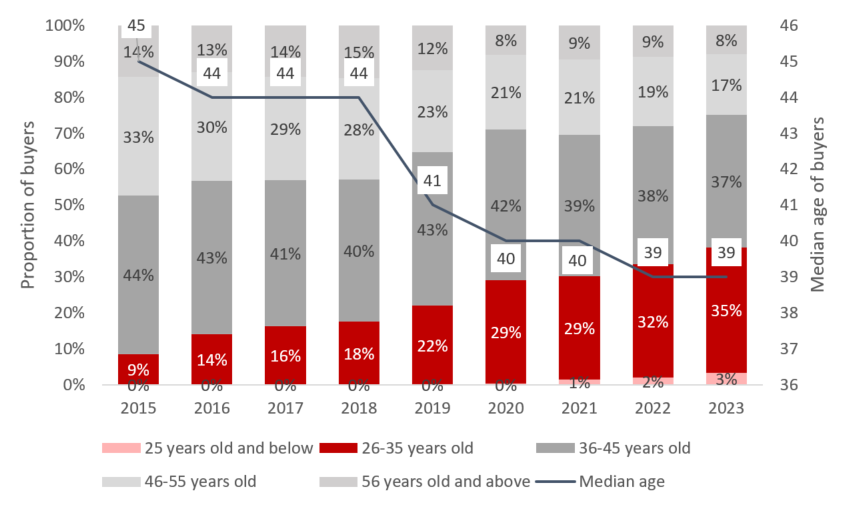

The market share of new private home buyers, aged 26 to 35 years old, more than tripled between 2015 to 2022.

Even in the face of recent headwinds, including higher interest rates, moderating economic activity, and the implementation of market cooling measures in April 2023, the demand for new private homes among Singaporeans has stayed steadfastly strong.

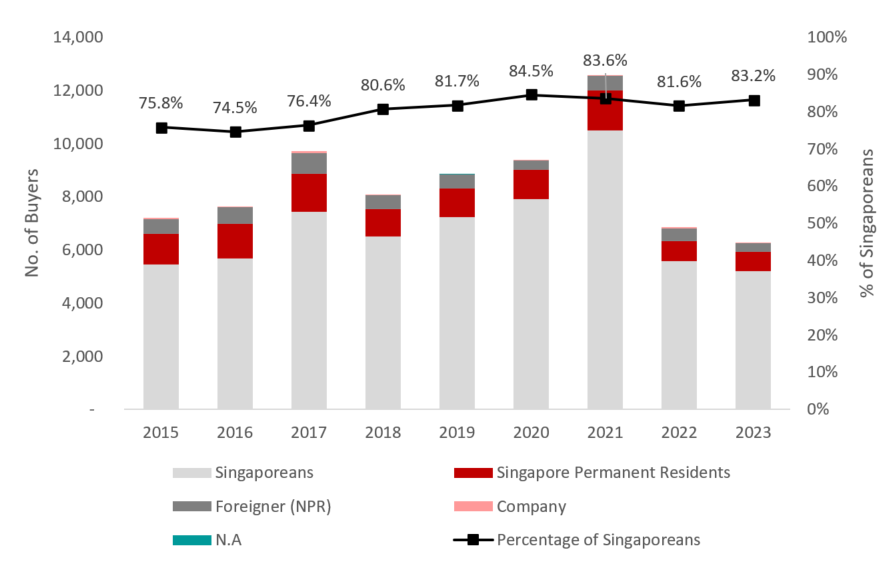

Singaporeans have consistently held sway in Singapore’s new private home market, capturing the lion’s share of yearly new home purchases. In 2015, Singaporeans accounted for approximately 75.8% of new private home sales; this percentage has risen steadily across the years, reaching a peak of 84.5% in 2020 and has remained at similar levels since.

Chart 1: New Private Home Buyers by Nationality and Residential Status (2015 to 2023)

Source: URA as of 18 Jan 2024, ERA Research and Market Intelligence

This upswing in Singapore buyers follows a steady growth in demand for new private residential homes, particularly amongst young Singaporeans, whom we define as Singaporeans aged between 26 to 35 years old.

Between 2015 to 2022, the cohort of local adults comprising the aforementioned age group of new private home buyers has more than tripled – a finding that tallies with mainstream media observations about the homeownership aspirations of Singaporean millennials and Gen-Zers.

The changing face of Singaporean new private home buyers

Based on proprietary industry data from ERA Singapore, covering a sample size of 37,000 Singaporean new home buyers, we have identified three prominent demographic trends pertaining to new private home buyers in Singapore.

1. A rising proportion of young Singaporeans are buying new private homes

Mirroring housing markets worldwide, older Singaporeans have traditionally dominated the domestic market for new private homes, but there are now compelling signs supporting a noticeable shift in this widely-held narrative.

Across the past nine years, the share of young Singaporean buyers of new private homes has climbed steadily. In 2015, this demographic group accounted for just 9% of new private home sales in the country; this figure has since surged by 26 percentage points to 35% in 2023.

The proportion of Singaporeans under 25 in the new private home sales market, though still small, also grew to 3% in 2023.

After the COVID-led demand surge seen in 2021, we saw the Singapore residential market transiting into a different realm largely characterised by rising home prices amid supply chain disruption and elevated interest rates. The Additional Buyer Stamp Duty implemented in April 2023 further dampened new home demand across the board in 2023. New private home sales reached some 13,027 units in 2021 but have fallen to a mere 6,421 units by 2023.

Looking at the numbers of Singaporeans buying new private homes, the number of buyers between the age group of 26 to 35 has seen a gentler decline in buyer numbers in comparison to other segments.

Between 2021 to 2023, the number of buyers aged 26 to 35 shrank by 59.5%, from 1,818 to 737. But for the age groups of 36 to 45, 46 to 55, as well as 56 and above, their respective declines were more noticeable at 69%, 72.9% and 71.8% respectively across the same period.

2. Singaporeans aged 36 to 45 still form the largest segment of new private homebuyers despite decline in numbers

Despite shrinking in number, Singaporean buyers belonging to the 36 to 45-year-old cohort have retained their dominance in the new private home market. In 2015, these Singaporeans accounted for 44% of new private residential property purchases; this was followed by Singaporeans between 46 to 55 years old, whose share of new private home transactions was 33% in the same year.

Fast forward to 2023, and the size of both buyer groups has dipped. Singaporeans belonging to the 36 to 45 age group now account for 37% of transactions, a 7-percentage point drop compared to eight years ago.

The shift is even more apparent for Singaporean buyers in the 46 to 55 age range, whose share of new private home transactions has fallen to 17% in 2023, marking a 16-percentage point decline.

3. The profile of new private homebuyers is skewing younger

In light of the latest changes in buyer demographics, the median age of Singaporean new private home buyers has distinctly exhibited a downward trend, possibly indicating that younger generations of locals will be playing a bigger role in Singapore’s new private residential market.

Chart 2: Proportion New Private Home Buyers by Age (2015 to 2023) and median age of buyers

Source: ERA Research and Market Intelligence

In 2015, the median age of new private home buyers was 45. Since then, it has traced downwards year on year over the last eight years, before reaching the current low of 39 years in 2023.

What is driving these shifts in new private homeownership?

1. Rising incomes are enabling young Singaporeans to achieve their private homeownership aspirations

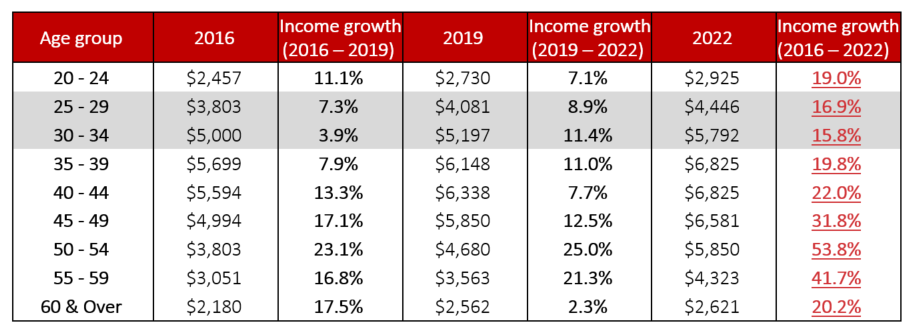

According to official figures by the Ministry of Manpower, the median income for full-time employed residents increased for all age groups from 2016 to 2022.

In 2022, the median gross monthly income for full-time employed residents between the ages of 25 and 29 reached $4,446 years old, while those between 30 and 34 earned $5,792. Compared to the corresponding figures in 2016, this represents a 16.9% increase (up from $3,803) and a 15.8% increase (up from $5,000) for local residents in the respective age groups.

Over the same period, full-time employed residents aged 35 – 54 also experienced some of the biggest increases in monthly income, ranging from 19.8% to 53.8%. This observation is a possible glimpse into the future earning potential of younger Singaporeans – and consequently more confident of their ability to invest in new private homes.

New private homes are more accessible for young Singaporeans with growing income. New private homes allow for the progressive payment scheme which support young Singaporeans who may not have the income to manage the full mortgage payment at the beginning.

Table 1: Median Gross Monthly Income from Work (Including Employer CPF) of Full-Time Employed Residents in S$

Source: MOM, ERA Research and Market Intelligence

In tandem with this trend, the macroeconomic review published by the Monetary Authority of Singapore in October 2023, indicated that nominal incomes for middle-income workers – half of whom are between 25 to 49 years old in 2021 – grew more rapidly vis-à-vis other income groups.

Equally so, the healthy overall employment rate in Singapore is a likely contributor to the growing number of young local private home buyers.

2. Elevated interest rates have impacted mortgage eligibility across the board, but older Singaporeans are affected more

Since 2H 2022, interest rates in Singapore have soared in tandem with hikes in US Federal Reserve rates – in particular, the 3-month compounded Singapore Overnight Rate Average has risen by 170 basis points since 3Q 2022.

The resulting squeeze has impacted the mortgage eligibility of all Singaporeans, though the effects are more pronounced for older borrowers than those belonging to younger age groups.

Older Singaporeans face a double whammy: In addition to shrinking mortgage approvals – which translate into steeper upfront payments and a larger initial capital outlay – they also have to contend with shorter loan tenures as well as higher interest rates that contribute to higher monthly mortgage repayments.

This confluence of factors has cause some older Singaporeans to put off their home upgrading plans indefinitely.

3. Buyers nearing the income ceiling for BTO flats may find more options in new private homes

Young Singaporean couples whose combined monthly household earnings surpasses the $14,000 income ceiling for Built-to-Order (BTO) flats, could gravitate towards purchasing an Executive Condominium (EC) or new private property over a resale HDB flat.

Case Study with Couple A:

With a combined gross monthly income of $15,000 exceeding the BTO income ceiling, Couple A is currently deciding between purchasing a resale HDB flat, an EC or a private condominium.

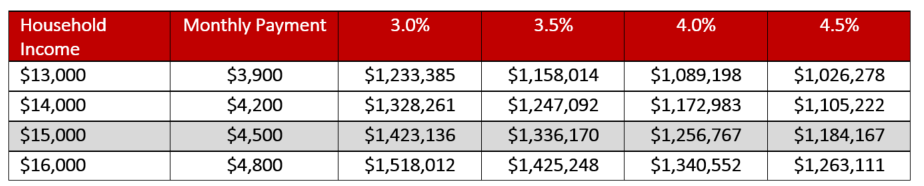

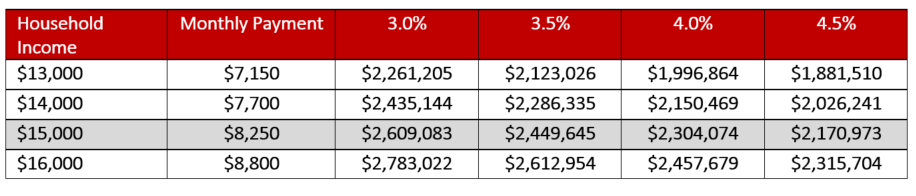

Table 2: Max purchase price for a resale HDB flat or EC by gross monthly household incomes and prevailing MSR

Source: ERA Research and Market Intelligence

Assuming a 75% Loan-to-Value (LTV) limit, 30-year loan tenure, and 4% medium-term benchmark interest rate, Couple A can afford an EC or a resale HDB flat priced up to $1.25 mil based on the prevailing Mortgage Servicing Ratio (MSR) of 30%.

Table 3: Max purchase price for a private residential unit by gross monthly household incomes and prevailing TDSR

Source: ERA Research and Market Intelligence

In comparison, with all loan assessment factors held constant and the current Total Debt Servicing Ratio (TDSR) of 55% applied, Couple A will be to afford a new private home valued near $2.3 mil.

Consequently, the larger loan quantum available for new private homes allows Couple A to explore a wider range of properties, thereby increasing their chances of finding a private residence which matches their needs and aspirations.

That said, the substantial down payment and stamp duties associated with purchasing a new private home may pose a hurdle for younger Singapore adults.

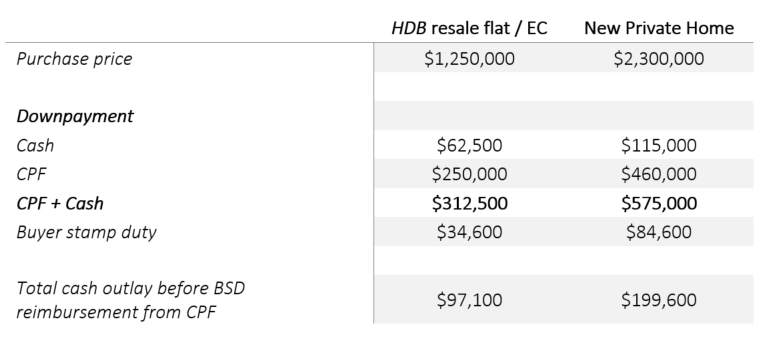

Supposing that Couple A has chosen to purchase a $1.25 mil resale HDB flat, they will need to provide a down payment amounting to $312,500, of which $62,500 has to be paid in cash for a bank loan. After accounting for the Buyer Stamp Duty (BSD) based on prevailing rates, Couple A’s initial cash outlay will amount to $97,100 but they can obtain reimbursement for the BSD from their CPF accounts.

In comparison, if Couple A were to opt for a new private home valued at $2.3 mil, they would instead be required to fork out $575,000 for their downpayment. This translates into a minimum cash amount of $115,000, and with the BSD included, Couple A’s upfront cost for a new private home comes up to $199,600.

Table 4: Comparison of cash and CPF outlay for the purchase of a HDB resale flat versus a new private home

Source: ERA Research and Market Intelligence

As a result, this initial upfront investment may put new launches out of reach for young Singaporeans aged 26 to 30 years old, but not so much for their 31 to 35-year-old peers, who could have adequate downpayment for upgrading upon selling their first home.

Anecdotal observations by our salespersons suggest a small proportion of young Singaporean homebuyers received some form of financial help from their parents for their first home purchase. But in most cases, young Singaporeans were able to pay the equity portion of the purchase price themselves.

1. Cap on HDB resale price growth over the longer term could prompt more Singaporeans to consider private homes as an investment option

The reclassification of HDB flats announced in August 2023 reaffirms the Singapore Government’s stance to ensure public housing affordability in the long run.

These include the introduction of the Plus and Prime housing models – both of which come with tighter resale and rental restrictions such as a 10-year Minimum Occupation Period, in addition to a subsidy clawback when they are sold on the resale market for the first time. Furthermore, prime flats will see resale buyers subject to income ceiling cap.

All of these conditions could have a moderating effect on resale price growth in the future. Consequently, aspiring investors may shifting their attention towards private homes which could potentially yield better returns compared to HDB flats.

2. More young Singaporeans accumulate initial downpayment for property purchase through savings and investing at a younger age

A survey published by global investment firm Franklin Templeton targeting respondents aged 18 to 35 years old, revealed that 80% of young Singaporeans are current investors. Additionally, half of the 502 respondents also agreed that they should start investing at a younger age (50%), and that doing so is key to good financial planning (51%).

By doing so, this allow younger Singaporeans to accumulate the initial downpayment and purchase their first property purchase since real estate is still widely regarded as a stable investment asset among Singaporeans. Private home offers opportunities for capital appreciation and passive incomes, which closely resonates with the young Singaporeans’ views on investing and building financial security at an early age.

Is this trend of young Singaporean private homebuyers here to stay?

Though it is a certainty that there is a growing number of Singaporeans entering the private housing market at a younger age, it remains to be seen if this will be a persistent trend in Singapore’s real estate landscape over the long term.

On one hand, a possible slowdown in economic activity and moderating income growth could dampen the appetites and purchasing power of young Singaporeans. This could lead to a reversal in the current trend, as aspiring homeowners re-evaluate their financial priorities and adjust their budgets accordingly.

Beyond just looking at macroeconomic conditions, several other factors may influence young Singaporeans to buy private homes.

The combination of premium facilities as well as the higher potential investment upside of private properties may hold greater appeal for young Singaporeans. Likewise, young aspiring investors may be drawn to private homes, owing to the moderation on HDB resale price growth over the longer term with more stringent resale restrictions for HDB flats in the future.

The appeal of private homes remains alluring and there are many compelling factors for young Singaporeans to invest into new private homes. And with some 32 upcoming new private home launches in 2024, prospective homebuyers will be spoilt for choice and have ample options to choose from. With that, we can expect to see a growing number of young Singaporeans making their foray into the dynamic realm of the new private home segment going forward.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The landed shophouse segment had some banner years but saw notable moderation in demand in 2023.

As at 20 December 2023, a total of 118 landed shophouses were transacted, amounting to a transaction value of $1.07 billion. Transaction volume and value have moderated by 35.9% and 32.6% year-on-year (y-o-y) respectively compared to 2022. At the peak in 2021, some 245 landed shophouses exchanged hands, totalling $1.84 billion.

Shophouse transactions have moderated in the second half of 2023 following rising prices and softer yields. Furthermore, the spat of high-profile money laundering cases uncovered in August led to heightened anti-money laundering checks on foreign buyers. The total landed shophouse market saw only 41 landed shophouse caveats, amounting to $349 million, lodged in 2H 2023.

Chart 1: Transaction volume and transaction value of landed shophouses

Source: URA as at 20 Dec, ERA Research and Market Intelligence

Steady rise in proportion of shophouses transacted in the $5mill and above price quantum

Some 45.5% of landed shophouses transacted between $5 mil and $10 mil, and another 24.6% of the landed shophouse transactions were more than $10mil in 12023.

The limited supply of landed shophouses has kept demand resilient over the years, supporting price growth. Based on caveats lodged, the average price of freehold landed shophouse has risen 57.8% since 2019. Freehold (FH) and 999-year leasehold shophouses accounted for 94% of landed shophouse transactions in 2023.

Chart 2: Price quantum of landed shophouse in the last ten years

Source: URA as at 20 Dec, ERA Research and Market Intelligence

Chart 3: Landed shophouse average price PSF

Source: URA as at 20 Dec, ERA Research and Market Intelligence

Singapore shophouse: An asset class that captivates foreign investors

Approximately 6,500 units of these landed shophouses fall under the conservation status, and owners of these properties must comply with strict guidelines around maintaining their façade and structure. Due to their scarcity, these shophouses are highly sought after by institutional investors and family offices.

Furthermore, the strong Singapore dollar, relatively low tax rates, and political stability make Singapore an attractive market for investors. For these reasons, the landed shophouses are coveted by institutional investors and family offices for capital appreciation and wealth preservation.

The most notable deal in 2023 would be the divestment of the remaining stake of the founder of 8M Real Estate to his partner, Crane Capital. Crane Capital is a Hong Kong-based real estate investment company with an international investor base. 8M Real Estate’s portfolio consists of shophouses in Singapore and is valued at $1.3 billion.

Popularity of Central Region shophouses

Freehold shophouses in Districts 1, 7 and 8, continue to see evergreen demand from investors largely due to its resilient rental demand.

These districts are popular for their eateries and bars that can command higher rents. Meanwhile, Districts 12, 15 and 19 tie for the fifth place, with seven transactions for each of the districts. Conservation shophouses are also popular among budding retailers drawn by their unique and eclectic charm.

Chart 4: Top five districts by transactions volume in 2023

Source: URA as at 20 Dec, ERA Research and Market Intelligence

Table 1: Top five landed shophouse transactions in 2023

| Development | Address |

District |

Transacted Price ($) |

Land Area (sqft) |

Unit Price PSF ($) |

Transaction Date |

| N.A. | 322,324,330 ETC SERANGOON ROAD |

08 |

62,500,000 |

9,042 |

$6,912 |

19 Jan 2023 |

| DESKER ROAD CONSERVATION AREA | 203,205,207 JALAN BESAR |

08 |

38,500,000 |

6,378 |

$6,037 |

27 Sep 2023 |

| TELOK AYER CONSERVATION AREA | 5, 5A, 5B ANN SIANG ROAD |

01 |

32,000,000 |

1,446 |

$22,136 |

14 Jul 2023 |

| BOAT QUAY CONSERVATION AREA | 37 BOAT QUAY |

01 |

30,000,000 |

1,426 |

$21,034 |

19 May 2023 |

| N.A. | 433,435 GEYLANG ROAD |

14 |

30,000,000 |

4,518 |

$6,641 |

27 Jun 2023 |

Source: URA as at 11 Dec, ERA Research and Market Intelligence

Tighter land use regulation for landed shophouse since July 2023

The Ministry of Law and Singapore Land Authority removed ‘Commercial & Residential’ zoning in July 2023. Going forward, foreigners and companies with foreign directors will require approval under the Residential Property Act to purchase landed shophouses. This change will not impact demand for shophouses zoned under ‘Commercial’.

Nonetheless, this amendment is expected moderate some foreign investors from diversifying into the shophouse segment from the residential market. Since April 2023, the Additional Buyers’ Stamp Duty (ABSD) for foreign buyers looking to buy residential properties doubled to 60%. This drove foreign buyer demand to the shophouse segment which is not subject to ABSD.

Shophouse demand to hold firm 2024

Shophouse demand is expected to hold firm despite rising prices and softer yields. Sustained interest from investors and strong holding power of shophouse owners will continue to support price growth, albeit at a moderated pace in 2024. The removal of ‘Commercial & residential’ zone will redirect foreign investors towards shophouses under the ‘Commercial’ zone instead.

The total landed shophouse transaction volume is projected to reach approximately $1.1 billion in 2023, and ERA projects the total transaction value to range between $1 billion – $1.2 billion in 2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The Housing & Development Board (HDB) resale market has shown signs of stabilising even with price trending higher in 2023.

In the first nine months of 2023, the HDB resale price rose 3.8% in the first nine months of 2023 and peaked at 178.5 in 3Q 2023.

Transaction volume stayed fairly stable as of 26 December 2023, recording 24,650 resale transactions (3-room and larger) in 2023. This marked a 6% year-on-year (y-o-y) decline compared to 2022, where 26,254 resale transactions were lodged.

Chart 1: HDB Resale Price Index

Source: HDB, ERA Research and Market Intelligence

Chart 2: HDB Resale Transactions (3-room and larger flats)

![]() Source: HDB as at 26 Dec 2023, ERA Research and Market Intelligence

Source: HDB as at 26 Dec 2023, ERA Research and Market Intelligence

Diminishing supply of MOP flats

The number of HDB flats that met the Minimum Occupation Period (MOP) has more than halved in 2023 compared to 2022. Between 2019 and 2022, the number of MOP units averaged 23,000 units per year, which bolstered demand in the residential market. Going forward, the supply of MOP units is set to diminish further potentially leading to a moderate supply of resale flats in the market.

Chart 3: HDB flats that met Minimum Occupation Period

Source: data.gov.sg, ERA Research and Market Intelligence

Million-dollar Flats more commonplace

HDB flats surpassing the million-dollar mark are becoming commonplace. As at 26 December, there have been 464 million-dollar flat transactions in 2023, an increase of 26% compared to 369 in 2022.

Majority of these million-dollar flat transactions are within mature estates such as Bukit Merah (61 units), Toa Payoh (57 units) and Kallang/Whampoa (53 units). Likewise, non-mature estates have started seeing more million-dollar flat transactions. Most notably, Woodlands saw 14 million-dollar flat transactions in 2023. Many of these million-dollar flats possess similar qualities that buyers value, such as a longer remaining lease, larger floor area and are located near transport nodes or amenities.

Chart 4: Million-dollar Flat Transacted by Flat Types

Source: data.gov.sg as at 26 Dec 2023, ERA Research and Market Intelligence

New classification of HDB flats to ensure sustainable price growth in the long term

In August 2023, the government announced the new classification of HDB flats that will take effect from 2H 2024. Instead of mature and non-mature estates, new BTO flats will be re-classified as Prime, Plus and Standard flats to better reflect locational attributes and demand. Prime and Plus flats will come with more subsidies but their potential upside will be capped as they are subjected to more stringent resale conditions. This includes a 10-year Minimum Occupation Period (MOP), a resale levy imposed and an income ceiling on resale buyers.

Build-to-Order launches drew some potential buyers away from resale market

HDB has collectively launched some 23,000 Build-To-Order (BTO) units in 2023 over four sales launches in 2023 to keep up with the demands of buyers. Another 4,090 BTO units will be launched in February 2024. Kallang Whampoa, Serangoon (Serangoon North Vista), and Queenstown (Ulu Pandan Glades) emerged as some of the popular BTO projects in 2023.

Change in BTO ruling

HDB announced the change in BTO ruling that will grant greater priority to First-Timer families. Apart from additional ballot chances, there will also be a higher allocation of BTOs and Sale of Balance Flat (SBF) for First-Timer families.

But in the event of non-selection of flat, HDB will cancel any existing applications by the same applicant for subsequent BTO/ SBF exercise. First-timer families that do not select a flat when given the chance will be considered second-timers for the next one year. Prior to this, some BTO applicants may have applied for multiple BTO/SBF exercises to increase their chances of securing their ideal home.

The recent changes in BTO ruling have resulted in a decline in the median application rate of BTO in the October and December sales launches. The rate for first timer families fell from 2.3 in May 2023 to 0.9 in October 2023’s sale launch. Similarly, the rate for second timer families fell from 30.4 in May 2023 to 8.7 in October 2023’s launch. With the heavier penalties for non-selection of flats, prospective buyers may become more selective around which sales launches to apply for, or it may redirect some buyers towards the resale market.

Chart 5: Overall median application rates BTO launches (3-room and above)

Source: HDB, ERA Research and Market Intelligence

HDB resale market set to see more muted price growth despite demand holding firm

The HDB market will see a moderate pace of price growth in 2024. This is in anticipation of a moderate supply of resale units being put up for sale with the diminishing supply of MOP units. Additionally, the elevated interest rate situation and higher cost of replacement homes may have delayed some HDB owners’ upgrading plans.

Nonetheless, demand for HDB flats is expected to hold firm, particularly those located in proximity to amenities and transport nodes. Existing resale flats, which are not affected by the more stringent resale conditions set for the upcoming Prime and Plus flats, will also be popular among buyers.

For the whole of 2023, ERA expects the total resale transaction volume to reach between 25,000 and 26,000 units, marginally lower than the 26,254 resale transactions in 2022.

Supported by firm resale demand, ERA projects the total resale transaction volume to reach between 26,000 and 27,000 units by end-2024, with resale prices rising by a more muted 3% to 5% range by end-2024.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Rising cost and the elevated interest rates have moderated residential property demand across the board in 2023. Residential demand tapered further with the Additional Buyer Stamp Duty (ABSD) hike in April that curtailed demand from investors and foreigner buyers. The roundup of money laundering cases in August involving several high-value residential property transactions, has further led to the heightening of anti-money laundering checks. What’s next for the Singapore residential market?

But recent new sales performance seems to paint a different picture. J’den and Watten House, launched in November, have reported exceptional sales amid achieving benchmark prices. The residential market looks to have turned the corner with returning buyers’ confidence.

Projected economic expansion, low unemployment rates and healthy household balance sheet to support homebuying activities in 2024

Despite the global slowdown, Singapore has emerged as the bright spot in Asia Pacific. Its economic growth is forecasted to expand by 2.3% in 2023. The labour force is largely stable with overall unemployment rate projected to stay low, even as retrenchment increases. Both headline and core inflation could begin abating and are projected to average 3.0%-4.0% and 2.5%–3.5% respectively in 2024. For now, the Singapore household balance sheet remains healthy. All of these factors will help support homebuying activities.

Analysts are hopeful that the Federal Reserve of United States could cut interest rate by up to 75 basis point in 2024 in the second half of 2024. This could further boost the residential market and bolster transaction volume in 2024.

Residential home prices

The All-residential property price index reported a modest increase in 2023, registering a 3.9% growth in 3Q 2023 since the beginning of the year. CCR non-landed home prices, the laggard among the regions, fell by 2.0% over the first nine months of 2023. By contrast, RCR and OCR saw non-landed home prices rise 4.0% and 8.8% in the first nine months of 2023, largely attributed to higher new home prices in the areas.

Landed home prices have held steady, rising only 3.9% over the last nine months of 2023. This is in contrast to the last two years where the COVID-led boom sent landed prices soaring by 13.3% and 9.6% y-o-y in 2021 and 2022 respectively.

The all residential property price index is forecasted to grow between 4%-5% y-o-y in 2023, and another 5%-6% y-o-y in 2024. Meanwhile, landed home prices are anticipated to stay relatively stable and could see a potential growth of up to 2% by end 2024.

Chart 1: Singapore residential price index

Source: URA, ERA Research and Market Intelligence

Non-landed new homes

According to caveats as at 15 Dec 2023, the islandwide average new home price in 4Q 2023 reached $2,550 psf (per square feet), registering 8.9% growth y-o-y. After a dearth of new home launches since August, November new home launches such as J’den and Watten House, have reported exceptional sales performance amid achieving benchmark prices. J’den sold at a median price of $2,475 per square feet (psf) while Watten House reached a median price of $3,198 psf.

Despite an increase in new home launches this year, sales volume has moderated. In 2023, the new home market welcomed 22 new launches and one Executive Condominium (EC) launch. An estimated of 7,600 new homes (excluding EC) is launched in 2023, which is 52% higher than in 2022 (4,987 units).

The top five best-selling projects by units in 2023 are as follow: The Reserve Residences, Grand Dunman, Lentor Hills Residences, Tembusu Grand and J’den.

ERA projects total new home sale could reach between 6,500 and 7,000 in 2023, just a shade lower than 2022 where 7,099 new homes were sold.

Chart 2: New sale transactions and average price

Source: URA as at 15 Dec, ERA Research and Market Intelligence

Table 1: Top five Best-selling projects (excluding EC) in 2023

|

Project name |

Total units |

Tenure | Market Segment | Total units sold in 2023 | Average price

($psf) |

Percentage Sold |

|

THE RESERVE RESIDENCES |

732 |

99 Years | RCR | 676 | 2,470 |

92% |

|

GRAND DUNMAN |

1,008 |

99 Years | RCR | 622 | 2,522 |

62% |

|

LENTOR HILLS RESIDENCES |

598 |

99 Years | OCR | 436 | 2,084 |

73% |

|

TEMBUSU GRAND |

638 |

99 Years | RCR | 376 | 2,463 |

59% |

|

J’DEN |

368 |

99 Years | OCR | 329 | 2,457 |

89% |

Source: ERApro, URA as at 15 Dec, ERA Research and Market Intelligence

Buyer profile for new homes

The ABSD hike in April 2023, which included the doubling of ABSD for foreign buyers, has curtailed demand from foreign buyers across the board.

Among the market segments, CCR was the most impacted. Prior to the pandemic, foreign buyers accounted for close to one quarter of the buyers for homes in CCR, but this proportion has trended between 12% and 14% since 2020. RCR and OCR have seen similar declines, even as they reported a marginal decline in the proportion of foreign buyers.

Chart 3: Buyers profile by residential status (new homes)

Source: URA as at 15 Dec, ERA Research and Market Intelligence

Government Land Sales Programme

A total of eight residential and two EC sites were awarded in 2023. Some Government Land Sale sites have attracted up to six bids this year, and more developers have partnered up and put in joint bids. Both of the EC sites received nine bids.

Developers have been eager to replenish their land bank in 2023 as the unsold residential stock fell to only 17,576 (including ECs) units in 3Q 2023. Land costs have inflated and this paves way for higher new home prices in the near term. For instance, the Toa Payoh Lor 1 site closed in Nov, achieved a bid of $968 million, which worked out to a land rate of $1,360 per square feet per plot ratio.

New home outlook

In 2024, there could be as many as 32 new home launches and one EC launch scheduled in the pipeline. This could contribute to a total of more than 11,000 new homes.

The 2023 land sale performance suggests prices of new homes in 2024 will continue to grow at a more measured pace. ERA forecasts prices of new homes to grow between 3%-4% by end-2024 while demand for new homes in 2024 will remain largely similar to 2023, falling in the range of 7,000 to 8,000 units.

Table 2: Project launches in 2024

| No. | Private Residential Projects |

Region |

Location |

District |

Tenure |

Estimated number of units |

|

1 |

Marina View Residences |

CCR |

Marina View |

1 |

99 LH |

683 |

|

2 |

TBC (Marina Gardens Lane GLS) |

CCR |

Marina Lane |

1 |

99 LH |

790 |

|

3 |

Newport Residences |

CCR |

Anson Road |

2 |

FH |

246 |

|

4 |

Former Peace Centre |

CCR |

Sophia Road |

9 |

99 LH |

240 |

|

5 |

21 Anderson |

CCR |

Anderson Road |

10 |

FH |

18 |

|

6 |

32 Gilstead Road |

CCR |

Gilstead Road |

11 |

FH |

14 |

|

7 |

Former Kew Lodge |

CCR |

Kheam Hock Road |

11 |

FH |

TBC |

|

8 |

Former Central Mall / Central Square |

RCR |

Havelock Road |

1 |

99 LH |

366 |

|

9 |

Keppel Bay Plot 6 |

RCR |

Keppel Island |

4 |

99 LH |

86 |

|

10 |

Former Golden Mile Complex |

RCR |

Beach Road |

7 |

99 LH |

TBC |

|

11 |

The Arcady at Boon Keng |

RCR |

St Barbabas Lane |

12 |

FH |

172 |

|

12 |

TBC (Lorong 1 Toa Payoh GLS) |

RCR |

Lorong 1 Toa Payoh |

12 |

99 LH |

800 |

|

13 |

Ardon Residence |

RCR |

Haig Road |

15 |

FH |

35 |

|

14 |

Former Meyer Park |

RCR |

Meyer Road |

15 |

FH |

230 |

|

15 |

TBC (Jalan Tembusu GLS) |

RCR |

Jalan Tembusu |

15 |

99 LH |

840 |

|

16 |

The Hill @ One-North |

RCR |

Slim Barracks Rise |

5 |

99 LH |

142 |

|

17 |

The Hillshore |

RCR |

Pasir Panjang Road |

5 |

FH |

59 |

|

18 |

TBC (Bukit Timah Link GLS) |

RCR |

Bukit Timah Link |

21 |

99 LH |

160 |

|

19 |

TBC (Pine Grove GLS) |

RCR |

Pine Grove |

21 |

99 LH |

565 |

|

20 |

Former La Ville |

RCR |

Tanjong Rhu Road |

15 |

FH |

107 |

|

21 |

Former Bagnall Court |

OCR |

Upper East Coast Road |

16 |

FH |

113 |

|

22 |

Kassia |

OCR |

Flora Drive |

17 |

FH |

276 |

|

23 |

TBC (Tampines Avenue 11 GLS) |

OCR |

Tampines Avenue 11 |

18 |

99 LH |

1,190 |

|

24 |

Former Chuan Park |

OCR |

Lorong Chuan |

19 |

99 LH |

900 |

|

25 |

TBC (Champions Way GLS) |

OCR |

Champions Way |

25 |

99 LH |

350 |

|

26 |

Lentor Mansion |

OCR |

Lentor Gardens |

26 |

99 LH |

533 |

|

27 |

Lentoria |

OCR |

Lentor Hills Road |

26 |

99 LH |

267 |

|

28 |

TBC (Lentor Central GLS) |

OCR |

Lentor Central |

26 |

99 LH |

475 |

|

29 |

TBC (Clementi Avenue 1 GLS) |

OCR |

Clementi Avenue 1 |

5 |

99 LH |

501 |

|

30 |

Sora |

OCR |

Yuan Ching Road |

22 |

99 LH |

440 |

|

31 |

Hillhaven |

OCR |

Hillview Rise |

23 |

99 LH |

341 |

|

No. |

Executive Condominium Project |

Region |

Location |

District |

Tenure |

Estimated number of units |

|

1 |

Lumina Grand |

OCR |

Bukit Batok West Avenue 5 |

23 |

99 LH |

496 |

Source: ERA Research and Market Intelligence

Non-landed Resale and Sub sale market

Based on caveats lodged as at 15 Dec 2023, the islandwide average non-landed resale prices grew 5.7% in 2023 while the average non-landed sub sale prices grew 1.5% y-o-y.

Some 9,455 resale units were sold, the lowest transaction volume since 2020, and another 1,095 sub sale units were sold in 2023. Compared to 2022, resale transactions have moderated by 22.0% y-o-y. On the back of more new homes approaching completion, sub sale transactions have rose substantially by 56.7% y-o-y on the back of more new homes approaching completion.

The price gap between new home and resale home have prompted some buyers to turn towards the sub sale and resale market instead. RCR and OCR saw more newly completed homes transacted in recent months and this trend is expected to persist into 2024. Newly completed homes have taken centre stage as they are increasingly popular with buyers, given their brand-new condition and readiness for immediate occupancy.

Chart 4: Resale and sub sale transactions and average price

Source: URA as of 1 Dec, ERA Research and Market Intelligence

Source: URA as of 1 Dec, ERA Research and Market Intelligence

Upcoming home completions

For the whole of 2023, some 19,000 private residential units (excluding EC) are expected to complete, marking the highest annual supply completion since 2016. Another 10,000 units are schedule to be completed in 2024.

Chart 5: Private residential completions

Source: URA as of 1 Dec, ERA Research and Market Intelligence

Resale and Sub sale Outlook

The surge in new home completions could regulate the pace of resale price growth and drive transaction volume in 2024. For the whole of 2023, ERA forecasts the average non-landed resale and sub sale price could increase by 5% y-o-y, and by another 6% y-o-y in 2024. The total non-landed resale and sub sale are estimated to reach between 11,000 and 11,500 units in 2023, and between 12,000 and 13,000 units in 2024.

Landed property

The landed property segment reported subdued sales in 2023, primarily on the back of higher home prices and a lack of inventory. Landed home owners, who have stronger holding power and are facing higher costs of replacement homes, have been inclined to set higher prices and showed little urgency to sell. The demand, on the other hand, has remained fairly stable. In light of this situation, more landed deals have fallen through as buyers and sellers reached an impasse on home prices.

Landed home prices have held steady, rising only 3.9% over the last nine months of 2023. This is in contrast to the last two years where the COVID-led boom sent landed prices soaring by 13.3% and 9.6% y-o-y in 2021 and 2022 respectively.

The total volume of landed property transactions has declined to 1,198 units, with the total transaction value reaching $6.9 billion. Compared to a year ago, both the transaction volume and transaction value have declined by 28.8% and 27.4% respectively. For the whole of 2023, the total volume of landed property transactions could reach 1,200 – 1,300 units, with the total transaction value expected to surpass $7 billion.

Looking ahead to 2024, the landed property segment is projected to see muted activities largely due to rising costs. ERA foresees total landed transaction volume could moderate to between 1,100 and 1,200 units, with total transaction value reaching between $6.0 – $6.5 billion. Landed home prices are anticipated to stay relatively stable and could see a potential growth of up to 2% by end 2024.

Chart 6: Landed property transaction volume and transaction value

Source: URA as at 15 Dec, ERA Research and Market Intelligence

Conclusion

Looking ahead to 2024, the new home segment could see as many as 32 new home launches and one EC launch scheduled in the pipeline. ERA forecasts prices of new homes could grow between 3%-6% by end-2024 largely attributed to higher land prices. Demand for new homes in 2024 could moderate to the range of 7,000 to 8,000 units.

More new home completions in 2024 could regulate the pace of non-landed resale price growth and drive transaction volume in 2024. ERA projects non-landed resale prices could increase by up to 6% y-o-y in 2024, with the total resale and sub-sale transactions ranging between 12,000 and 13,000 units in 2024.

The landed property segment is projected to see muted activities and stable price growth in 2023. ERA foresees total landed transaction volume could moderate to between 1,100 and 1,200 units, with total transaction value reaching between $6.0 – $6.5 billion. Landed home prices are anticipated to stay relatively stable and could see a potential growth of up to 2% by end 2024.

In conclusion, the private residential market appears to have turned a corner. Macroeconomic indicators are showing signs of cautious optimism in 2024, and there is quiet confidence that the residential market will recover in 2024. The second half of 2024 is projected to bring about more positive economic developments that could propel the Singapore private residential market further.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.