How Homebuyers Can Benefit from the “Agglomeration” of New Home Launches

- By Egan Mah Jixiang

- 4 mins read

- Private Residential (Non-Landed), Property News

- 10 Apr 2025

This article was written in conjunction with Eugene Lim, Key Executive Officer and Wong Shanting, Head of Research and Market Intelligence of ERA Singapore

The article first appeared in The Business Times BT Property Week section on 9 April 2025.

In recent years, the practice of clustering new home launches within the same neighbourhoods has been growing in prominence. For instance, Tengah and Lentor Hills Estate have seen a staggered rollout of fresh private housing projects, in line with URA’s broader master plan for precinct renewal or development.

Similarly, in the months ahead, we can expect to see similar residential clusters taking shape at Zion Road, River Valley and one north.

Though no formally-adopted term for this trend exists, parallels can be drawn with the concept of “agglomeration” in which businesses cluster to yield synergistic benefits.

From an urban planning perspective, concentrating new home launches in the same neighbourhoods could enhance planning efficiency, resulting in more effective resource allocation when developing new precincts.

This benefit is crucial, as investing in infrastructure for new precincts is a significant undertaking that should not be taken lightly. By strategically clustering new homes in the same area, the Government can ensure that any infrastructure investments are focused on meeting the needs of a larger community.

The clustering of new home launches is nothing new

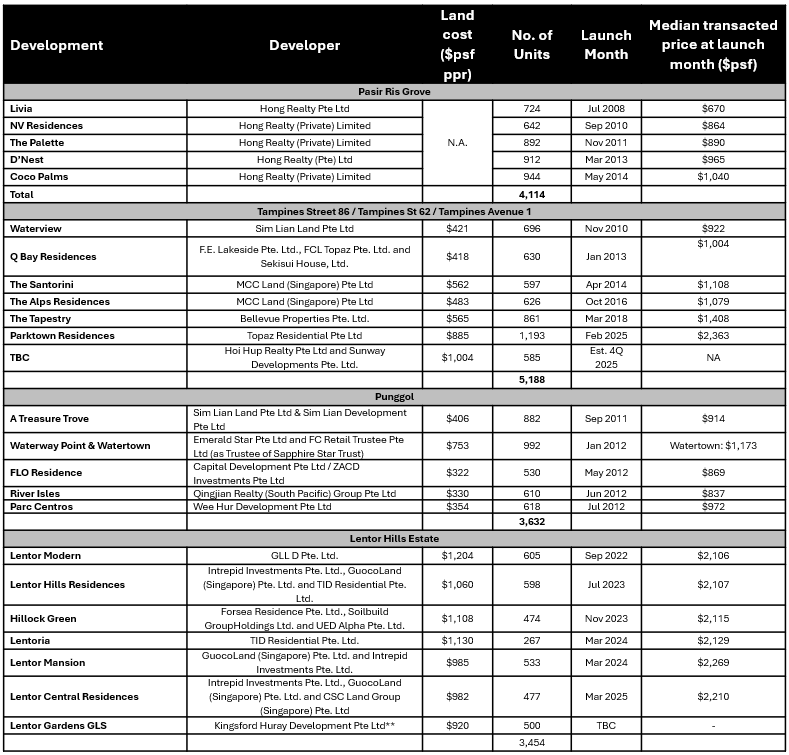

The concept of clustering new home launches is not a new one, having been previously observed in areas such as Pasir Ris, Punggol, Sengkang, and Tampines. In a way, this could be the fastest and most efficient way to developing a new township, whether as an independent entity or as an extension to an existing town.

Between 2008 and 2014, Pasir Ris Grove saw five new homes launches bringing over 4,100 new homes in the vicinity. All five projects were also collectively developed by Hong Realty Pte Ltd. Likewise, between 2010 and 2017, five residential sites along Tampines Street 86 / Tampines Avenue 1 were awarded under the Government Land Sales (GLS) Programme to different developers. Altogether, these five sites yielded some 3,400 units. More recently, five sites, yielding approximately 3,600 units, were sold to drive the development of the Punggol New Town.

This is particularly pronounced in the Lentor Hills Estate cluster, which has seen six launches to date, with another site expected to launch in 2026. Despite initial concerns about a potential supply glut with each successive launch, such fears were allayed as demand for new homes remained robust, evident by healthy take-up rates and rising home prices. GuocoLand, in particular, is the developer behind four of the Lentor Hills Estate developments, allowing them to be bold and experiment with various concepts tailored to meet the diverse needs of homebuyers.

Table 1: Launches in new housing clusters

Source: URA, ERApro, ERA Research and Market Intelligence

*Based on caveats

**Subject to site being awarded

While the clustering of homes is often seen as a strategic move for developers and the government, it also brings about tangible benefits for buyers. Let us explain further below.

1. Buyers get to explore all various projects and make well-informed decisions

One significant benefit is that buyers can ‘shop’ at all the projects almost simultaneously.

This allows them to make an informed decision before committing to their home purchase. By being able to view multiple projects simultaneously, buyers can compare features, layouts and prices more effectively. This transparency and ease of comparison can lead to better decision-making.

Additionally, it reduces the pressure of having to make quick decisions based on limited information, as buyers have a comprehensive view of the new homes launched in the vicinity.

2. New amenities and rejuvenation to support the growing community

The clustering of new homes often acts as a catalyst for urban rejuvenation, prompting the government to introduce new amenities and infrastructure to meet the needs of incoming residents.

For example, the Our Tampines Hub was opened in 2017 to serve the residents of Tampines. In a more recent example, Our Residents’ Hub @ Lentor Estate was opened in end-2024, ahead of the influx of future dwellers.

Another notable example is Pasir Ris, where a new sports and hawker centre was added in the 2010s, alongside the announcement of the new Cross-Island Line with an interchange at Pasir Ris.

Looking ahead, upcoming precincts like Tengah are also expected to benefit from new initiatives and infrastructure developments.

3. Sustained price growth through the clustering of new home launches

In most cases, the clustering of new home launches results in new home prices trending higher with each subsequent launch. This pattern is reinforced by developers pricing latter launches higher due to rising land and construction costs.

Moreover, as the estate matures with the addition of more amenities and robust transportation networks, this leads to prices being pushed further upwards. This dynamic demonstrates the first-mover advantage, whereby early buyers secure lower prices than those who purchase later.

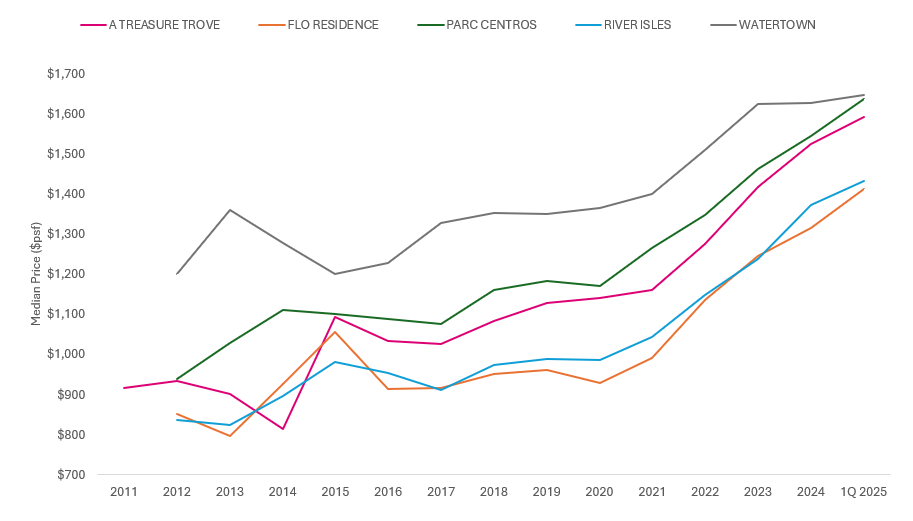

Chart 1: Median Price psf condos at Punggol

Source: URA, ERA Research and Market Intelligence

*For periods without transactions, we estimated prices using the average of the preceding and following transaction prices.

Since their respective debuts, condominiums in the Punggol have delivered a compound annualised returns of between 2.5% and 4.4%, based on median transacted price per square foot ($psf). Even though there are some price differences across the projects, their price trends have generally moved in parallel, reflecting a broadly similar pace of appreciation over time. This observation brings us to our next point.

4. A similar price entry point minimises the risk of losses and supports price growth

With new homes launched at comparable price points, it reduces the likelihood of any owner selling at a loss. This pricing alignment can help maintain market confidence and support steady price appreciation across the precinct.

5. Competition could drive developers to enhance their product offerings

Having successive launches also means more and better options for buyers. With similar locational attributes, developers will compete to offer compelling and unique projects that stand out in the market.

These projects are also often better positioned with higher-quality finishes, a more diverse mix of unit sizes and layouts, and innovative designs aimed at different homebuyer segments.

In an environment where intense competition for the same pool of buyers and price sensitivity both exist, developers will strive to outdo each other. Hence, regardless of whether there are multiple developers or just one developing a few sites within a precinct, homebuyers will be the ultimate beneficiaries of this heightened competition.

This is evident in Lentor Hills Estate, which saw six launches over a 30-month period. In particular, Guocoland has developed four of the six sites awarded in the Lentor Hills Estate. With each launch, Guocoland was able to better anticipate the needs of its buyers. From unit layouts to unit sizes, each development was thoughtfully tailored to suit the needs of different buyers.

Over the past 30 months, we have seen diverse unit configurations. Lentor Modern, launched in September 2022, offers flexible spaces with adaptable layouts designed to meet the post-pandemic needs of families for larger living spaces or dedicated workspaces. Lentor Hills Residences featured dual-key units for investors seeking rental income. Hillock Green and Lentoria focused on larger, more efficient floor plans with squarish layouts and combined living and dining areas ideal for hosting.

6. A large precinct can support an easy exit strategy

With a sizable number of homes in the precinct, homeowners can expect consistent market activity, making it easier to sell their homes when the time comes. This reduces the risk of not being able to find a buyer in the future and helps sustain property values in the long term. Furthermore, a well-planned precinct with amenities and strong transport connectivity tends to attract a continuous influx of potential buyers, which is advantageous for the resale process.

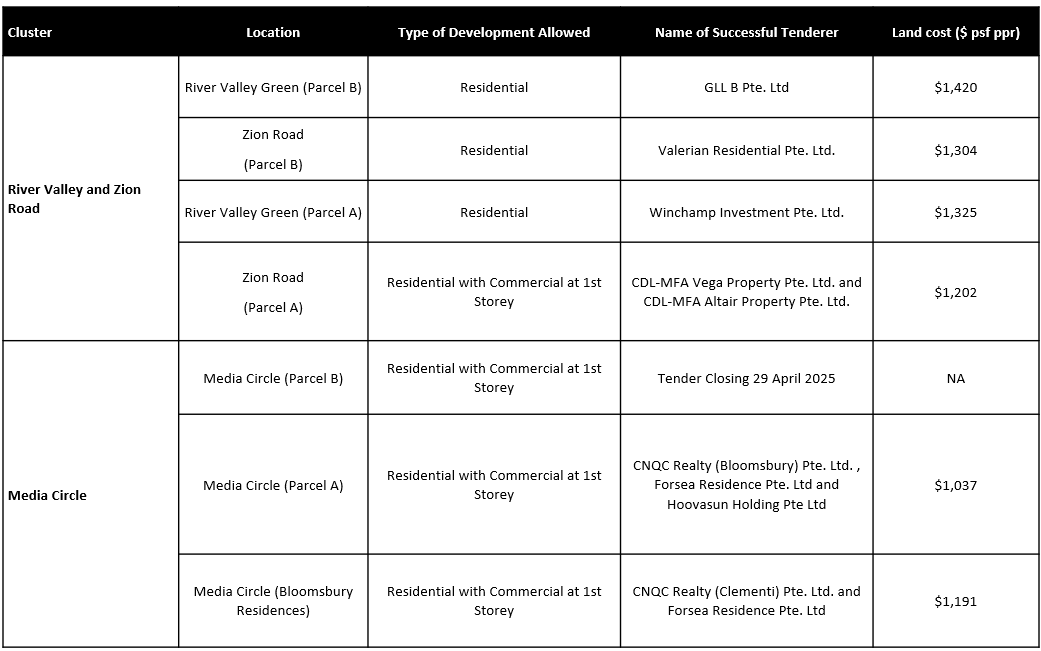

Looking ahead, the next “agglomeration” of new home clusters is expected to take place in the River Valley, Zion Road, and Media Circle precincts. These includes four sites at River Valley and Zion Road cluster as well as three sites at Media Circle.

Table 2: List of Upcoming Clusters

Source: URA, ERA Research and Market Intelligence

Conclusion

In closing, while some buyers may be hesitant about locales with multiple new launches, clear advantages do exist. The ability to view and compare several home launches simultaneously empowers buyers to make well-informed decisions.

Separately, one can also expect new amenities alongside enhanced connectivity that could contribute to long-term price growth. As these precincts mature, the steady influx of homebuyers provides a viable exit strategy, should owners need to sell their homes for any reason.

Looking ahead, the next “agglomeration” of new home clusters is expected to take place in the River Valley, Zion Road, and Media Circle precincts. Could one of new projects be where you call home next?

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.