Private home rental market shows signs of bottoming in 2Q 2024, while the HDB rental market remains resilient.

Private Residential Rental Index

The private residential properties rental index decreased by 0.8% quarter-on-quarter (q-o-q), reflecting a slower pace of growth compared to the 1.9% seen in the previous quarter. This marked the third consecutive quarter of decline.

The Landed property rental index decreased 0.9% q-o-q while the Non-Landed property rental index decreased by 0.8% q-o-q.

The Non-Landed property rental indexes across all regions saw declines in 2Q 2024. Rents for the Rest of Central Region (RCR) and Outside Central Region (OCR) dipped by 1.4% and 1.3% q-o-q respectively, while the Core Central Region (CCR) saw a less significant contraction of 0.1% q-o-q.

Rentals in the CCR seem to have bottomed out as CCR rents have fallen 4.8% y-o-y while demand remains steady. This has prompted renters who had previously moved outwards to return. Moreover, new expats with high incomes and larger rental budgets are more likely to pay extra to live closer to their workplaces or the city centre.

Also, with lower private property rents, some HDB tenants may find better value in renting a private property unit with on-site facilities and better security. Some HDB renters may capitalise on lower private property rents when their tenancy expires as the rental gap between HDBs and condominiums continues to narrow.

Chart 1: Private Residential Rental Indexes

Source: URA, ERA Research and Market Intelligence

Private Rental Contracts

The total number of private non-landed rental contracts rose 1.9% q-o-q in 2Q 2024 to 19,744 transactions. However, this figure is still 9.9% lower than the 5-year average.

Chart 2: Private Residential Rental Contracts

Source: URA, ERA Research and Market Intelligence

With another 6,975 private non-landed units expected to be completed in the 2H 2024, this could potentially lead to more properties being put up for rent , thus further saturating the rental market.

Furthermore, in a high interest rate environment, some landlords may adopt a more practical strategy of securing tenants even at lower rents to ensure that they can cover their mortgages.

HDB Rental Market

Higher HDB median rents across all towns for 3, 4 and 5-room flats

HDB rents are exhibiting an upwards trend, with median rents across all flat types and towns rising by an average of 1.9% y-o-y. This increase was primarily driven by a 3% increase in rents for 2-room flats. Despite the increase in rents, HDB flats remain the most affordable housing option for prospective tenants.

Amidst inflationary pressures and economic uncertainty, some private property tenants have turned cautious, leading them to consider renting HDB flats. However, these tenants typically have a competitively larger rental budget and are willing to pay slightly higher rents to secure choice units. The limited supply and higher demand for HDB flat rentals have prompted the slight uptick in rents.

Table 3: HDB Median Rents in 2Q 2024

| Town |

1-Room |

2-Room |

3-Room |

4-Room |

5-Room |

Executive |

| ANG MO KIO |

– |

* |

$2,800 |

$3,400 |

$3,600 |

* |

| BEDOK |

– |

* |

$2,700 |

$3,300 |

$3,530 |

* |

| BISHAN |

– |

– |

$2,900 |

$3,500 |

$3,800 |

* |

| BUKIT BATOK |

– |

$2,480 |

$2,500 |

$3,200 |

$3,500 |

* |

| BUKIT MERAH |

* |

* |

$2,970 |

$3,800 |

$4,000 |

– |

| BUKIT PANJANG |

– |

* |

$2,600 |

$3,100 |

$3,300 |

$3,530 |

| BUKIT TIMAH |

– |

– |

* |

* |

* |

* |

| CENTRAL |

– |

* |

$3,100 |

$4,400 |

* |

– |

| CHOA CHU KANG |

* |

* |

$2,500 |

$3,100 |

$3,150 |

$3,400 |

| CLEMENTI |

– |

* |

$3,000 |

$3,700 |

$4,000 |

* |

| GEYLANG |

– |

* |

$2,700 |

$3,300 |

$3,700 |

* |

| HOUGANG |

– |

* |

$2,700 |

$3,200 |

$3,350 |

$3,600 |

| JURONG EAST |

– |

* |

$2,700 |

$3,300 |

$3,600 |

$3,830 |

| JURONG WEST |

– |

* |

$2,500 |

$3,300 |

$3,500 |

$3,600 |

| KALLANG/WHAMPOA |

– |

* |

$2,830 |

$3,800 |

$4,100 |

* |

| MARINE PARADE |

– |

– |

$2,850 |

$3,250 |

* |

– |

| PASIR RIS |

– |

* |

* |

$3,200 |

$3,500 |

$3,600 |

| PUNGGOL |

– |

* |

$2,930 |

$3,200 |

$3,300 |

* |

| QUEENSTOWN |

– |

* |

$3,000 |

$3,800 |

$4,300 |

* |

| SEMBAWANG |

– |

$2,400 |

* |

$3,150 |

$3,300 |

$3,400 |

| SENGKANG |

– |

$2,300 |

$2,900 |

$3,200 |

$3,300 |

$3,500 |

| SERANGOON |

– |

– |

$2,600 |

$3,400 |

$3,500 |

* |

| TAMPINES |

– |

* |

$2,800 |

$3,300 |

$3,600 |

$3,850 |

| TOA PAYOH |

– |

* |

$2,750 |

$3,500 |

$4,000 |

* |

| WOODLANDS |

– |

* |

$2,400 |

$3,000 |

$3,300 |

$3,450 |

| YISHUN |

– |

* |

$2,630 |

$3,100 |

$3,300 |

$3,500 |

Source: HDB, ERA Research and Market Intelligence

HDB rental demand holds

Although rents are falling slightly, demand for HDB rentals remains strong. The number of approved applications is 9,554, representing an increase of 1.3% q-o-q, following the 3.6% q-o-q decline in 1Q 2024.

Chart 2: Number of approved applications to rent out HDB flats by flat type

Source: HDB, ERA Research and Market Intelligence

Conclusion

Overall, the moderation in private residential rents has resulted in an increase in the number of rental contracts in 1Q 2024.

Furthermore, with 3,600 private residential units (including ECs) completed in 1H 2024, and approximately 11,300 more units expected to be completed by the end of this year, the market could see further upticks in the number of rent-ready properties. This rise in supply may lead to heightened competition for tenants amongst landlords, possibly softening the rental market further.

With that, ERA predicts a potential easing of private residential rental prices by up to 5% y-o-y in 2024, with the number of rental contracts ranging between 75,000 and 80,000.

When it comes to the HDB rental market, the narrowing gap between HDB and private home rents may encourage some tenants to pay a slight premium for a condominium instead. Nonetheless, the HDB rental market is expected to show resilience due to low inventory, possibly resulting in average rents growing by up to 10% in 2024.

Therefore, ERA forecasts that the number of HDB rental approvals will range between 36,000 to 38,000 contracts in 2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

June saw muted new home sales with the holidays and lack of new home launches.

June 2024 saw muted new sale demand with no new home launches, registering 228 units (excluding Executive Condominiums (ECs)) sold. This marked a 3.2% increase month-on-month (m-o-m).

In addition to this, another 50 units of ECs were sold.

Excluding ECs, the top five selling projects included four projects in the OCR, with one in the RCR.

Best Performing New Launches

Table 1: Top five performing new launch projects

|

Name |

Market segment |

Total units | Number of units sold |

Median price ($psf) |

|

The LakeGarden Residences |

OCR |

306 |

23 |

$2,119 |

|

The Botany @ Dairy Farm |

OCR |

386 |

21 |

$1,979 |

|

Tembusu Grand |

RCR |

638 |

20 |

$2,542 |

|

Hillhaven |

OCR |

341 |

18 |

$2,124 |

|

Pinetree Hill |

OCR |

520 |

15 |

$2,548 |

Source: URA as of 15 July 2024

Three of the top five selling launches, namely The Botany at Dairy Farm ($1,979psf), Hillhaven ($2,124psf) and The LakeGarden Residences ($2,124psf) transacted at prices below the island-wide median new sale transaction price of $2,248psf.

Topping the sales chart for June, The LakeGarden Residences saw 23 units sold at a median price of $2,119 psf. Remarkably, this surpasses the 22 units sold from January to May 2024. Prospective buyers were holding off their purchases until after Sora’s preview, before committing to a decision.

In addition to this, 19 of the 23 units sold at The LakeGarden Residences were 75sqm and larger. This indicates a strong demand for larger sized units for buyers, possibly HDB upgraders, looking for their own stay purposes.

Promise of a major development of the large white site in the Jurong Lake District led by a five-party consortium could have given buyers confidence to purchase a property in the JLD, and fuelled demand for new sale homes in the area.

In second place, the Botany at Dairy Farmmoved 21 units at a median price of $1,979 psft . The project has seen a steady demand over the past quarter, which can be largely attributed to its affordable entry price.

Executive Condominiums

June 2024 saw 50 EC units sold, a 25% increase m-o-m from May. As there were no new ECs launched in the month, these sale numbers were made up of existing stock on the market.

Of these units, 29 of them were from the sale of homes for North Gaia at a median price of $1,311psf. Lumina Grand also moved another 16 units at a median price of $1,508psf.

As the next available new EC projects will only hit the market in 2025, buyers are snatching up remaining stock, especially when they are available at an affordable price point.

Buyer Profile

The doubling of Additional Buyer Stamp Duty rates for nforeig buyers since April 2023 continued to curbed foreign buyer interest in Singapore’s residential property market on a large scale.

Only 11 caveats were lodged by foreign buyers in June 2024, and hese transactions took place in the CCR and RCR market segments.

Chart 1: Buyer profile for all new non-landed homes excluding ECs

Source: URA as of 15 July 2024, ERA Research and Market Intelligence

Luxury Properties (Non-landed Homes $5 mil and above)

Chart 2: Buyer profile for homes transacted at $5mil and more

Source: URA as of 15 July 2024, ERA Research and Market Intelligence

In total, seven luxury homes ($5m and above) were transacted in June 2024. All of these transactions took place in the CCR. Of the seven luxury homes sold, four of them were purchased by foreigners, although from unspecified nationalities. The highest transaction was for a 1,808sqft unit at Midtown Modern, which was sold for $6,688,000, at $3,698psf.

What can we expect in 2H 2024?

Based on our observations, homebuying momentum is likely to pick up in 2H 2024 with the upcoming launch of highly anticipated new projects comprising Sora, Kassia, The Chuan Park, and Emerald of Katong.

In the 2H 2024, ERA expects the launch of approximately 17 new home projects, which will introduce around 8,400 new homes.

Factoring a softer labour and with higher-for-longer interest rates, ERA has revised our new home forecast to between 5,500 to 6,500 units by the end-2024, down from the previous forecast 7,000 to 8,000 units. New home price growth is expected to reach between 4% and 6% y-o-y by end-2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

At present, Singapore’s shophouse market marks a departure from past performance, when transaction volumes were notably higher.

As of 10 July 2024, based on lodged caveats, only 36 shophouses changed hands in the first six months of 2024, amounting to a total transaction value of $341.7 m. This is a far cry from the market’s peak in 2021, which witnessed approximately 245 shophouses with a cumulative worth of $1.8 b being sold in a year.

Year-on-year (y-o-y), compared to 1H 2023, 1H 2024’s transaction volume and value moderation has declined by 53.3% and 52.7% on respectively; these results come on the back of a continued slowdown that initially started in 2H 2023, when only 45 shophouse units were transacted.

Preceding this slowdown, prices of shophouses were inflated by transactions made by buyers linked to the $3b money laundering cases, resulting in a frothy market. These buyers were willing to pay above-normal prices, and with their exit from the market, buying momentum slowed.

Presently, most shophouse sellers are not under distress and are in no hurry to sell. Moreover, with the exception of those facing foreclosure or money laundering investigations, most shophouse sellers have benchmarked their asking prices to past years.

Buyers, on the other hand, are waiting on the sidelines till shophouse prices ease to enhance their prospects for future capital appreciation. Additionally, buyers may also be biding their time due to higher-for-longer interest rates, which have exerted downwards pressure on yields.

Consequently, this mismatch in price expectations between shophouse buyers and sellers has led to a standstill in transactions.

Freehold landed shophouse prices rise year-on-year, while 99-year leasehold counterparts see price decline

Chart 1: Transaction volume and transaction value of landed shophouses

Source: URA as of 10 July 2024, ERA Research and Market Intelligence

Of the 36 shophouses transacted in 1H 2024, 86.1% (31 units) were of Freehold (FH), inclusive of shophouses with 999-year leasehold tenure.

Both these types of shophouses represent compelling investment opportunities, owing to their rarity. Furthermore, due to their immunity to lease decay, these properties are able to hold their value over the long term. A greater number of FH shophouses also contributes to price stability, as they are less susceptible to strong volatility.

Average prices of FH shophouses grew 2.0% y-o-y in 1H 2024. In contrast, 99-year leasehold shophouses saw just four transactions over the past half-year, with average prices falling by 76.7% y-o-y.

There have also been some notable deals made by high-profile family office investors and high-net-worth individuals who were willing to pay a premium. With lower sales, these higher value transactions have a more pronounced effect on average prices in the market.

One of the more notable shophouse deal was The Rail Mall, which Paragon REIT divested for $78.5m on 20 June 2024 to a private investor. The property has a remaining lease of 21 years 8 months.

Chart 2: Average PSF prices for landed shophouses

Source: URA as at 10 July 2024, ERA Research and Market Intelligence

Higher proportion of shophouses transacted below price quantum of $5 million

Some 36.1% of landed shophouses transacted in 1H 2024 were sold for under $5m, while another 25.0% of transactions in the same period were made for $10m or more.

While overall transaction values in the market are falling, the limited supply of landed shophouses have kept demand resilient over the years. Being assets that see capital appreciation, this dip in landed shophouse prices may just be a slight blip as the market corrects.

Chart 3: Price quantum of landed shophouse in the last ten years

Source: URA as at 10 July 2024, ERA Research and Market Intelligence

Singapore shophouse: An asset class that captivates foreign investors

The scarcity of landed shophouses, coupled with Singapore’s robust economy, stable political climate, and low tax regime, have led to these properties being coveted by institutional investors and family offices. Oftentimes as vehicles to achieve their clients’ goals of capital appreciation and wealth preservation.

Earlier in February this year, Business Times reported a high-profile landed shophouse deal, said to have been made by the spouse of Alibaba Group co-founder Jack Ma; having purchased three 99LH shophouses on Duxton Road with balance terms of 63 years.

The deal, which was understood to be worth a combined total of between $45 – $50m, will see the purchased units converted into mixed-use developments with ground-floor restaurants and upper-floor office spaces. The properties were originally acquired by their previous owner for a combined value of $22.2m in 2018.

Popularity of Central Region shophouses

Among the 36 shophouses sold in 1H 2024, 33 were located in the Central Region – an area popular for eateries, fitness studios and co-living spaces. As such, owners of Central Region landed shophouses will likely be able to command higher rents on their properties.

District 8 was the most popular area for landed shophouse buyers, making up half (18 units) of the total transactions in 1H 2024. There could also be opportunities for value buys present in District 8, as seven of these transactions were transacted below $5m.

Chart 4: Top five districts by transactions volume in 1H 2024

Source: URA as at 10 July 2024, ERA Research and Market Intelligence

Table 1: Top five shophouse transactions in 1H 2024

| Development | Address | District | Transacted Price ($) | Land Area (sqft) | Unit Price PSF ($) | Transaction Date |

| The Rail Mall | 380, 382, 384 ETC Upper Bukit Timah Road | 23 | 78,500,000 | 105,563 | 744 | 20 Jun 2024 |

| Kreta Ayer Conservation Area | 31 Pagoda Street | 08 | 19,000,000 | 1,310 | 14,504 | 13 Mar 2024 |

| Geylang Conservation Area | 223,225,227 Geylang Road | 08 | 18,680,000 | 4,319 | 4,326 | 26 Feb 2024 |

| Telok Ayer Conservation Area | 182 Telok Ayer Street | 01 | 16,500,000 | 1,429 | 11,543 | 28 May 2024 |

| Kreta Ayer Conservation Area | 35 Mosque Street | 01 | 15,930,000 | 1,202 | 13,249 | 6 Mar 2024 |

Source: URA as at 10 July 2024, ERA Research and Market Intelligence

Shophouse demand expected to remain subdued in 2024

Amid rising prices and softer yields, the demand for landed shophouses is expected to stay soft this year. However, their allure as proven assets that are low in supply may keep investors and institutional funds interested, assuming that interest rates start to come off in the coming months.

However, their allure as proven assets remain owing to their rarity and heterogeneity, as no two shophouses are identical. Furthermore, shophouses are zoned Commercial, they are not subject to Additional Buyer’s Stamp Duty and Seller’s Stamp Duty. Correspondingly, unlike residential properties, commercial shophouses have no restrictions on foreign ownership.

Owing to the abovementioned qualities, shophouses will still hold appeal for foreigners and entities, such as institutional funds, who wish to hold local property in their portfolios. As such, should interest rates come off, we can anticipate a growth in shophouse transaction volumes.

Furthermore, should banks put up more shophouses seized from money laundering cases at lower asking prices, we may witness a correcting effect on the market, subject to transaction outcomes.

Likewise, if the gap between sellers and buyers’ price expectations narrows, we are likely to see more shophouse transactions take place, albeit without any strong fluctuations in prices. Otherwise, a continued stalemate will lead to transaction volumes dwindling further.

Based on these factors, ERA forecasts the landed shophouse transaction volume for 2H 2024 to be between 40 to 50 units. This prediction will take the total transaction volume to between 75 to 85 units for the year. Finally, we project the total transaction value for landed shophouses to range between $800m – $900m for the entirety of 2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Singapore’s private property market continued to slow down one year after the adjustments to Additional Buyer’s Stamp Duty (ABSD) rates were introduced in April 2023.

Furthermore, buyers have turned cautious and have pushed back their homebuying plans amid strong headwinds from slower economic growth. This has been further compounded by higher-for-longer interest rates and the higher cost of replacement homes.

Residential Home Prices

Based on flash estimates, the All-residential property price index reported a modest quarter-on-quarter (q-o-q) increase of 1.1% in 2Q 2024 compared to the 1.4% increase in 1Q 2024.

Prices of non-landed properties increased by 0.9% in 2Q 2024, compared to an increase of 1.0% in the previous quarter. Prices of non-landed properties in the Core Central Region (CCR) decreased by 0.2%, compared to the 3.4% increase in the previous quarter.

Prices of non-landed properties in the Rest of Central Region and Outside Central Region increased by 2.2% and 0.3% respectively, compared to an increase of 0.3% and 0.2% in the previous quarter respectively.

For landed properties, prices increased at a more gradual pace of 1.8% in 2Q 2024, compared to the 2.6% increase in the previous quarter.

Affordability remains a top concern for homebuyers. Despite rising prices, nearly 4 out of 5 non-landed homes sold in 2Q 2024 were priced below $2.5 million, with many buyers compromising by choosing smaller home sizes in order to keep within this price range.

Overall, 42.6% of the caveats were recorded within the sweet spot price range of between $1.5mil and $2.5mil.

Chart 1: Residential Price Indices

*Based on flash estimates

Source: URA as of 1 July 2024, ERA Research and Market Intelligence

Transaction Volume

According to URA flash estimates, sale transaction volume (up to mid-June) totalled 4,215 in 2Q 2024, compared to 4,230 in 1Q 2024.

Based on caveats lodged, islandwide non-landed private property transactions have dropped to 3,591 units, falling by 8.9% q-o-q and 29.7% y-o-y, the lowest observed since 4Q 2022.

On the back of fewer launches in 2Q 2024, new sale transaction volume fell to its lowest since 4Q 2022. New sale transaction volume fell to just 663 transactions, marking a decline of 41.8% q-o-q and 68.0% y-o-y. This is the lowest seen since 4Q 2022. In 2Q 2024, there were only six new projects launched.

Among which, two of the launches were luxury developments, Skywaters Residences and 32 Gilstead, which sold at a median price of $6,100 psf and $3,455 psf respectively.

Demand in the secondary market fell marginally by 3.7% y-o-y to 2,928 units in 2Q 2024.

Chart 2: All non-landed private residential transactions

Source: URA as of 1 July 2024, ERA Research and Market Intelligence

CCR

Non-landed private home transaction volume in the CCR fell by 41.8% q-o-q and 68.0% y-o-y to 663 units in 2Q 2024.

The CCR market, which typically sees the largest proportion of foreign buyers has remained suppressed due to the increase in ABSD rates for foreigners since last April.

The recent price adjustments at Cuscaden Reserve and The Residences at W Singapore Sentosa Cove have sparked much-needed buyer activity in the CCR market, providing value buys for investors.

RCR/OCR

The total transaction volume in Rest of Central Region (RCR) more than halved in 2Q 2024 compared to 2Q 2023 with just 1,142 transactions. The decline was attributed to fewer new homes launched in 2Q 2024 compared to a year ago.

In the Outside Central Region, the number of transactions rose 13.0% y-o-y to 1,823 in 2Q 2024 compared to 1,613 in 2Q 2023.

The RCR and OCR regions continue to be largely supported by homeowners and HDB upgraders who are attracted to locations with upcoming redevelopment, as well as areas that will see improved connectivity in the long term.

However, these buyers tend to be price sensitive and would typically buy within the sweet spot price quantum.

2H 2024 Government Land Sale (GLS) Programme

To continue to cater to housing demand and maintain market stability, the URA has ten sites on the Confirmed List and nine sites on the Reserve List in the 2H 2024 GLS program.

On the Confirmed List, there are nine residential sites, inclusive of an executive condominium (EC) plot, and a residential and commercial plot. There will be a total supply of 11,110 private residential units created via the Government Land Sales Programme in 2024 – the highest in a single year since 2013.

Outlook

Based on our observations, homebuying momentum is likely to pick up in 2H 2024 with the upcoming launch of highly anticipated new projects comprising SORA, Kassia, The Chuan Park and, Emerald of Katong.

In 2H 2024, ERA anticipates up the launch of approximately 17 new home projects, which will introduce around 8,400 new homes.

Factoring current market conditions, ERA has revised our new home forecast to between 5,500 to 6,500 units by the end-2024, down from the previous forecast 7,000 to 8,000 units. New home price growth is expected to reach between 4% and 6% y-o-y by end-2024.

In terms of the secondary market, ERA expects the CCR to continue seeing subdued demand, while RCR and OCR demand should hold with support from local buyers.

ERA holds our project the secondary market. The total resale and subsale transaction volume could reach between 26,000 and 27,000 units, with price expected to rise by 4% to 5% y-o-y in 2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Following April’s 57.7% month-on-month (m-o-m) fall in new sale numbers, May 2024 saw a further decline of 25.9% m-o-m to 261 units (including Executive Condominiums (ECs). This is on the back of the launches of smaller developments such as Skywaters Residences (198 units) and two boutique projects – Straits at Joo Chiat (16 units) and Jansen House (20 units).

A total of 248 new private homes were launched in May, compared to 278 units in April. This marked a 10.8% m-o-m decrease. Correspondingly, a total of 221 new homes, excluding ECs, were sold, registering a 26.6% m-o-m decrease.

EC sales momentum slowed in May 2024, with 40 units sold. With no new EC launches since January 2024, buyers are snapping up the remaining units of current EC stock. North Gaia (19 units) and Lumina Grand (20 units) accounted for 97.5% of EC units sold, with the other sold unit from Provence Residence.

EC stock fell to only 299 new EC units remaining across the five projects – North Gaia, Altura, Lumina Grand, Parc Greenwich and Tenet. Demand for ECs is likely to stay subdued until the current stock of limited options is fully sold, given the limited selection. The next ECs will likely only be launched in early-2025. as the Plantation Close and Tampines Street 62 (Parcel B) sites were awarded in September and October 2023 respectively.

Best Performing New Launches

Table 1: Top five performing new launch projects (excluding EC)

|

Development |

Market Segment |

Total units |

Number of Units Sold |

Median Price ($psf) |

|

Lentor Hills Residences |

OCR |

598 |

25 |

$2,164 |

|

Hillhaven |

OCR |

341 |

23 |

$2,099 |

|

Hillock Green |

OCR |

474 |

21 |

$2,128 |

|

The Botany at Dairy Farm |

OCR |

386 |

18 |

$1,968 |

|

The Myst |

OCR |

408 |

17 |

$2,152 |

Source: URA as of 18 June 2024, ERA Research and Market Intelligence, ERApro

Excluding ECs, all five top performing developments were found in District 23 (Bukit Batok, Bukit Panjang) or District 26 (Mandai, Upper Thomson) of the Outside Central Region (OCR).

Lentor Hill Residences was the best-selling project in April, with 25 units sold at a median price of $2,164 psf. The development has now sold 88.1% of its 598 units. Following Lentor Mansion’s launch in March at benchmark prices in the Lentor Hills Estate, there was an uplift in prices for the surrounding developments that were launched previously. The median price psf for Lentor Hills Residences’ increased from $2,114 psf in March to $2,164 psf in May 2024. Similarly, Hillock Green also moved another 21 units at a median price of $2,128 psf, increasing from $2,109 psf in March.

Homes in District 23 ($2,047 psf) and 26 ($2,176 psf) presented value buys for new home buyers as their median prices are below the island-wide median of $2,206 psf (excluding ECs) in May 2024.

ECs continue to provide a strong value proposition for buyers due to the subsidies provided. However, with no new EC launches till early-2025, buyers will continue to take up existing units in the market, seen from the moving of 39 units from Lumina Grand and Altura.

Buyer Profile

Singaporeans made up the majority of new non-landed home buyers (82.5%) in May 2024, marginally lower than the 82.3% in April. Foreign buyers accounted for another six transactions (2.7%).

May 2024 also marks one year since the doubling of Additional Buyer Stamp Duty rate for non-permanent resident (PR) foreign buyers to 60%. Between June 2023 and May 2024, foreign buyers only accounted for an average of 3.1% of total new sale buyers each month. This is significantly lower than the previous 12-month period, where foreign buyers accounted for an average of 11.2% of new sale transactions each month.

Chart 1: Buyer profile for all new non-landed homes excluding ECs

Luxury Properties (Non-landed Homes $5 mil and above)

Nine luxury new homes were sold in May 2024. Of these nine units, four were purchased by Singaporeans, four by Singapore Permanent Residents (SPRs), and one by a non-PR foreigner. The luxury home purchased by the foreigner was a 7,761 sqft unit at Skywaters Residences that transacted for $47.3 million, wherein the buyer shelled out $28.4 million for the ABSD.

These nine transactions were across six different developments in the Central Region. Seven of them were in the Core Central Region (CCR) while two are in the Rest of Central Region (RCR). The two luxury home transactions in the RCR were at The Reserve Residences, which has sold 93.7% of its 732 units since its launch in May 2023. Despite being in the city fringe, buyers are willing to pay a premium for large sized units in an integrated development which offers convenience and easy accessibility.

19 Nassim and Watten House also moved another two luxury home units each, owing to the fact that they are developments with prestigious address that are attractive to high net worth buyers.

Chart 2: Buyer profile for home $5mil and more

Source: URA as of 18 June 2024, ERA Research and Market Intelligence

New Home Sales Momentum to Remain Slow with No New Launches Slated for June

June 2024 will likely continue to see subdued sales as there are no expected launches. Moreover, the school holiday period seasonally sees more subdued sales as more people travel out of the country

New home buying activities could only start picking up in 2H 2024. Kassia (280 units) and Sora (440 units), two small-to-mid sized developments in Changi and Jurong Lake will be open for booking in July 2024. Moreover, highly-anticipated large projects such as The Chuan Park and Emerald of Katong slated for launch in 3Q 2024 are expected to capture the interest of home buyers and boost new home sales.

For now, buyers are cautious and remain sensitive to overall price quantum especially since interest rates are likely to stay elevated for longer. The initial forecast of rate cuts may be delayed further into 2024, given the persistent high inflation rate in the US. However, we could see the return of buyer interest once the rate cuts are implemented in the later part of the year.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

April 2024 saw a decline in new home sales due to muted new home launches.

A total of 278 new private homes were launched in April, compared to 877 units in March. This represents a decrease of 68.3% month-on-month (m-o-m). April’s new homes sale numbers fell 58.8% m-o-m to 352 units (excluding ECs).

With no new EC launch, buyers have snapped up the remaining unsold EC stock. April saw the sale of another 51 units, and North Gaia accounted for 64.7% of the transactions. The number of unsold EC stock fell 8.1% m-o-m to 329 units.

There were three new launches in April namely, The Hill @ One North (142 units), The Hillshore (59 units) and 32 Gilstead (14 units).

32 Gilstead is a ultra luxury freehold development in the Core Central Region (CCR) moved four of its 14 units (28.6%). These transacted units are of at least 4,100 sqft and sold for upwards of $14.2 million to local buyers.

While The Hill @ One-North and The Hillshore are located in the Rest of Central Region (RCR), they are situated outside the typical heartland areas. Hence, they appeal to a distinct group of buyers, which explains for their gradual sales rate.

The Hillshore moved three of its 59 units (5.1%) at a median price of $2,599 psf.

Among the three new launches in April, The Hill @ One-North performed the best, selling 42 of its 142 units (29.6%) at a median price of $2,614 psf.

Best Performing New Launches

Table 1: Top five performing new launch projects

|

Development name |

Market segment |

Total units |

Number of Units Sold |

Median Price PSF ($) |

|

The Botany at Dairy Farm |

OCR |

386 |

50 |

$2,003 |

|

The Hill @ One-North |

RCR |

142 |

42 |

$2,614 |

|

North Gaia (EC) |

OCR |

616 |

33 |

$1,315 |

|

Hillhaven |

OCR |

341 |

22 |

$2,080 |

|

Pinetree Hill |

RCR |

520 |

18 |

$2,439 |

|

Lumina Grand (EC) |

OCR |

512 |

18 |

$1,515 |

Source: URA as of 15 May 2024

Four of the top five performing developments were found in the Outside Central Region (OCR).

The Botany at Dairy Farm was the best-selling project in April, with 50 units sold at a median price of $2,004 psf. With new OCR projects transacting at a median of $2,204 psf as at April, The Botany at Dairy Farm is a value buy for new home buyers.

North Gaia was the best-selling EC project in April, moving another 33 units at a median price of $1,315 PSF. Lumina Grand also moved another 18 units at a median price of $1,515 psf.

Buyer Profile

Singaporeans made up the majority of new home buyers (82.9%) in April 2024, a decline from 91.6% in March. Foreign buyers accounted for another 10 transactions (3.4%).

Chart 1: Buyer profile for all new non-landed homes excluding ECs

Source: URA as of 15 May 2024, ERA Research and Market Intelligence

Luxury Properties (Non-landed Homes $5 mil and above)

Chart 2: Buyer profile for homes transacted at $5mil and more

Source: URA as of 15 May 2024, ERA Research and Market Intelligence

Twelve luxury new homes were sold in April 2024. Of these twelve units, five were purchased by Singaporeans, six by Singapore Permanent Residents (SPRs), and one by a foreigner. The luxury home purchased by a foreigner was a 1,851 sqft unit at Watten House was transacted for $6.2 million.

Five of these 12 luxury homes were at Watten House, which has sold 78.9% of its 180 units since November 2023. Another four units were sold at 32 Gilstead, targeting high-net-worth buyers with prices starting at $13 million.

The highest-transacted property was a 4,209 sqft unit at 32 Gilstead, purchased by a local buyer for $14.5 million ($3,455 PSF).

Singapore residents accounted for 91.7% of new home luxury market sales in April, as the punitive ABSD rates continue to deter foreign buyers.

New home sales momentum to remain slow in May with only one boutique development being launched

May will only see the launch of Straits at Joo Chiat, a boutique development comprising 16 units.

New home buying activities could only pick up after July as we expect fewer launches in May and June.

In 2H 2024, highly anticipated projects such as The Chuan Park (916 units) and Emerald of Katong (846 units) are expected to capture home buyers’ interest and boost new home sales.

Amid the economic headwinds, geopolitical instability, rising retrenchment exercises and higher-for-longer interest rates, buyer sentiment remained lukewarm. Furthermore, there have been emerging concerns around the persistently high inflation rate in US which could impact the Federal Reserve’s decision to cut interest rates this year. As a result, some prospective homebuyers may hold back on home purchases till second half of the year.

Barring any unforeseen circumstances, ERA forecasts new home sale to ranging between 7,000 and 8,000 units in 2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

HDB has launched the Resale Flat Listing (RFL) service to create a transparent, reliable and trusted marketplace for the listing and transactions of HDB resale flats. Flat owners or their property agents can list flats for sale and complete their resale transactions on the HDB Flat Portal.

The RFL service will soft launch on 13 May 2024 while the official launch is set to be on a later date within the same month. The RFL service is the latest enhancement to the HDB Flat Portal and will be free of charge for the time being.

Why has HDB launched the Resale Flat Listing Service?

1. Improve convenience for buyers and sellers of HDB flats

Since 2018, HDB has launched the HDB Resale Portal to streamline and simplify the resale transaction process. Subsequently, the HDB Flat Portal was launched to complement the HDB Resale Portal for home buyers and sellers to gather information on the purchase (new or resale) or sale of a flat, on a single integrated platform. Some of the enhancements include one-stop loan listing service, customisable financial calculators, as well as information on the HDB Flat Eligibility (HFE) letter.

The RFL service is the part of HDB digitalisation efforts aligned with the government’s Real Estate Industry Transformation Map strategies. The aim of the industry transformation map is to use technology to deliver seamless and efficient property transaction services.

2. RFL to help verify HDB buyers and sellers

The RFL will help weed out fake HDB listings, which is pervasive on listing portals, through verification of resale listings.

For flats sellers with a valid Intent to Sell, they can either choose to appoint a property agent to manage their flat listing on the HDB flat portal, or list and market their flat on their own. But each seller can only post one flat listing to ensure that there is no duplicative listing for the same flat.

Even though any prospective flat buyer can browse the flat listings on the RFL service, only those with a valid HFE letter can obtain the sellers’ contact details, allowing them to schedule viewing appointments through the HDB Flat Portal.

3. RFL to help manage sellers’ price expectations which will ensure a more sustainable property market in the long run

The system will prompt the seller if the listed price is 10% higher than the last transacted price in the vicinity over the past six months. This feature helps sellers stay informed about recent resale prices and allows them adjust their listing price to better reflect market conditions.

Are real estate agents still relevant with the launch of the Resale Flat Listing?

The biggest question on everyone’s mind would be, “will real estate agents and listing portals become a thing of the past for the HDB resale market?”

1. A real estate agent can help navigate the complex HDB sales process

For many consumers, transacting an HDB flat might only happen once or twice in their lifetime. With the constantly evolving HDB resale rules and paperwork, the resale process can seem daunting for many consumers.

By engaging a real estate agent, sellers and buyers can receive guidance on the up-to-date processes and advice how they can approach the sales process efficiently.

2. Real estate agents to negotiate in your interest, and help brokerage the best deal

Some real estate agents specialise in certain housing estates, which enables them to develop strong market insights and intelligence. In this way, they can help sellers conduct thorough competitive market analysis, and have proven to bring sellers the best possible price achievable for their units.

Beyond just negotiating prices, real estate agents serve as intermediaries between buyers and sellers, helping them to align on intangible aspects such as the submission dates and HDB appointment dates.

To illustrate, a seller must ensure the delivery of his HDB unit after they have moved into their next home. This will require extensive coordination, from managing the flow of funds from the sale to the purchase, to timing the move and settling into the new place before the handover of the existing flat.

3. Business as usual for listing portals even though they are expected to a decline in HDB listings

For the time being, the RFL service will be free of charge allowing HDB sellers with their exclusive property agents to save on advertisement cost.

Furthermore, since the RFL will allow only allow sellers with a valid Intent to Sell to post their listings, this will help weed out fake HDB listings, which is pervasive on listing portals.

With the RFL, we anticipate HDB sellers will be less reliant on existing listing portals, and that could lead to a decline in HDB listing on such portals.

We believe the RFL will benefit real estate agents who focus on exclusive listings and here’s why:

4. Savings on advertisement cost for HDB real estate agents

Once appointed by the HDB sellers, the HDB real estate agent can leverage on the RFL to advertise the listing. For now, the RFL is free of charge and this can translate to savings on advertisement cost.

5. Pre-qualified buyers for the listings

The RFL allows any prospective flat buyer to browse the flat listings but those with a valid HFE letter can obtain the sellers’ contact details, allowing them to schedule viewing appointments through the HDB Flat Portal.

This ensures that the prospective buyers are pre-qualified before the viewing, which may not be the case for now. Currently, some buyers may not have completed the necessary loan assessment before viewing the flats, and this impedes their ability to make an offer.

Separately, some buyers may be looking to take a bank loan for their upcoming HDB purchase, and for now the RFL does not cater to this group of buyers.

6. RFL will help to manage sellers’ price expectations

The system will prompt the seller if the listed price is 10% higher than the last transacted price in the vicinity over the past six months. This feature helps sellers stay informed about recent resale prices and allows them adjust their listing price to better reflect market conditions.

7. Providing a more accurate reflection on the available listings in the market

For real estate agents serving buyers, having an accurate overview of the available listings in the market helps them facilitate appointments more efficiently. They no longer need to sift through fake listings on listing portals, enabling them to better inform their buyers about market conditions and advise on realistic buying prices.

In a nutshell, the RFL is poised to offer greater transparency to the HDB market, fostering more sustainable price growth over time term. However, it faces some initial challenges such as facilitating contact between buyers using bank loans and sellers to arrange viewings. Sellers must also be ready to be overwhelmed by non-serious enquires from buyers and real estate agents. Overall, we view the RFL as a significant step towards improving transparency and efficiencies of the real estate market. Real estate agents should work alongside with the RFL to enhance their professionalism and service to their clients.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Ask any Singaporean what they think of Sentosa Cove and you may hear responses like “posh,” “rich,” or “symbol of status”. Sentosa Cove is all about swanky cars and over-the-top architecture, representing the upmarket community it embodies.

When the Sentosa Cove Masterplan was first conceptualised in 1992, Sentosa Cove was envisioned to be Singapore’s exclusive waterfront resort living, mimicking Port Grimaud in France. The idea was to offer another housing option for wealthy individuals and families seeking respite from the urban hustle and bustle, yearning for the resort lifestyle seen in places like Dubai’s Palm Jumeirah or Florida’s Palm Beach.

Because of this, foreign buyers, who are non-permanent residents, may apply to acquire a piece of landed property at Sentosa Cove, and approvals are generally granted.

Two decades after its first land parcel was sold, Sentosa Cove has seen moderate success but has fallen short of lofty expectations. Home prices in Sentosa Cove continue to languish and have failed to keep pace with Core Central Region (CCR) home price growth. In this piece, we will review Sentosa Cove and unpack its relevance in the Singapore housing market today.

The birth of Sentosa Cove – there are only so many homes here

With the sale of its first land parcel in 2003, Sentosa Cove heralded a new era of luxury waterfront living in Singapore. By 2006, the first development on Sentosa Cove was completed, and by 2008, all land parcels had been sold. Sentosa Cove was paving its way towards becoming a prestigious waterfront community, enticing individuals with deep pockets from around the world to invest in Singapore.

Zoned within the CCR, Sentosa Cove boasts of some 2,160 residential homes; approximately 16% are landed homes. This makes up about 0.5% of islandwide private home stock. Despite all homes at Sentosa Cove being on 99-year leases, the allure of spacious waterfront lifestyles and coveted addresses are compelling reasons for one to aspire to own a piece of Sentosa Cove. According to Squarefoot research, Singaporeans account for close to 50% of the buyers of new homes at Sentosa Cove, with Singapore Permanent Residents and Foreigners accounting for 21% and 23% respectively.

However, apart from non-landed properties, there are some restrictions around buying Sentosa Cove landed properties. For instance, foreigners are only allowed to purchase one detached house for their own use. In the past, the Long-Term Visit Pass scheme granted foreign buyers in Sentosa Cove long-term stays within Singapore, but the scheme was terminated in 2014. In contrast, Singaporeans face no restrictions on the number of detached houses they can buy, and there are also no limitations when leasing these units.

Two decades on, Sentosa Cove has blossomed into a self-sufficient upscale neighbourhood

Today, Sentosa Cove has evolved into a luxurious neighbourhood where living next door to influential and affluent personalities is the norm. It’s a melting pot of local homeowners and expatriate tenants, adding to its cosmopolitan allure.

Beyond its curated selection of restaurants along Quayside Isle and nearby hotels, Sentosa Cove boasts amenities like supermarkets and several preschools, catering to the diverse needs of its residents.

The nearby ONE°15 Marina Sentosa Cove yacht club and the renowned Sentosa South Golf Island offer not just leisure and recreational opportunities but also serve as hubs for socialising among the well-heeled.

Homes in Sentosa Cove are highly coveted for the status symbol and lifestyle they represent. Landed homes, in particular, can be customized to owners’ preferences, with some known for their quirky architecture.

Moreover, the luxury of space allows for ample room to host functions and dinners, enabling residents to showcase their homes to relatives, friends, and, importantly, business partners.

How have home prices at Sentosa Cove fared so far?

We’ve segmented our analysis into three distinct time periods to explore the evolving dynamics and challenges of Sentosa Cove. Each period reflects unique market conditions shaped by factors such as government policies, economic trends, and external events. Given Sentosa Cove’s prestigious status, we’ll be juxtaposing its home prices with those in the CCR.

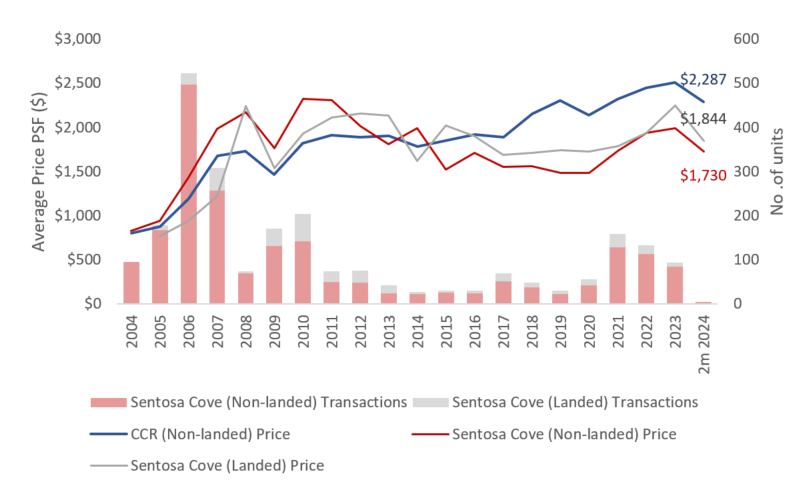

Conception of Sentosa Cove (2004 – 2010)

With successive new home launches in the area, Sentosa Cove experienced robust home sales and significant price growth. Transaction volume steadily rose, reaching a peak in 2006 with 522 transactions. During this period, both non-landed and landed property prices in Sentosa Cove saw substantial appreciation. Non-landed properties surged from $829 per square foot (psf) in 2004 to $2,325 psf in 2010, while landed properties followed a similar trajectory, climbing from $765 psf to $1,933 psf.

Pre COVID-19 (2011 – 2019)

Between 2011 and 2020, multiple rounds of cooling measures effectively dampened foreign buyer interest in Sentosa Cove. Additionally, global economic headwinds exacerbated the decline in foreign buyer demand, leading to a notable decrease in both home prices and transaction volume in Sentosa Cove. By 2015, the average non-landed home prices had plummeted by 34.4% from their peak in 2010, while landed homes experienced a more gradual price decline.

After 2017, home prices in Sentosa Cove began to gradually decline, in stark contrast to the continued increase in prices observed in the CCR.

COVID-19 and Post-COVID-19 (2020 – 2023)

From 2020 to 2023, a post-COVID housing demand boom characterized the market, fueled by pent-up demand and renewed interest from buyers in Sentosa Cove. During this period, prices for non-landed properties in Sentosa Cove increased by 16.2%, while landed properties saw a growth of 6.8%. Transaction volume in 2021 reached a 10-year peak, reflecting heightened market activity in Sentosa Cove. However, the market’s momentum slowed thereafter due to the April 2023 Additional Buyer Stamp Duty (ABSD) hike, imposing a hefty 60% tax on foreign buyers purchasing residential properties.

Additionally, the slew of money laundering cases in headlines during 2023 led to increased caution among buyers, prompted by more stringent checks and unwanted scrutiny. Despite the recovery in home prices at Sentosa, the home prices remained comparatively lower than homes in the CCR.

Chart 1: Homes at Sentosa Cove

Source: URA as at Feb 2024, ERA Research and Market Intelligence

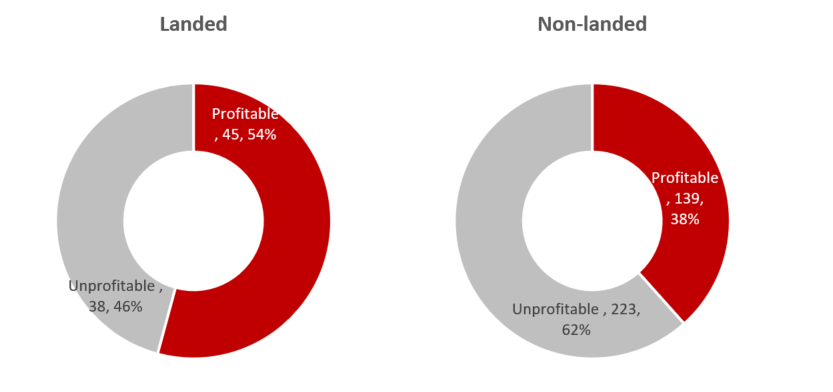

Around 41% of Sentosa Cove transactions were profitable in the last ten years

In the last ten years, about 40% of transactions in Sentosa Cove were profitable. However, it’s noteworthy that landed homes outperformed non-landed ones in terms of profitability. Specifically, 54% of landed home transactions in Sentosa Cove reported an average median gross profit of $3.6 million. In contrast, during the same period, only 38% of non-landed home transactions in Sentosa Cove resulted in a profit, with an average median gross profit of $587,000.

Chart 2: Transactions in Sentosa Cove (2013-2023)

Source: URA as at Feb 2024, ERA Research and Market Intelligence

Sentosa’s rental market

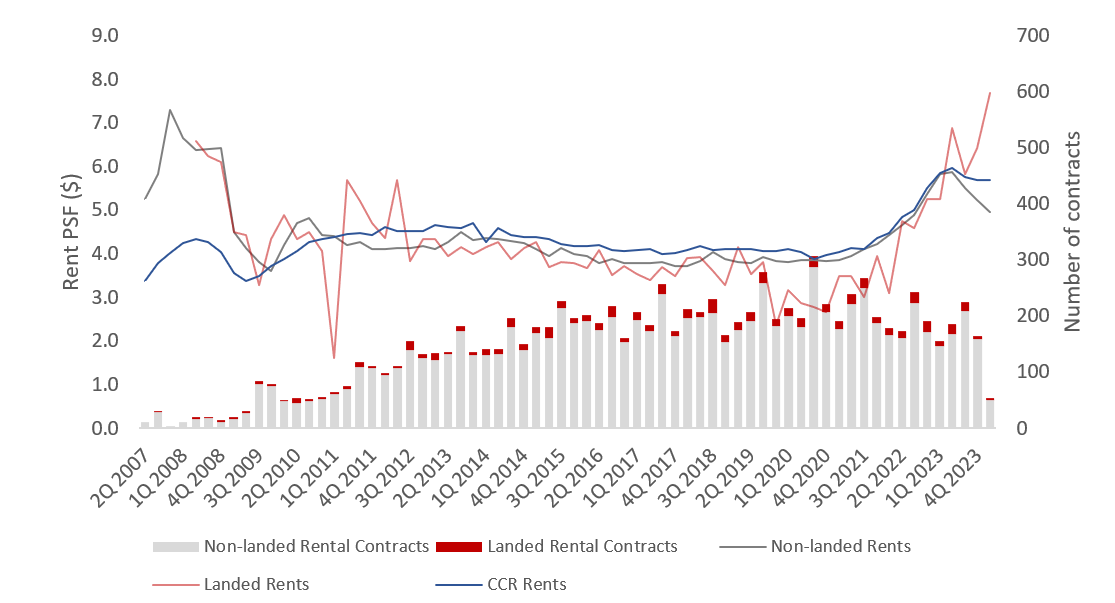

Between 2015 and 2023, Sentosa Cove saw an average of 764 non-landed units and 57 landed homes being rented out yearly. This accounted for almost 38% of the total homes at Sentosa Cove. Non-landed rents at Sentosa Cove are comparable to those in the Core Central Region (CCR), while landed rents at Sentosa have been rising and are now at their all-time peak. High-net-worth tenants looking for waterfront homes are willing to pay higher rents for these rare units.

Chart 3: Median Rents and Rental Contracts in Sentosa Cove

Source: URA as at Feb 2024, ERA Research and Market Intelligence

Sentosa Cove – the comeback kid

Sentosa Cove to benefit from the Sentosa-Brani Masterplan development

Announced in 2019, the Sentosa-Brani Masterplan had a vision to transform the island into a game-changing leisure and tourism destination. There will be five zones across the island that will see new indoor and outdoor attractions for families, nature lovers, and adventure seekers. In addition, the opening of the 30,000 square meter (sqm) multisensory two-tiered walkway will integrate and connect Resorts World Sentosa in the north with Sentosa’s beaches in the south. Redevelopment works at Sentosa are part of the plans for the Greater Southern Waterfront, which includes Keppel, Sentosa, and Gardens by the Bay.

Since there are no plans to increase the number of residential units in Sentosa, the redevelopment is expected to yield positive effects on Sentosa Cove, as it will be minutes away from aspiring world-famous attractions.

Future of work

In a post-pandemic world where hybrid or remote work is becoming more prevalent, Sentosa Cove emerged as choice place of residence. It’s serene and idyllic environment, along with its luxurious amenities, make it attractive for those pursuing sophistication, leisure and a refined lifestyle even as they are working from home. Even though Sentosa Cove is pretty self-sufficient, enhanced last mile delivery options have further elevated convenience for residents in recent years.

Singapore’s reputation as a safe haven beckons High Net Worth Individuals (HNWIs)

Singapore’s reputation for safety, political stability, and economic resilience continues to attract foreign investors. The government has been relentlessly pursuing High Net Worth Individuals (HNWIs) and talents to Singapore through various schemes, enticing them to invest here, including in residential properties.

The Global Investor Programme allows HNWIs who generate economic spin-offs and create employment to attain Permanent Residency status. To do so, they can choose to invest at least S$10 million in a business or S$25 million in an approved fund.

Other long-term programmes for high-income skilled foreign talents include the Overseas Networks & Expertise Pass and the Tech.Pass.

Being recognised as a wealth hub in Asia, Singapore attracted some $2,619 billion in foreign direct investment and has close to 1,100 family offices established in Singapore as at 2022. Moreover, the KPMG Private Enterprise and family office consultancy Agreus estimated as at 2023, 59% of all family offices in Asia are located in Singapore.

But the government could potentially sweeten the deal for foreigners through Sentosa Cove.

Is it time to reduce ABSD for foreign buyers purchasing properties Sentosa Cove?

The initial vision for Sentosa Cove was conceived with the aim of positioning Singapore as a premier waterfront living destination for the affluent.

However, along the way, multiple rounds of cooling measures have taken a toll on the Sentosa Cove housing market. Sentosa home price growth has not kept pace with homes on the main island. In 2023, the CCR average home prices reached around $2,510 psf compared to the average of $1,992 psf at Sentosa Cove.

One potential solution is to reduce the ABSD payable by foreign buyers purchasing homes at Sentosa Cove from 60% to 20%. This would align with what a Singaporean would pay when buying a second property. By implementing this change, this may redirect more foreign buyer interest towards Sentosa Cove.

Sentosa Cove is on track to becoming a choice waterfront living enclave in the region

Singapore will continue to be a magnet for global investors due to its reputation for safety, political stability, and ease of doing business. This, in turn, will help support the Singapore property market over the long term.

Sentosa Cove offers a differentiated product and presents an opportunity for those aspiring to immerse themselves in the epitome of luxury waterfront living. One can revel in its unparalleled luxury and exclusivity by indulging in oceanfront villas, tranquil waterway bungalows, and an array of upscale condominiums at Sentosa Cove.

Beyond its stunning architecture and picturesque landscapes, Sentosa Cove is still priced below homes in the CCR, and that presents a value buy for investors. Going forward, with the anticipated rising home prices across the island, coupled with redevelopment in Sentosa and the Greater Southern Waterfront, home prices in Sentosa Cove could see further appreciation in the future.

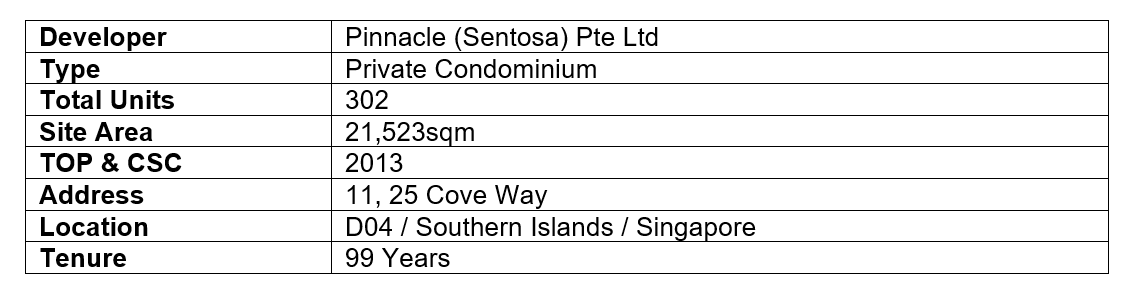

Have we piqued your interest in Sentosa Cove? Here are some exciting home options.

Cape Royale

DESCRIPTION

Cape Royale Sentosa Cove is the tallest residential condo. Situated just at the entrance of the marina leading into Sentosa Cove Singapore. Sentosa Cove condo residents will be enjoying the breathtaking views of the South China Sea and Tanjong Golf Course.

Cape Royale condo is developed by Pinnacle (Sentosa) Pte Ltd. This iconic tower will offer 302 luxurious residential units in Sentosa Cove. Residents will have easy access to an integrated marina, One°15 Marina Club and Resort World Sentosa. All other Sentosa Island entertainments are with minutes reach. On top of the Sentosa Island attractions, Cape Royale Singapore is easily accessible to and from the main island of Singapore. Travel time to Singapore Changi International Airport is within half an hour drive away.

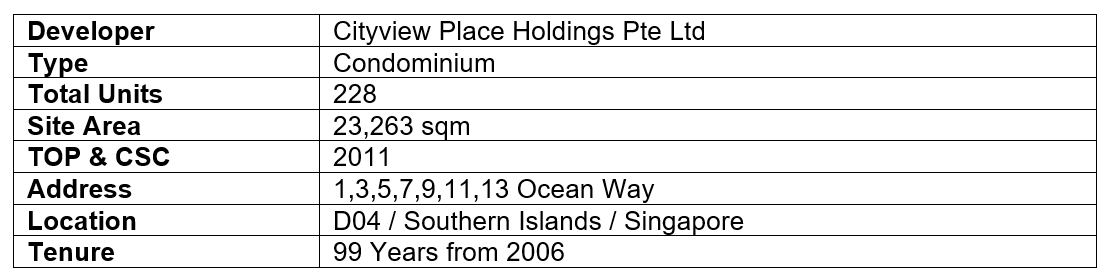

The Residences At W Singapore Sentosa Cove

The Residences is a luxury leasehold condominium project comprising 228 exclusive apartment suites situated amongst a wave of six-storey condominium blocks.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Budget 2024 announced four changes that will affect home owners and the Singapore residential market. Here is what you need to know.

1. Enhanced Annual Value Band for Owner-Occupier Residential Properties to offer Property Tax Relief in 2025

Owner-occupier residential property will pay lower property tax from 2025 with as Annual Value (AV) bands adjust higher. The earlier tax had meant to be a wealth tax. But with the AV rising due to higher rents, the majority of owner-occupier residential properties were impacted by a significant jump in their property tax. This move will be a relief for the majority of homeowners.

Table 1: Changes To Property Tax

|

Marginal PT rate

|

Portion of AV (S$) |

Portion of AV (S$) |

|

2024 |

From 1 Jan 2025 |

|

|

0% |

$0 – $8,000 |

$0 – $12,000 |

|

4% |

>$8,000 – $30,000 |

>$12,000 – $40,000 |

|

6% |

>$30,000 – $40,000 |

>$40,000 – $50,000 |

|

10% |

>$40,000 – $55,000 |

>$50,000 – $75,000 |

|

14% |

>$55,000 – $70,000 |

>$75,000 – $85,000 |

|

20% |

>$70,000 – $85,000 |

>$85,000 – $100,000 |

|

26% |

>$85,000 – $100,000 |

>$100,000 – $140,000 |

|

32% |

>$100,000 |

>$140,000 |

Source: MOF, ERA Research and Market Intelligence

For example, an OCR 3 bedroom with an AV of $40,000 can enjoy a tax saving of $360 in 2025. While a semi-detach with an AV of $85,000 can enjoy a tax savings of $2,460.

Table 2: Property tax relief for owner-occupier residential properties from 2025

|

Annual Value |

Property Tax |

Property tax decrease |

|

|

2024 |

2025 |

||

|

$12,000 |

$160 |

$0 |

$160 |

|

$20,000 |

$480 |

$320 |

$160 |

|

$30,000 |

$880 |

$720 |

$160 |

|

$40,000 |

$1,480 |

$1,120 |

$360 |

|

$55,000 |

$2,980 |

$2,220 |

$760 |

|

$70,000 |

$5,080 |

$3,720 |

$1,360 |

|

$85,000 |

$8,080 |

$5,620 |

$2,460 |

|

$100,000 |

$11,980 |

$8,620 |

$3,360 |

|

$140,000 |

$24,780 |

$19,020 |

$5,760 |

Source: ERA Research and Market Intelligence

In addition, retirees living in properties with high AV but face cash flow issues paying their property taxes can opt for a 24-month instalment plan with no interest over the regular 12-month. This will make monthly payments more affordable for them. They must be aged 65 and above, living in the property they own and have an assessable income of $34,000 or less.

2. Single Seniors concession on ABSD

Single Senior Singapore citizens aged 55 and above to get the additional buyer’s stamp duty (ABSD) refund to help them in “right sizing” their property. To qualify, these buyers will need to sell their only residential property within six months of purchasing a replacement lower-value private property.

The ABSD concession extended to single senior Singaporeans is timely, providing this group of Singaporeans another option to right size their properties, helping them to unlock some monies from their existing property that could support their retirement. The punitive 20% ABSD have previously deterred this group to look into the private property segment, restricting them to only HDB resale flats; but they will now have another housing alternative.

However, for those who are unable to foot the 20% ABSD first will still have to sell their existing property before buying. For a $1.2 million property, the ABSD is $240,000 and this is payable within 14 days of exercising the Option to Purchase the private property.

3. Lower ABSD clawback rate for developers of housing developments that sell >90% within 5 years

Housing developers will have more flexibility with the ABSD clawback if they sell at least 90% of their units. Developers will pay the full 25% or 35% (depending on when the site is purchased) as long as there are unsold units. ABSD remission clawback is subject to 5% interest per annum.

From 16 February 2024 onwards, the clawback rate will be reduced if they sell at least 90% of units in the development within the five-year timeline. This provides them with more flexibility, while ensuring that supply of new homes are released in a timely manner.

The recent GLS biddings drew more muted responses as developers are cautious amid the elevated interest rate environment and slower new home sales rates. By lowering the ABSD clawback based on the proportion of units sold, this will give developers some respite and confidence to bid for upcoming GLS sites, allowing them more time to sell their balance units. Some of the larger units due to their higher price quantum typically take longer to sell.

To put things into perspective, the 1% unsold units equates to 7 units in a 700-unit housing development. Under this revised ABSD remission clawback, a $1 billion site which have 1% unsold units can save up to $100 mil, which is pretty substantial.

Table 3: Revised ABSD remission clawback for residential projects

| Proportion of units sold |

Projects with residential land acquired between 6 Jul 2018 and 15 Dec 2021, subject to 30% ABSD with upfront 25% remission |

Projects with residential land acquired on or after 16 Dec 2021, subject to 40% ABSD with upfront 35% remission |

||

|

ABSD Remission clawback applicable before 16 Feb 2023 (%) |

ABSD Remission clawback applicable after 16 Feb 2023 (%) |

ABSD Remission clawback applicable before 16 Feb 2023 (%) |

ABSD Remission clawback applicable after 16 Feb 2023 (%) |

|

|

100% |

0% |

0% |

0% |

0% |

|

99% |

25% |

15% |

35% |

25% |

|

98% |

25% |

16% |

35% |

26% |

|

97% |

25% |

17% |

35% |

27% |

|

96% |

25% |

18% |

35% |

28% |

|

95% |

25% |

19% |

35% |

29% |

|

94% |

25% |

20% |

35% |

30% |

|

93% |

25% |

21% |

35% |

31% |

|

92% |

25% |

22% |

35% |

32% |

|

91% |

25% |

23% |

35% |

33% |

|

90% |

25% |

24% |

35% |

34% |

|

<90% |

25% |

25% |

35% |

35% |

Source: MOF, MND, ERA Research and Market Intelligence

Table 3: ABSD clawback for a $1 billion site purchased in January 2024

|

Before 16 Feb 2024 |

After 16 Feb 2024 |

|||

|

Proportion of units sold (%) |

ABSD remission clawback rate |

ABSD clawback amount |

ABSD remission clawback rate |

ABSD clawback amount |

|

88% |

35% |

$ 350 mil |

35% |

$350 mil |

|

90% |

34% |

$340 mil |

||

|

95% |

29% |

$290 mil |

||

|

99% |

25% |

$250 mil |

||

Source: ERA Research and Market Intelligence

4. Eligible families waiting for BTO can soon get voucher to rent flat in open market.

To help young couples who are ready to settle down, the Government will provide a voucher under the Parenthood Provisional Housing Scheme (PPHS) so that eligible families waiting for their Build-To-Order (BTO) units can rent a Housing Board flat on the open market. The voucher will be available for a year.

The PPHS provides interim rental housing to families with a monthly household income of $7,000 or below, and have an uncompleted flat from HDB’s sales exercises.

There are no details yet on the amount of the voucher and the mechanics of the scheme.

In summary

Overall, the budget changes are relatively minor and focus on fine-tuning existing policies rather than introducing any major overhauls. We believe, these adjustments are designed to enhance the effectiveness of current measures and address emerging issues.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The rental market showed signs of stabilising since 2Q 2023 with the slower growth of the rental index. Meanwhile the HDB rental market stayed resilient. Has the rental market tipped in favour of tenants?

Private Residential Rental

The all private residential property rental index prices grew 11.1% in the first nine months of 2023. Rental growth has been more gradual since 2Q 2023, with the rental index rising by 2.8% quarter-on-quarter (q-o-q) in 2Q 2023 and 0.8% q-o-q in 3Q 2023. The rental index surged 53.0% between 3Q 2020 and 1Q 2023 on the back of COVID-led disruptions, but the rate of growth has ease since the second half of 2023.

Chart 1: Rental Index of Private Residential Properties

Source: URA as at 20 Dec, ERA Research and Market Intelligence

Looking at non-landed median prices across the regions, all regions have seen rents easing since the beginning of 2023. But the Core Central Region reportedly saw median rents moderated in 3Q 2023. In light of the softer economic outlook, more tenants have observed to be prudent with their rental budgets choosing to downsize their apartments, or move further outskirt to capitalise on more affordable rents. This has supported rents in the Rest of Central Region and the Outside Central Region.

Chart 2: Non-landed median rent by market segment

Source: URA, ERA Research and Market Intelligence

The number of private residential rental contracts for 11m 2023 reached 76,686 contracts, contracting by 10.3% compared to 84,551 contracts inked in 11m 2022. This is largely attributed to the moderation of rental demand with the progressive easing of the construction backlog. For the whole of 2023, the private residential contracts could reach between 80,000 and 82,000.

Chart 3: Private residential rental contracts

Source: URA as at 20 Dec, ERA Research and Market Intelligence

More rental inventory expected with the slew of new home completions

Some 19,000 private residential units (excluding EC) completed in 2023, marking the highest annual supply completion since 2016. Another 10,000 units are schedule for completion in 2024. More rental inventory will come onstream with the slew of new home completions.

Chart 4: Private residential completions

Source: URA, ERA Research and Market Intelligence

Landlords to bear the brunt of higher property tax going forward

Annual values and property taxes are set to rise in 2024, and landlords will find themselves bearing the brunt of the increase amid a softer rental market. To put things into perspective, a property with a $45k annual value will see its property tax increase by 15.8% from $5,700 to $6,600. A property with a $60k annual value will see its property tax increase by 22.0% from $8,850 to $10,800.

Table 1: Non-owner-occupier residential tax rates (residential properties)

| Annual Value($) |

Effective 1 Jan 2023 |

Property Tax 2023 |

Effective 1 Jan 2024 |

Property Tax 2024 |

Property Tax Increase |

Percentage Increase |

| First 30,000 |

11% |

$3,300 |

12% |

$3,600 |

$300 |

9.1% |

| Next $15,000 |

16% |

$2,400 |

20% |

$3,000 |

$600 |

25.0% |

| First $45,000 |

– |

$5,700 |

– |

$6,600 |

$900 |

15.8% |

| Next $15,000 |

21% |

$3,150 |

28% |

$4,200 |

$1,050 |

33.3% |

| First $60,000 |

– |

$8,850 |

– |

$10,800 |

$1,950 |

22.0% |

| Above $60,000 |

27% |

36% |

Source: IRAS, ERA Research and Market Intelligence

Rental demand has gradually receded since the beginning of 2023 with the clearing of the construction backlog. The influx of new home completions since 2Q 2023 has helped ease the rental market with more inventory coming onstream. ERA anticipates private residential rental prices to ease as much as 5% and the number of rental contracts to reach between 75,000 – 80,000 in 2024.

HDB Rental Market expected to stay resilient in 2024

HDB median rental prices reported sustained growth over the first nine months of 2023. On average, the HDB median rental price for 3-room flat and 4-room flat across the various town rose 11.2% and 11.4% respectively in the first nine months of 2023. Meanwhile, 5-room and Executive flats reported steeper growth of 13.7% and 21.5% across various towns over the same period.

Table 2: 3Q 2023 HDB median rents by town and y-o-y growth

| 3Q 2023 | Y-o-y | |||||||||

|

Town |

3-Room |

4-Room |

5-Room |

Executive |

Town |

3-Room |

4-Room |

5-Room |

Executive |

|

|

Ang Mo Kio |

$2,700 |

$3,380 |

$3,700 |

* |

Ang Mo Kio |

17.4% |

16.6% |

17.5% |

||

|

Bedok |

$2,700 |

$3,280 |

$3,500 |

$4,000 |

Bedok |

17.4% |

17.1% |

16.7% |

||

|

Bishan |

$2,800 |

$3,600 |

$4,000 |

* |

Bishan |

7.7% |

12.5% |

12.7% |

||

|

Bukit Batok |

$2,600 |

$3,150 |

$3,700 |

* |

Bukit Batok |

18.2% |

18.9% |

15.6% |

||

|

Bukit Merah |

$3,000 |

$3,900 |

$4,400 |

– |

Bukit Merah |

15.4% |

11.4% |

15.8% |

||

|

Bukit Panjang |

$2,600 |

$3,000 |

$3,400 |

$3,450 |

Bukit Panjang |

-3.7% |

5.3% |

13.3% |

||

|

Bukit Timah |

* |

* |

* |

* |

Bukit Timah |

|||||

|

Central |

$3,080 |

$4,100 |

* |

– |

Central |

10.0% |

6.5% |

|||

|

Choa Chu Kang |

$2,300 |

$3,100 |

$3,300 |

$3,300 |

Choa Chu Kang |

-17.9% |

10.7% |

10.0% |

10.0% |

|

|

Clementi |

$2,900 |

$3,800 |

$4,000 |

* |

Clementi |

16.0% |

18.8% |

17.6% |

||

|

Geylang |

$2,700 |

$3,100 |

$3,850 |

* |

Geylang |

14.9% |

3.3% |

|||

|

Hougang |

$2,580 |

$3,150 |

$3,450 |

$3,000 |

Hougang |

12.2% |

14.5% |

27.8% |

11.1% |

|

|

Jurong East |

$2,680 |

$3,500 |

$3,700 |

* |

Jurong East |

7.2% |

20.7% |

19.4% |

||

|

Jurong West |

$2,700 |

$3,200 |

$3,500 |

$3,600 |

Jurong West |

22.7% |

10.3% |

15.5% |

38.5% |

|

|

Kallang/ Whampoa |

$2,700 |

$3,500 |

$3,400 |

* |

Kallang/ Whampoa |

10.2% |

12.9% |

-8.1% |

||

|

Marine Parade |

$3,000 |