden offers more amenities to its residents. The mini hub at Serangoon Garden Circus offers everything for its residents, from food, to enrichment and tuition centres, as well as healthcare, and pet care shops.

There is even a shopping mall, MyVillage with a FairPrice Finest for residents to do their shopping, along with dining options, and beauty parlours and hair salons.

Scarcity of Housing in Serangoon Gardens

Given the popularity of the estate, housing availability is scarce in Serangoon Gardens. This is especially so when we consider that most of the houses in the estate are landed homes.

Currently, landed homes are high in demand, with a low supply. As a result, landed homeowners possess strong holding power, with the median price for a house in Serangoon Gardens in 2024 costing $4.62m, making it inaccessible for most homebuyers.

With landed houses being scarce, costly, and mostly out of reach for most of us, we automatically look for non-landed private property options in the area. However, a search in the Serangoon Gardens estate would show that there are few condominium or private apartments.

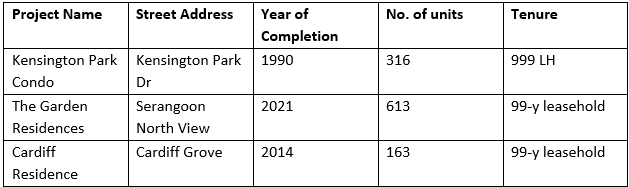

Table 1: Non-landed private projects in Serangoon Garden Estate (<500m of Serangoon Garden Circus)

Source: PropertyGuru, ERA Research and Market Intelligence

For those looking for a private property close to Serangoon Gardens, a fantastic place to look would be its sister neighbourhood of Lorong Chuan.

Lorong Chuan – An Alternative

Lorong Chuan is a subzone and precinct that neighbours the Serangoon Gardens estate. The precinct is named after a road bearing the same name, which connects the Central Expressway (CTE) to Serangoon Gardens.

It is considered a desirable location to live in by Singaporeans and foreigners alike, for three notable reasons. Firstly, it is close to Serangoon Gardens and Serangoon Central, as well as Bishan and Toa Payoh towns, offering residents of the precinct a wealth of amenities and conveniences.

Secondly, the precinct is also serviced by Lorong Chuan MRT, one stop away from Serangoon and Bishan MRT stations – major interchanges on the North-South and North-East lines respectively.

Finally, there are a variety of condominium projects here that are allow living near the landed estates of Serangoon Gardens and Braddell Heights at a more affordable price point.

Price Growth

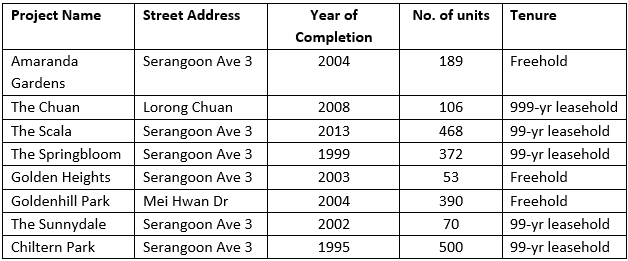

Table 2: Non-landed private projects in Lorong Chuan

Source: PropertyGuru, ERA Research and Market Intelligence

Demand drivers for homes in the area directly stem from the convenience that the area provides. In addition to this, the neighbourhood falls within the 1km radius for notable schools such as St. Gabriel’s Primary School and CHIJ Our Lady of Good Counsel.

While there is a thriving and attractive private condominium estate in Lorong Chuan, there hasn’t been a new launch in the area in over a decade – that is until the announcement of the upcoming Chuan Park, which has caught the attention of the market as one of the biggest launches of 2024.

Chuan Park – A New Development with New Opportunities

Chuan Park is an upcoming 916-unit mega development with a 99-year leasehold tenure. It is being built as a redevelopment following the collective sale exercise of the former Chuan Park condominium.

Adding a stock of 916 units to the existing inventory of 2,148 units in Lorong Chuan will increase the number of condominium units in the area by 43%, which is sure to rejuvenate and encourage price growth.

Mega-Development, Mega Benefits!

Being a mega-development, Chuan Park will have clear strengths in the market for investors, such as a fresh 99-year lease, along with a wide variety of amenities that will attract buyers and tenants from diverse groups.

In addition to this, families will be drawn to the development, due to its wide array of facilities, distance to nearby amenities and a 1km priority enrolment distance to St. Gabriel’s Primary and CHIJ Our Lady of Good Counsel.

Great Accessibility

The most attractive attribute about the location is that Lorong Chuan MRT is situated right at its doorstep. Aside from integrated developments, not many condos in Singapore can boast this level of convenience.

Lorong Chuan MRT on the Circle Line provides a direct route to Marina Bay, as well as to Buona Vista and one-north business nodes. It is also within 3-5 stops to the Thomson East Coast Line, East West Line and Downtown Line, as well as 6 stops to Orchard, further connecting it to more business nodes in Singapore.

Working professionals could also find the location attractive if they work at New Tech Park. Alternatively, Lorong Chuan’s location adjacent to the CTE provides a speedy 15-minute drive to the central region of Singapore.

Expected to launch in the second half of this year, Chuan Park is bound to turn heads as one of the biggest launches of the year. If you are interested to find out more about this exciting new launch, kindly reach out to an ERA trusted advisor today.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any

URA dropped ten sites on the Confirmed List. Could this lead to a potential housing glut?

On the 25th June 2024, the Urban Redevelopment Authority (URA) announced a list of ten sites on the Confirmed List for their Government Land Sales (GLS) program. These will comprise nine residential sites, inclusive of an executive condominium (EC) plot, and a residential and commercial plot.

This is part of an active effort by the government to stabilise property prices and manage long-term housing demand. We are positive that this will give homebuyers more choices in the future, especially with sites in sought-after locations like Bayshore Road and Chuan Grove.

Overall, these ten sites could yield an estimated 5,050 residential units – a similar figure to the 5,450 units offered in 1H 2024’s Confirmed List of GLS sites.

A total supply of 11,110 private residential units in 2024 (including 610 units from the activated Reserve List site tendered out in May 2024) will be the highest supply introduced in a single year since 2013.

The sites available under the Confirmed List are as follows.

Table 1: Confirmed List 2H 2024

| Site | Type of Site |

Area (ha) |

Proposed GPR |

Estimated No. of Residential Units |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (sqm) |

Estimated Launch Date |

Agency |

| Tampines Street 95 (EC) | Residential |

2.25 |

2.5 |

560 |

0 |

– |

Aug-2024 |

HDB |

| Faber Walk | Residential |

2.58 |

1.4 |

400 |

0 |

– |

Sep-2024 |

URA |

| Lentor Gardens | Residential |

2.06 |

2.1 |

500 |

0 |

– |

Oct-2024 |

URA |

| River Valley Green (Parcel B) | Residential |

1.17 |

3.5 |

580 |

0 |

500 |

Oct-2024 |

URA |

| Bayshore Road | Residential |

1.05 |

4.2 |

515 |

0 |

– |

Nov-2024 |

URA |

| Media Circle (Parcel A) | Residential |

0.81 |

3.7 |

345 |

0 |

400 |

Nov-2024 |

URA |

| Media Circle (Parcel B) | Residential |

0.97 |

4.3 |

485 |

0 |

400 |

Nov-2024 |

URA |

| Chuan Grove | Residential |

1.58 |

3.0 |

550 |

0 |

– |

Dec-2024 |

URA |

| Holland Link | Residential |

1.72 |

1.4 |

240 |

0 |

– |

Dec-2024 |

URA |

| Chencharu Close | Commercial & Residential |

2.94 |

3.2 |

875 |

0 |

13,000 |

Sep-2024 |

HDB |

Source: URA, ERA Research and Market Intelligence

Among the sites, the Tampines Street 95 EC site and Chuan Grove are located within established residential enclaves that have previously seen resilient housing demand. This could draw higher interest from developers.

In addition to this, the URA has also placed an additional nine sites on their Reserve List as part of the 2H 2024 GLS program, should developers feel the need to bid for extra sites based on market demand. The Reserve List comprise five residential sites, one commercial site, two white sites, and a hotel site.

In total, they offer a potential 3,090 residential units, as well as 99,350 sqm gross floor area of commercial space, and 530 hotel rooms.

Table 2: Reserve List 2H 2024

| Site | Type of Site |

Area (ha) |

Proposed GPR |

Estimated No. of Residential Units |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (sqm) |

Estimated Launch Date |

Agency |

| Senja Close (EC) | Residential |

1.01 |

3.0 |

295 |

0 |

0 |

Available |

HDB |

| Marina Gardens Lane | Residential |

0.61 |

5.6 |

400 |

0 |

0 |

Oct-2024 |

URA |

| Woodlands Drive 17 (EC) | Residential |

2.58 |

1.7 |

435 |

0 |

0 |

Oct-2024 |

HDB |

| Holland Plain | Residential |

1.58 |

1.8 |

275 |

0 |

0 |

Dec-2024 |

URA |

| River Valley Green (Parcel C) | Residential |

1.15 |

3.5 |

470 |

0 |

0 |

Dec-2024 |

URA |

| Punggol Walk | Commercial |

1.00 |

1.4 |

0 |

13350 |

0 |

Available |

URA |

| Marina Gardens Crescent | White |

1.73 |

4.2 |

775 |

6000 |

0 |

Available |

URA |

| Woodlands Avenue 2 | White |

2.75 |

4.2 |

440 |

78000 |

0 |

Available |

URA |

| River Valley Road | Hotel |

1.02 |

2.8 |

0 |

2000 |

530 |

Available |

URA |

Source: URA, ERA Research and Market Intelligence

A total of 17 new projects are set to launch in 2H 2024, tallying to an estimated 8,300 new homes.

There are eight more sites currently open for tender, and another one set to launch this month. This bumper crop of GLS sites in 2H 2024 will further bolster the existing ample land supply.

However, prevailing factors like the high-interest rate environment, economic uncertainty, and slower new home sales amidst tighter homebuyer affordability may encourage developers to bid prudently.

Let’s go over the location analysis for the ten GLS sites on the confirmed list.

Tampines Street 95 (EC) – 560 units

Source: URA

In contrast to the plot at Tampines Street 94 (previously launched in 1H 2024), the newly released site at Tampines Street 95 is earmarked for development as an EC project.

Being near its sister plot, this puts the site at Tampines Street 95 within range of Tampines West MRT station, Bedok Reservoir Park, as well as future retail options at Tampines Street 94. This confluence of amenities, coupled with its designation as an EC site, will likely make Tampines Street 95 an attractive proposition for developers and future buyers alike.

Faber Walk – 400 units

Source: URA

This site is between AYE, Pandan River and the Faber Walk landed enclave. It will be a low-rise development of up to five storeys, comprising of 400 units. While there are no MRT stations in the vicinity, is it only a 5-minute drive to Clementi MRT Station. Despite being next to AYE, residents will enjoy privacy in this tranquil living environment along Pandan River. The adjacent site (now Waterfront@Faber) was previously awarded for $687 psf ppr in June 2013. We may see muted response due to the location of the site.

Lentor Gardens – 500 units

Source: URA

Even though the Lentor Gardens GLS site is the last site available in the Lentor Hills estate, much of the area’s housing demand has been absorbed by earlier launches. Furthermore, it is the furthest site from Lentor MRT station making it less advantageous compared to neighbouring plots. Thirdly, the upcoming Upper Thomson site awarded to GuocoLand and Hong Leong will also provide prospective homebuyers with more options.

River Valley Green (Parcel B) – 580 units

Source: URA

The launch of the River Valley Green (Parcel B) site comes hot off the heels of the closure of Parcel A’s tender last week. The site, which is an estimated yield of 580 units, borders Great World MRT and is also near Great World City and River Valley Primary School. However, despite its remarkable locational attributes, it remains to be seen whether developers will exhibit interest for Parcel B, given the saturation of new launches in the area for the next two years.

Bayshore Road – 515 units

Source: URA

The Bayshore Road site is the first to be launched in the area since 1997. With a potential yield of 580 residential units, it will join upcoming HDB projects in shoring up Bayshore’s nascent future as a new waterfront neighbourhood. The site’s proximity to the newly operational Bayshore MRT station and the expansive views of East Coast Park from future high-rise units are also compelling selling points. We expect to developers to put in competitive bids for the site, especially with Bayshore’s promising future and the scarcity of newer private residential developments in the area.

Media Circle (Parcel A) and (Parcel B) – 345 and 485 units

Source: URA

Source: URA

Straddling each side of Portsdown Road, both the Media Circle (Parcel A) and Media Circle (Parcel B) sites are poised to bolster the future housing supply in one-north with a total of 830 estimated residential units; this is in line with URA’s plans to enhance the area as a vibrant mixed-use district. This could also make shorter office-to-home commutes a reality for residents working in the vicinity.

Additionally, unlike the Media Circle plot launched in 1H 2024, both new sites are not required to include a Serviced Apartments II (SA2) component. Without the mandatory requirement to include long-stay serviced apartments, developers will likely be more motivated to bid for these parcels in the face of diminished risk.

Chuan Grove – 550 units

Source: URA

This site can potentially yield 550 homes in high-rise tower blocks. It will likely draw competitive bids being on the edge of the city fringe with amenities and schools while being a 3-minute walk to Lorong Chuan MRT Station. The existing Chuan Park site that was sold enbloc is scheduled to launch in 2H 2024.

Holland Link – 240 units

Source: URA

The GLS site at Holland Plain consists of an estimated 240 units and is located amidst a predominantly landed housing enclave. Considering its exclusive location, the site is likely to be developed as high-end luxury homes to support housing needs for the residents in the vicinity.

Chencharu Close – 875 units

Source: URA

Chencharu’s status as Yishun’s newest residential precinct will translate into new convenience-driven amenities for residents, both existing and new. Close to 2,000 private residential units are slated for development in Chencharu; this figure is inclusive of its first-ever mixed-use site where 875 private homes could be potentially built, accompanied by a bus interchange and hawker centre.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Heard of developments like Ardor Residence, The Hillshore, or Straits at Joo Chiat? Then you might already be familiar with some of the newest boutique condominiums, or boutique condos on the market now.

Consisting of 100 units or less, boutique condominiums (or condos) are small, yet sophisticated. And though they possess smaller site areas and fewer amenities than their larger counterparts, boutique condos deserve to be on your radar – even if you are home-hunting in a bigger development.

Due to their unique selling points, boutique condos represent a distinct, but nonetheless, compelling value proposition for buyers.

In this article, we breakdown the benefits, and also, potential drawbacks of boutique condos so you can easily determine whether these small, but mighty developments are the right choice!

Boutique condos are private and exclusive

Unlike larger developments, boutique condos typically appeal to an entirely different crowd from families. Buyers who value exclusivity and serenity are likely to be drawn to boutique condos; this includes couples with no children or empty nesters – parents whose children have grown up and moved out.

Empty nesters will likely find boutique developments more appealing as they may no longer have a need for the wider range of facilities that large condos have. Instead, boutique condos – with their smaller, but curated selection of amenities – can provide them with a more personalised living experience.

Coupled with a smaller resident community, boutique condos are a more intimate choice of residence for the aforementioned buyer groups. One striking example of this can be found in District 15, where both Grand Dunman (a 1,008-unit mega-development) and Straits of Joo Chiat (a 16-unit boutique development) are located.

Boutique condos offer greater flexibility in their layouts

Exclusivity aside, another benefit of choosing boutique condos is the added flexibility they offer in their layouts.

As boutique condos are often built on land acquired through collective (or en-bloc) sales of older condos, they are not subject to the requirement imposed residential developments built on Government Land Sales (GLS) sites to be constructed with a 65% Prefabricated Prefinished Volumetric Construction (PPVC) method.

Tower crane hoisting of ppvc module. Image credit: BCA

This method of construction entails creating free-standing 3D modules with internal finishes, fixtures and fittings on an off-site fabrication facility before being delivered and installed on-site.

This requirement, mandated by the Building and Construction Authority is to ensure that condos built on GLS sites have faster construction times and better quality control. The downside of the PPVC method, however, is that there is less flexibility in being able to knock down or merge rooms, unless there are flexi rooms included in the unit configuration and layout.

Developers of boutique condos might not opt to utilise the PPVC method in building construction – as they are not mandated to do so. With their smaller size, it might be faster or more affordable to construct boutique developments the traditional way.

Homeowners of boutique condos have more flexibility when designing their interior, allowing them to use quirky or open-concept designs.

Boutique condos being constructed traditionally offer homebuyers the flexibility to knock down or merge rooms much more freely than in a condo constructed with the PPVC method, which are more restrictive with their renovation guidelines. This enhanced layer of flexibility appeals to homebuyers that are looking for a condo for their own stay.

New Launch Freehold boutique condos are value for money

Ever since the government has stopped putting freehold land for sale as part of the GLS program, new freehold projects have become a rare commodity.

Of 132 freehold condos launched in the last decade, 101 (or 77%) of them were boutique condos.

The reason why there is such a large number of freehold boutique condo is that they are often built on en-bloc sites. These smaller plots of land are easier and cheaper for smaller developers to buy and develop, presenting less of a risk compared to developing a larger project.

Freehold property offers perpetual ownership, which is a rare commodity in land-scarce Singapore. It offers a secure way to hold and pass down wealth to future generations.

A freehold boutique condo makes for a fantastic legacy asset. Image: The Hillshore

As they are not subject to lease decay, freehold properties perpetually hold their value. It is unlikely that they net a loss when they eventually get transacted many years, or even decades down the road.

Given a quiet en-bloc market and a scarcity of new freehold condos, boutique condos offer buyers in the market for a new freehold condo with invaluable options.

The culmination of the aforementioned factors makes boutique freehold condos a treasured legacy asset to be passed on to future generations. They make great homes for older parents to invest in – as their children leave the nest to start their own families. For them, owning a boutique freehold condo is a great way to preserve their wealth and ensure a more secure future for their loved ones

Some boutique condos might have a lower entry price

Boutique condos are built on smaller plots of land, which are often purchased as part of an en-bloc sale by developers. Due to their small size, developers are able to purchase and redevelop the land more affordably. This results in lower launch prices, compared to larger projects built on GLS sites.

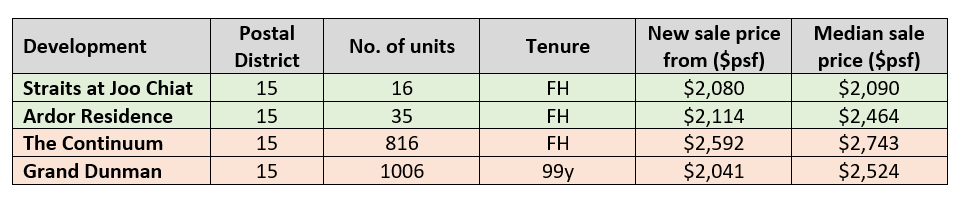

Table 1: Comparison between boutique (green) and large-sized (red) condos in District 15

Source: URA as of 19th June 2024, ERAPro

By comparing two new boutique condos with two larger projects within District 15, we can see that boutique condos generally have a lower entry price.

Additionally, boutique condos are often located in private and exclusive locations, such as within landed enclaves. These locations are less convenient compared to the locations of larger condos, which are more prominent and located closer to transport nodes, amenities and schools.

While these factors all contribute to a lower entry price for boutique condos, that doesn’t necessarily equate to a low exit price.

Comparing the price growth of boutique with medium-large sized condos island-wide, we can see that larger condos see an overall more robust price growth.

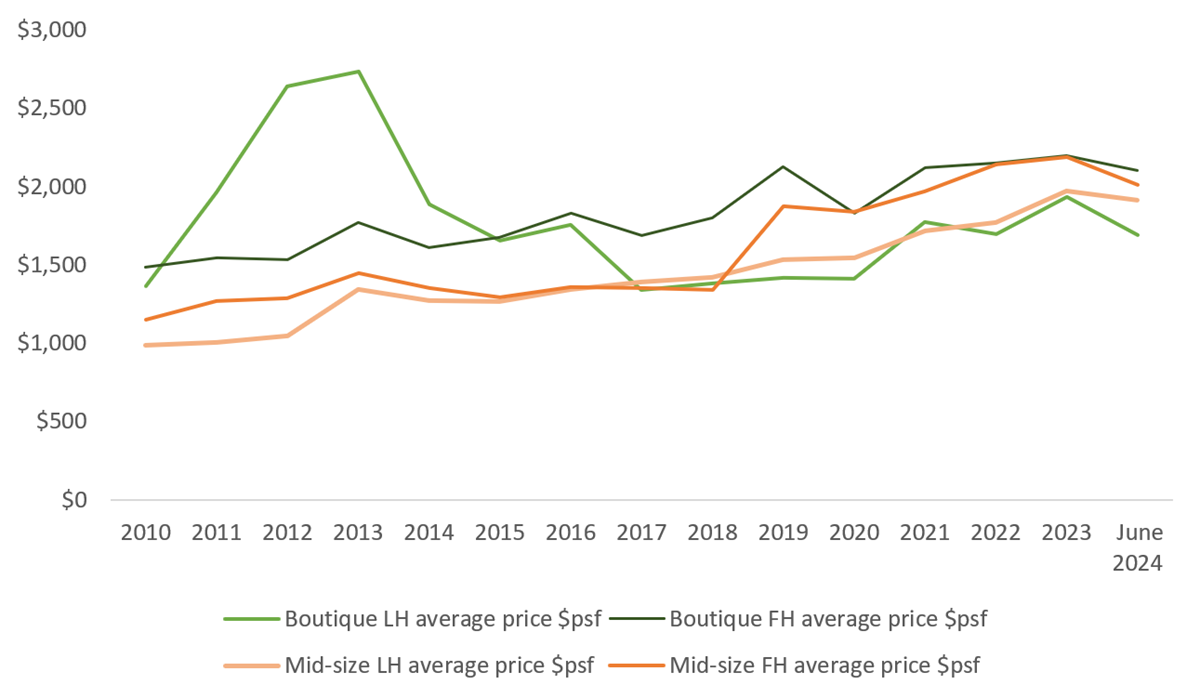

Chart 1: Average transacted price $psf of leasehold (LH) and freehold (FH) boutique and mid-sized condos

Source: URA as of 12th June 2024, ERA Research and Market Intelligence

Boutique leasehold condo prices grew by 24.1% since 2010, compared to mid-sized leasehold condos which saw 93.6% growth.

Less of a disparity was seen in the freehold market, with boutique condo prices growing by 41.5% compared to mid-sized condos, which saw 74.6% growth.

It is expected for the larger developments to experience a faster price growth. Larger projects, especially mega-developments possess the “sales” volume required to drive transaction prices. As a result, they generally see a faster price growth due to frequent transaction activity.

However, this does not mean that boutique condos are poor investment choices. Owners of boutique condos are still able to make a profit when they do decide to sell, albeit at a lower rate.

Final Considerations

To sum it all up, yes – boutique condos might not be for everyone.

Owners of boutique condos often tell stories of how long it takes for them to sell their unit, further exaggerated the smaller the development is.

If you are looking for an investment property with high liquidity and a faster rate of capital appreciation, a larger condo with features that appeal to mass market buyers would be preferred.

Similarly, families with young children will lean towards larger condos due to their accessibility, wide variety of facilities, and livelier atmosphere for their children to grow up in.

However, if these concerns are not of priority, you might find the prospect of living in a boutique condo alluring. They offer a level of privacy and exclusivity that is only bested by landed property, which lies within an entirely different price bracket.

Additionally, living in a boutique condo allows residents to foster a strong sense of community. With a fewer number of occupants, residents are able to build closer and more meaningful relationships with their neighbours.

Buyers who want to own a freehold project have limited choices in today’s market, and may opt to turn to boutique condos. On the whole, they hold their value well, and more importantly offer this same value for generations to come.

Table 3: New launch boutique condos available (as of 18th June 2024).

Source: ERAPro as of 18 June 2024, ERA Research and Market Intelligence

If you are interested in, and would like to find out more about these exciting new boutique projects, do not hesitate to approach an ERA trusted adviser today.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

In recent months, land bids for Government Land Sales (GLS) sites have fallen, with noticeably lower participation by developers. In the first five months of 2024, the average number of developers bidding for awarded sites with residential use fell to 2.4, down from 3.4 in 2H 2023 and the peak of 8.6 in 2021.

Chart 1: Average number of bidders for GLS sites*

Source: URA, ERA Research and Market Intelligence, *Sites zoned ‘Residential (Non-landed)’, ‘Residential and Commercial’, ‘Residential with Commercial on 1st storey’ and ‘White’

Land bids in recent months have been comparatively lower than those for previously sold sites that share similar locational attributes. The media has reported that some sites sold were sold at prices “below analyst’s predictions”. Moreover, the Marina Gardens Crescent site was not awarded as the $984 per square feet per plot ratio (psf ppr) was “too low”.

Below are some examples of recent GLS residential sites that sold for up to 32.0% less than some neighbouring developments.

Table 1: Recent GLS sites awarded previously and recently in similar locations

Source: URA, ERA Research and Market Intelligence 1. The site is zoned Residential with Commercial at 1st Sty. 2. Sites are in different districts, but are just 150m apart.

Could this change signal waning demand for GLS sites? Are developers exercising more caution? Will new launch prices finally fall?

Below, we explore the answers to these questions through the lens of 4 recent GLS sites, alongside the reasons why developers are unlikely to cut new launch prices.

Reason #1: The floor area harmonisation rule reduces sellable floor area in a development

Applying to all residential and industrial GLS sites launched for sale from 1 September 2022 onwards, the new Floor Area Harmonisation rule will see the following changes implemented:

- The Urban Redevelopment Authority, Singapore Land Authority, Building and Construction Authority and Singapore Civil Defence Force will measure all floor areas to the middle of the wall

- All strata areas will be included in Gross Floor Area (GFA).

- All voids will be excluded from the strata area.

As a result of these changes, spaces like air-con ledges and voids are no longer included as sellable spaces. But developers are unlikely to lower selling prices, even if they pay less for land. To put things into perspective, developers do incur expenses building void spaces and aircon ledges and hence they are likely to incorporate related costs into the selling price.

Table 2: Land prices for projects launched before and after the floor area harmonisation rule

Source: URA, ERA Research and Market Intelligence* Site is zoned Residential with Commercial at 1st Sty.

A case in point is Lentor Mansion, where units launched after the floor area harmonisation rule are priced higher per square foot than units of similar size and design at Lentor Modern. This is despite Lentor Mansion’s lower land cost of $985 psf ppr, compared to Mentor Modern’s $1,204 psf ppr (18.2% difference).

Table 3: Price difference for 2-bedroom units at Lentor Modern and Lentor Mansion

Source: URA, ERA Research and Market Intelligence

Reason #2: Developers expected to undertake higher risks for some sites

Higher Additional Buyer Stamp Duty (ABSD)

Since the Cuscaden Road site was awarded in May 2018, there has been three rounds of ABSD hikes on foreign buyers, raising the original rate to a hefty 60%. With developments in the Core Central Region (CCR) typically seeing more foreign buyers, developers are becoming more conscious about waning demand. Hence, they are lowering their bids to account for the current market conditions.

Image 1: Timeline of increases in ABSD for foreign buyers (non-Singapore permanent resident)

Source: IRAS, ERA Research and Market Intelligence

As demand from foreign buyers was high before July 2018, the developer of Cuscaden Reserve was more bullish in their bids.

However, with the market now cooled, developer sentiments are substantially dampened, resulting in the top bid for the Orchard Boulevard site being 32% lower than Cuscaden Reserve’s.

Depending on market conditions, further revisions to the ABSD rate could happen.

Consequently, developers must factor in such regulatory risks that could affect sales of units; this might involve setting aside funds for marketing or contingency costs.

Business risks arising from a new rental housing typology

Driven by evolving demographics and rising demand for rentals amongst Singaporeans, the URA recently introduced a new class of long-stay serviced apartments (SA2) in several of their newly released GLS sites.

With a minimum stay of three months, SA2s are intended to cater to tenants in need of housing for a period lasting longer than a typical hotel stay, but shorter than the usual 1-year lease for local rentals. Potential tenants for SA2 apartments may include foreigners on extended job stints, some younger Singaporeans who may choose to rent as a start, and homeowners waiting out their home completion or renovation.

Developers undertaking SA2 projects are required to either have hospitality expertise or to partner with parties with relevant capabilities. Furthermore, being an untested market, it may be challenging for developers to determine the demand for properties built under this new rental housing typology.

Zion Road, Parcel A (Source: Google Maps)

The Zion Road (Parcel A) site is the first site to pilot the new SA2 flats. It was sold for $1 billion ($1,202 psf ppr), 30.6% lower than the site sold at Jiak Kim Street (now Rivière), which sold for $955.4 million or $1,733 psf ppr in 2018.

Nevertheless, even with the comparatively lower land cost, developers for Zion Road (Parcel A) are not expected to reduce selling prices. On the contrary, they could even factor in holding costs and possible vacancies of the SA2 units, given uncertainty about their future profitability.

Larger projects may present higher risk of unsold units

Treasure at Tampines (Source: Sim Lian)

Although large residential projects offer enticing benefits like larger total revenues and potentially lower construction costs due to economies of scale, they can also be fraught with risks for developers who choose to tender for larger GLS sites. The Zion Road (Parcel A) site has a maximum GFA of 85,577 sqm, potentially yielding 735 units (excluding SA2 units). Meanwhile, the 455-unit Riviere’s GFA is only 51,231 sqm, 40.1% less.

This heightened risk traces back to Singapore’s policy of imposing ABSD on unsold units. Under this regulation, developers who fail to sell all units within five years of acquiring a GLS site face a hefty penalty of up to 35% of the land cost.

This need to manage risk associated with unsold stock makes developers unwilling to lower selling prices, even with lower land costs. Instead, they are more likely to maintain prices in exchange for managing common challenges associated with large projects. These challenges include longer construction runways and more rigorous project requirements.

Reason #3: Surge in construction demand could drive construction and labour costs higher

At present, Singapore’s construction industry is experiencing strong demand for public and private projects. The total projected contract value is between $32 billion and $34 billion in 2024, the highest since 2015.

Chart 2: Construction demand in Singapore

Source: data.gov.sg, ERA Research and Market Intelligence

Key contributors to construction demand include private sector projects from GLS site tenders and the expansion of Singapore’s two integrated resorts. Similarly, public projects like HDB Build-to-Order (BTO) flats, the Cross-Island MRT line, Changi Airport Terminal 5, and Tuas Port have also significantly contributed to this growth in demand.

This momentum is expected to continue with the Building and Construction Authority forecasting a steady rise in demand to reach between $31 billion and $38 billion per year from 2025 to 2028. This translates into an increase of between 4.7% to 28.4% on the 10-year average of $29.6 billion.

With the increased volume of construction, competition for labour and materials has intensified. The Tender Price Index, which tracks the price movement of construction components such as materials and manpower, has grown by 32.4% between 2020 and 2023.

Although labour pressure has eased with approximately 40% more work permits issued for the construction, marine shipyard, and process industries, skilled labour shortages could remain a significant constraint.

Other cost pressures, such as higher-for-longer interest rates, persistent inflation, higher Goods & Services Tax, and heftier property taxes due to higher land values, also make price cuts from developers unlikely.

Additional Costs for Sustainability Considerations

In line with the cost-push factors highlighted above, developers could also incur extra expenditure due to certain requirements for the awarded GLS sites. These requirements incur additional consultancy and surveying fees for special impact assessment studies which adds to the developers’ costs. Examples of recent GLS sites necessitating special impact assessments are Upper Thomson (Parcel B).

Image: Upper Seletar Reservoir

Due to Upper Thomson (Parcel B)’s proximity to the Central Catchment Nature Reserve, developers must incorporate biodiversity-sensitive strategies as part of their proposed developments. This is to ensure Springleaf’s rich biodiversity is protected, as well as to strengthen ecological connectivity along the Khatib Nature Corridor.

Additionally, the site houses a conserved building, the former Seletar Institute, and an open communal space that must be restored and integrated into the resulting residential development.

So, what could cause new home prices to fall?

In the event that new home prices decline, we posit two reasons that could result in such an outcome.

A major economic shock leading to a decline in household income

Major economic shocks, leading to job losses and declining household income, may trigger price corrections in Singapore’s property market. This is evident from past cycles where the property market saw adjustments during the three major financial crises since the 1980s. Since then, the Government has implemented multiple rounds of cooling measures, as well as tightened borrowing conditions to encourage financial prudence.

Chart 3: GDP growth versus Property Price Index

Source: Singstat, ERA Research and Market Intelligence

Singapore starts experiencing a decrease in population

Like many developed countries, Singapore is experiencing an aging population with more than half of Singapore’s residents aged 65 years or older. Currently, the country’s working population is bolstered by non-residents who play a vital role in sustaining an aging workforce. Unless the government tightens its foreign labour policy, Singapore is unlikely to see a substantial population decline in the medium term, a factor that could influence housing demand, and by extension, new home prices.

Chart 4: Total Population versus Proportion of Singapore Residents (65 years and older)

Source: Singstat, ERA Research and Market Intelligence

Conclusion: Lower land costs may not necessarily translate into lower selling prices for upcoming new launches in the foreseeable future

While lower prices for GLS sites in the past year may appear to point towards lower new launch prices on the horizon, this is unlikely to be the case in the current market, as well as for the foreseeable future.

Although comparatively lower GLS site prices were observed in the past year, as seen through the examples above, this trend is unlikely to persist in the current market or the near future.

At present, lower land bids by developers can be attributed mostly to growing project costs and risk premiums. This is especially so for larger projects and those incorporating new home typologies or criteria.

Due to these factors, developers are more cautious about their land bids, and more selective about the sites they are bidding on. However, developers are expected to keep prices for new launches steady – as they undertaking greater risks while balancing buyer’s affordability.

Furthermore, with more GLS sites being awarded since 2021, many developers now possess ample land stock and are focusing on selling their existing new home supply. Unless the upcoming GLS sites possess attractive qualities (e.g. proximity to amenities or good schools nearby), they will be unlikely to attract a large number of bids by developers, much less aggressive ones. This raises the likelihood of GLS land prices staying stable for the foreseeable future.

This stability in land prices, suggests that private home prices are likely to remain steady; this aligns with URA’s goal of meeting homebuyer demand and achieving market stability, thus ensuring a healthy, well-balanced property market going forward.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

District 15 possesses a unique blend of heritage, convenience and quietness. It has always been lauded by Easties as one of the best places to live in Singapore.

Being a location well loved by both locals and expats alike, District 15 has always been a popular district among homebuyers. This is due to the allure and unique lifestyle offered by the seafront living experience.

If you have always dreamed of living along the East Coast, here’s your chance! There are several District 15 New Launch condos available on the market right now – which could end up becoming your dream home.

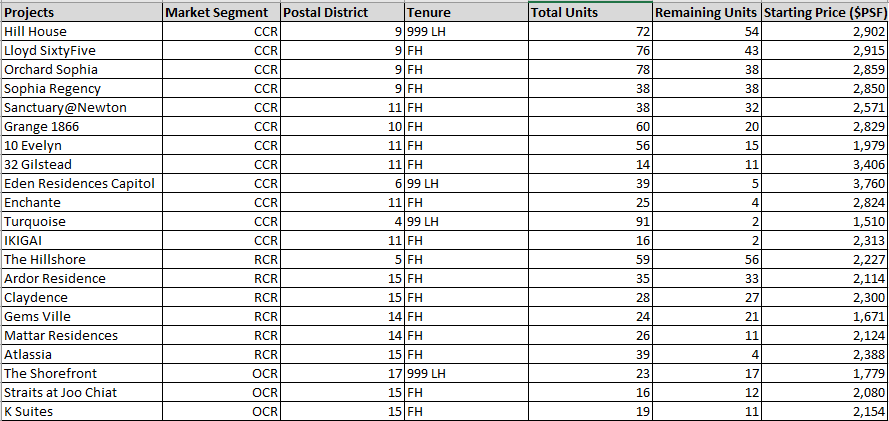

Table 1: New projects on sale in District 15

| Development | Street | Tenure | No. of Units | Price PSF starting from ($) |

| Grand Dunman | Dunman Road | 99-LH | 1,008 | $2,041 |

| Straits at Joo Chiat | Joo Chiat Place | FH | 16 | $2,080 |

| Ardor Residence | Haig Road | FH | 35 | $2,114 |

| Tembusu Grand | Jalan Tembusu | 99-LH | 638 | $2,174 |

| Claydence | Still Road | FH | 28 | $2,300 |

| Atlassia | Joo Chiat Place | FH | 39 | $2,388 |

| The Continuum | Thiam Siew Avenue | FH | 816 | $2,592 |

| Meyer Blue | Meyer Road | FH | 226 | Yet to launch |

| Emerald of Katong | Jalan Tembusu | 99-LH | 846 | Yet to launch |

Source: ERApro as of 14 May 2024, ERA Research and Market Intelligence

What’s There in District 15?

When someone says they live in a property with a sea view, areas such as “East Coast”, “along Siglap” or “the Marine Parade area” come to mind. These areas fall under District 15, where residents staying in high floor units often get to enjoy an immaculate view of Singapore’s South-Eastern coastline and East Coast park.

Source: Map data ©2019 Google, ERA Research and Market Intelligence

While people often associate East Coast Park with District 15, it does not include the entire 18km of reclaimed coastline. Located in both the Outside Central Region (OCR) and the Rest of Central Region (RCR), its locale includes Amber Road, East Coast, Joo Chiat, Katong, Marine Parade, Meyer, and Tanjong Rhu.

There is also a large landed enclave and many small developments scattered across the district, creating a quiet and exclusive atmosphere. In addition, much of the land at Meyer Road and Amber Road has a 999-year or freehold lease, a legacy from the 1800s. At the same time, these areas are within walking distance of amenities, making District 15 a highly coveted estate to live in.

Amenities and Conveniences in District 15

District 15 is home to the famous and history-rich areas of Joo Chiat and Katong. Populated by colonial shophouses, these iconic buildings are now famous for their lifestyle offerings amongst locals and the expat community, with cafes, bars, restaurants, and well-known eateries. There are also several popular schools in the district, such as Victoria School and CHIJ Katong Convent.

Great for nature, exercise and pet lovers

District 15 is a fantastic area to stay in if you are a pet lover. Areas such as Joo Chiat and Tanjong Katong are home to a variety of pet stores and vet practices. This ensures that your animal companions’ needs are always cared for.

There is also a high density of dog-friendly cafes and restaurants in the area. East Coast Park is another highlight for dog owners, as it is not only a fantastic place to walk your dog, but also houses the largest dog run in Singapore. A dog swimming pool, and a pet megamart can also be found there.

The park comes to life, especially on evenings and weekends. From cyclists and fitness enthusiasts, the vast park is home to people of all interests. There are also a variety of food options available, notably seafood restaurants, where families in the area often go to for their meals.

District 15 is seeing improved connectivity in 2024

Previously, the East Coast area used to be ‘neglected’ in terms of connectivity, without access to an MRT line. Partly due to reclaimed land requiring time to settle, there were only bus services to shuttle residents to their workplaces in the city centre or other parts of Singapore.

However, the eastern region of the Thomson-East Coast Line (TEL) will soon be ready by June 2024. It will connect passengers from Bayshore in the East to Woodlands in the North via the Central Business District.

Future plans

It is likely that further changes will come to the area in the future. This is part of the Government’s proposed “Long Island” plan to marry coastal protection measures with new homes, coastal parks, and recreational spaces.

Along the East Coast Parkway, east of District 15, Bayshore will be developed as a smart and sustainable car-lite estate with amenities and recreational spaces. Homes will have sea views. The East Coast Green Corridor will run through this town. This will provide residents with another 20km of upcoming coastal and waterfront parks.

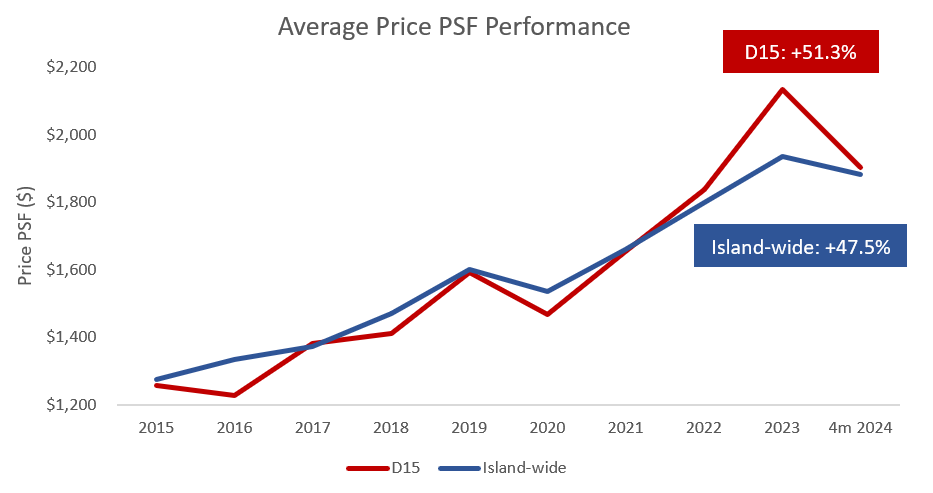

Price Performance

District 15 has outperformed island-wide, in terms of average price per square foot (psf) of units transacted (see Chart 1). Historically, there has been a high demand for homes in District 15 due to its unique location. This has led to people flocking to buy both new and resale properties there.

Chart 1: Price performance of non-landed properties in District 15.

Source: URA as at 14 May 2024, ERA Research and Market Intelligence

We can also expect to see further price uplifts from the MRT effect, with Phase 4 of the TEL set to be opened in June 2024.

As District 15 becomes more connected through enhanced transportation infrastructure and improved amenities, both current owners and potential buyers can anticipate a significant increase in property value and quality of life.

Conclusion

Based on ERA’s proprietary data between 2021 and April 2024, 56.8% of buyers of District 15 new launches were previously living in the East.

For those who live in the East and proclaim “East side, best side”, many of their reasons to support this claim can be traced back to District 15.

If you would like to become an Eastie too, now is the perfect time to make your wish come true. The current inventory of new launch condominiums available will suit the criteria of any buyer. It includes exclusive boutique developments of as small as 16 units (the Straits at Joo Chiat) to sprawling mega developments that house up to 1,008 units (Grand Dunman).

The majority of these new launches are also freehold properties, which is a definite plus for most buyers. To find out more, check out the ERA Projects Online Gallery here, or speak to an ERA Trusted Adviser today!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Every Singapore district has its highlights. District 9 has a world-renowned shopping belt in Orchard Road, District 11 has a growing medical hub, and District 14 has Paya Lebar which will be redeveloped as a “highly liveable and sustainable new town”. The list goes on.

So then, what does District 15 have to offer?

Located in the eastern corner of Singapore, District 15 consists of popular enclaves such as Marine Parade, Joo Chiat, and Katong – areas that are both rich in heritage and prime real estate.

However, those aren’t the only features contributing to the appeal of these towns, and also, not the only reasons why you should consider owning a home in District 15.

1. Plans are in place to improve the liveability of District 15

Though all neighbourhoods in District 15 have their own rich history, that’s not to say they aren’t seeing change.

One of the biggest transformations coming to District 15 is the addition of new MRT stations along the Thomson-East Coast Line (TEL) which will bring greater travel convenience to residents in the east. These include Katong Park station and Tanjong Katong station, both located in the larger Marine Parade planning area.

Meanwhile, Marine Parade MRT station, which too is a stop along the TEL, will bring District 15 residents closer to various suburban shopping malls.

Some examples that long-time east-siders will surely identify with are Parkway Parade and i12 Katong Mall – the latter of which was recently reopened in June last year after a two-year revamp.

Source: URA

Also, located in the vicinity of District 15 enclaves is East Coast Park. With a history dating back all the way to the 1970’s, this 15km-long coastline, which is wholly-built on reclaimed land, has long been a favourite weekend destination among Singaporeans who want some sun and sea in their lives.

Given the Government’s proposed “Long Island” plan to marry coastal protection measures with new homes, coastal parks, and recreational spaces, it’s likely that further changes will be coming to the area in the future.

More recent improvements to East Coast Park include Costal Playgrove, a renovated water play area, as well as the construction of a brand-new Cyclist Park.

Completed in 2021, Costal Playgrove is sited where Big Splash once stood, and like its predecessor, has water play areas that bring relief from the heat. On the other hand, the Cyclist Park, which is found in Area D of East Coast Park, has riding paths for both amateurs and professionals.

Though unrelated to either transport or recreation, the redevelopment of Paya Lebar Airbase is another ‘upgrade’ that’ll potentially change what it’s like to live in District 15.

In his 2022 National Day Speech, Prime Minister Lee Hsien Loong shared plans to relocate Paya Lebar Airbase to make way for more housing space, along with the lifting of building height restrictions in nearby towns. These include Hougang, Punggol, and most crucially, Marine Parade, which falls under District 15.

Ultimately, what this could mean for District 15 residents is the modernisation of existing residential properties either through the Selective En Bloc Redevelopment Scheme (SERS) or a private en bloc sale to create taller homes.

2. Returns on private homes in the area tend to outperform the regional average

District 15 may be best known for its coastline and leisure offerings, but what its residents may not be aware of are the relatively high returns that they can earn on their homes.

Considering that District 15 is primarily located in the Rest of Central Region (RCR), per square foot (PSF) prices for non-landed private residential properties in the latter would serve as a fair benchmark for the performance of equivalent property sale prices in the former.

Data from ERA’s SALES+ app shows that there has been a steady rise in PSF prices for both 99-year and freehold RCR non-landed private properties across the last decade.

Between 2013 to 2023, PSF prices for 99-year private homes in the RCR grew by 26.95% whereas those for freehold private homes rose by 10.36%.

In contrast, average PSF prices for 99-year private properties in District 15 grew 37.17% across the same period, while freehold private homes in the area rose by 32.89%.

These observations are good cause to believe that present owners of private properties in District 15 will enjoy better-than-usual yields on their real estate sales.

Then what about future owners and developments? There’s the possibility that they too will experience positive outcomes due to further price uplifts from the MRT effect following Phase 4 of the TEL’s opening.

What new condominium launches are there in District 15 for 2023?