Shophouse Demand Plummeted to a 26-year Low: Will it Revive in 2025 Despite Geopolitical Uncertainties?

- By Egan Mah Jixiang

- 6 mins read

- Commercial

- 23 Dec 2024

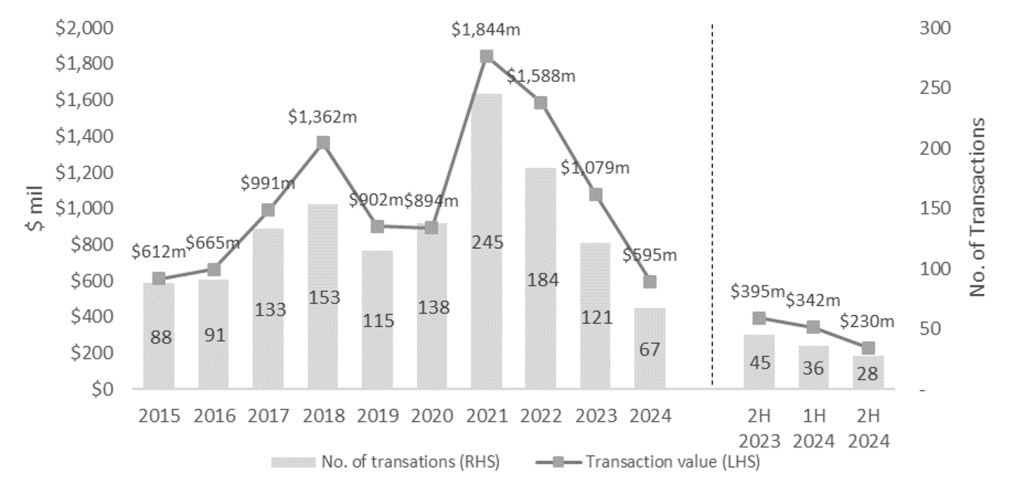

Based on URA’s lodged caveats, landed shophouse transactions fell to 28 deals worth $229.3 million in 2H 2024, down from 39 transactions totalling $365.3 million in 1H 2024. For the whole year, 67 landed shophouses were sold for a total of $594.5 million, marking the lowest number of transactions since 1998, when just 48 shophouses changed hands for $11.3 million.

The landed shophouse market remained in the doldrums after a high-profile money laundering case in 2023 dampened the appetite for shophouses.

Additionally, the high interest rate environment previously coupled with rising price quantum, had resulted in unattractive yields for investors. Even though the recent interest rate cuts might spark some optimism, the increasingly uncertain geopolitical landscape will likely leave investors cautious, with many preferring to stay on the sidelines for now.

Moreover, demand has also eased after the initial euphoria caused by the doubling of Additional Buyers’ Stamp Duty rate for foreign buyers purchasing residential properties. Some of these buyers had turned to the commercial shophouse market then.

Shophouses against Singapore’s CBD backdrop

However, this may not be a full view of the market as there could be deals transacted that may have flown under the radar. This could be due to several reasons, such as the caveats not being lodged, or the deal may have been purchased using Special Purpose Vehicles. Consequently, the total transaction value stands at $595 million, dwarfing the $1.1 billion recorded during the same period last year.

Against the market’s peak in 2021, which witnessed approximately 245 landed shophouses with a cumulative worth of $1.8 billion being sold in a year, the landed shophouse market has seemed to have bottomed out.

In summary, ERA remains cautiously optimistic of Singapore’s property market in 2025. Underpinned by firm macroeconomic fundamentals, Singapore will continue to deepen its status as one of Asia’s leading wealth management hub, thus drawing family offices, high-net-worth individuals and multinational companies to establish a firm foothold in the city.

For such investors, landed shophouses in Singapore are still deemed valuable and coveted assets.

Barring any unforeseen circumstances and assuming interest rates continue to moderate, the 2025 property market could outperform 2024, signalling a potential recovery on the horizon.

Taken together, the factors mentioned above are expected to boost buyer confidence, driving demand for real estate. Moreover, future price increases are more likely be driven by genuine buying interest, rather than speculative or foreign demand.

2024 Property Investments Underpinned by Firm Economic Fundamentals

Singapore’s economy gained momentum in 3Q 2024, recording a 5.4% year-on-year (y-o-y) expansion compared to a 3.0% growth in 2Q 2024[1].

The growth was primarily driven by robust performances in the manufacturing, wholesale trade, and finance & insurance sectors. With a continued recovery in global electronics demand and stronger-than-expected economic activity, MTI revised its full-year GDP growth forecast to approximately 3.5%, up from the earlier range of 2.0% to 3.0%.

Amid the economic expansion, hiring in the labour market has similarly picked up in 3Q 2024. According to the Labour market advance release[2], Singapore saw a sharp uptick in employment numbers alongside a decline in retrenchments. Hiring in 3Q 2024 more than doubled, rising by 24,100 compared to 16,000 in 1H 2024.

Retrenchment numbers in the first nine months of 2024 has declined by 17.3% to 9,200, compared to the 11,130 in the same period last year. Overall unemployment rate continued to remain at a low of 1.8% in 3Q 2024.

Singapore continued to see easing inflationary pressures in 3Q 2024, falling to 2.2% which is the lowest seen since 2Q 2021. Accommodation inflation has likewise moderated 2.9% in 3Q 2024, a sharp contrast to the peak of 4.9% in 1Q 2023. As inflation eased, Singapore’s real income rebounded in 2024 compared to 2023.

Despite concerns over growing household debt, local borrowers remained largely capable of handling their mortgage repayments in 2024. According to the Monetary Authority of Singapore, this resilience is largely underpinned by a combination of higher wages and robust financial assets.

Moreover, the recent cuts in the Fed interest rate have benefited homeowners with existing mortgages by easing the cost of monthly repayments. This is evident in the decline of the 3-month compounded Singapore Overnight Rate Average (SORA), a key benchmark for home loan pricing, from 3.70% in January to 3.24% in November.

In short, the better-than-expected economic outlook and firm economic fundamentals had bolstered shophouse transaction activities in the four months of 2024. But as we look ahead, the bigger question remains: Is recovery on the horizon for the Singapore 2025 property market?

Singapore’s Strong Foothold in The Region Continues to Inspire Confidence Among Investors Even as Uncertainty Looms in 2025

While Singapore’s economy surpassed expectations in 2024, uncertainties continue to abound in the global economy – which could impact the pace of Singapore’s economic growth in 2025.

Worldwide, concerns about global trade have emerged as president-elect Donald Trump prepares to assume his second term in January 2025. Trump’s incoming administration has already signalled an intent to slap tariffs of up to 25% on China, Canada, and Mexico; this has raised fears of inflation and the possibility of interest rates staying higher for longer.

Consequently, we can expect to see rising protectionism and trade tension, alongside the escalating conflicts in the Middle East and Ukraine. Should all these key themes materialise or worsen, we can certainly expect to see further disruption to global supply chains. This will most definitely drive costs higher and may impede the growth of global trade. Taking these factors into account and barring the materialisation of downside risks, MTI has forecasted Singapore’s economy to grow by 1.0 to 3.0% in 2025.

Even amidst these uncertainties and disruptions, Singapore could still potentially emerge as an early beneficiary of the trade war. Leveraging on our strategic position as a regional safe haven, global companies could be incentivised to relocate their manufacturing supply chains to Singapore.

In brief, ERA remains cautiously optimistic of Singapore’s property market in 2025. Underpinned by firm macroeconomic fundamentals, Singapore will continue to deepen its status as one of Asia’s leading wealth management hub, thus drawing family offices, high-net-worth individuals and multinational companies to establish a firm foothold in the city.

Barring any unforeseen circumstances and assuming interest rates continue to moderate, the 2025 property market could outperform 2024, signalling a potential recovery on the horizon. Taken together, the factors mentioned above are expected to boost buyer confidence, driving demand for real estate. Moreover, future price increases are more likely be driven by genuine buying interest, rather than speculative or foreign demand.

Landed Shophouses Transaction Volume

Chart 1: Transaction volume and transaction value of landed shophouses

Source: URA as of 18 Dec 2024, ERA Research and Market Intelligence

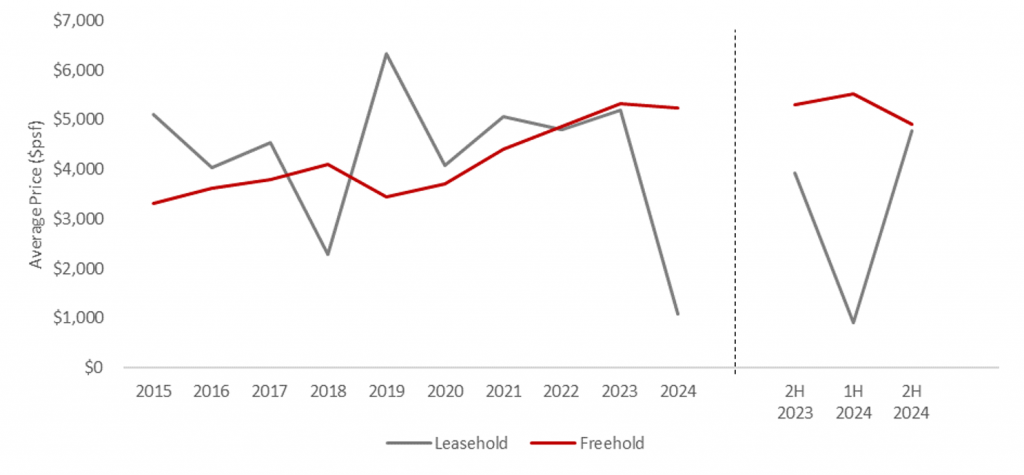

Of the 28 shophouses transacted in 2H 2024, 85.7% (24 units) were of Freehold (FH), inclusive of shophouses with 999-year leasehold tenure.

These FH shophouses are immune to lease decay. Hence, these properties are able ride through market volatility, preserving their value if held over the long term. Institutional investors see this as an asset worth having in their portfolio.

In June 2024, The Rail Mall was divested by Paragon REIT to a private investor for $78.5 million ($744 psf). This led to the average price of 99-year leasehold (99-LH) landed shophouse to be significantly lower in that half-year period.

However, comparing 2H 2023 and 2H 2024, the average price of freehold landed shophouse fell by 7.7%. In contrast, their 99-year leasehold counterparts saw a 21.6% increase. The 99-LH shophouses transacted in 2H 2024 were all in the Central Region and in conservation areas. Moreover, they all had at least 70 years of remaining lease, providing a strong reason for buyers.

Despite having a 99-year lease, shophouses with outstanding locational attributes, conservation status, well-maintained façade and interiors and a long remaining lease would still entice buyers. Hence, we will still expect prices to appreciate in future.

Chart 2: Average PSF prices for landed shophouses

Source: URA as of 18 Dec 2024, ERA Research and Market Intelligence

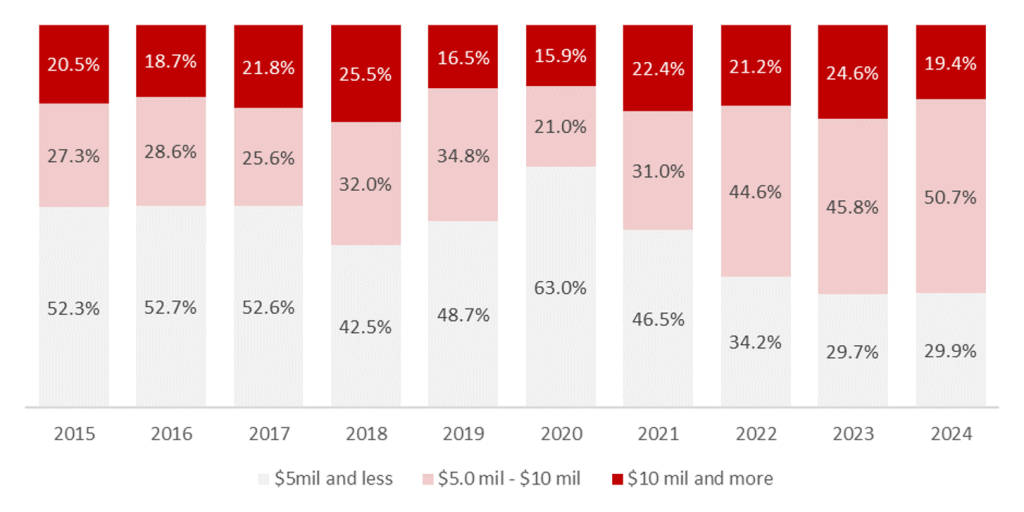

Over the past decade, the price quantum of landed shophouses has generally increased, shown by the proportion of higher valued transactions. In 2024, more than half of the shophouse transactions were between $5 million and $10 million. This could be the sweet spot for a landed shophouse. While there are shophouses transacted under $5 million, they are either not centrally located or have a 99-LH tenure.

Chart 3: Price quantum of landed shophouse in the last ten years

Source: URA as of 18 Dec 2024, ERA Research and Market Intelligence

Singapore shophouse: An asset class that captivates foreign investors

The scarcity of landed shophouses, coupled with Singapore’s status as a wealth hub, have led to these properties being coveted by institutional investors and family offices. Oftentimes, shophouses are used as vehicles to achieve their clients’ goals of capital appreciation and wealth preservation.

In cosmopolitan gateway cities worldwide, investment properties come in the form of modern skyscrapers and trophy assets. Thus, the uniqueness of shophouses can captivate investors seeking something distinct and exceptional.

Hence, with inherently favourable attributes, this slight blip in landed shophouse prices may actually be an opportune time to look out for good deals in the market. Those in prime location and freehold tenures may be undervalued.

Shophouses in Little India

Popularity of Central Region shophouses

Among the 67 shophouses sold in 2024, 63 were located in the Central Region – an area popular for eateries, fitness studios and co-living spaces. As such, owners of Central Region landed shophouses will likely be able to command higher rents on their properties.

District 8 (Little India) was the most popular area for landed shophouse buyers, with 31 transactions in 2024 (46.3%). There could also be opportunities for value buys present in District 8, as ten of these transactions were transacted under $5m.

District 14 (Eunos, Geylang, Paya Lebar) saw seven transactions, while District 01 (Raffles Place, Cecil, Marina, People’s Park) and District 02 (Chinatown, Tanjong Pagar) saw five transactions each in 2024.

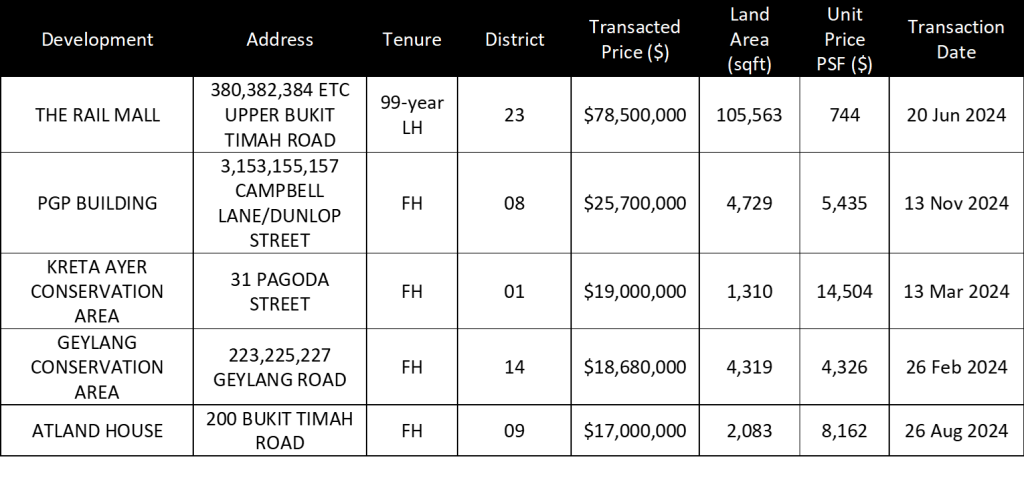

Table 1: Top five shophouse transactions in 2024

Source: URA as of 18 Dec 2024, ERA Research and Market Intelligence

Shophouse demand expected to improve going into 2025

While landed shophouse prices have fallen in 2024, it is unlikely that the market in on a downward trend. While institutional investors and funds may look to offload these properties and recycle their capital, it does not mean that they are looking to sell at a discount. These investors have high holding power, making it unlikely for them to be forced into a sale. A slight decline in prices may provide the opportunity to enter the market.

Moreover, underpinned by firm economic fundamentals and with projected Fed rate cuts on the horizon, we should see more buying interest amid higher projected yields and scope for capital appreciation. Hence, once the impasse is resolved between buyers and sellers’ price expectations, transaction volume will pick up once again.

Shophouses will continue to be sought after by local and international buyers owing to their rarity and heterogeneity. Without the additional stamp duties imposed, investors will continue to keep shophouses as a viable option. Family offices and investors are the most probable buyers for shophouses, especially when the properties are located in the Central Region or have a 999-Leasehold or Freehold tenure.

Owing to the abovementioned factors, ERA forecasts a recovery in landed shophouse transaction volume to be between 70 to 80 units, with the transaction value to be between $650m to $750m.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

[1] Ministry of Trade and Industry, Economic Survey of Singapore Third Quarter 2024

[2] Ministry of Manpower, Labour Market Third Quarter 2024

[3] Singstat, Percent Change In Consumer Price Index (CPI) Over Corresponding Period Of Previous Year, 2019 As Base Year