Tariffs and Property: Can the Residential Market in Singapore Withstand Trump’s Trade Tariffs?

- By Wong Shanting

- 4 mins read

- Commercial, HDB, Private Residential (Non-Landed)

- 8 Apr 2025

The world may be “shook”, but the firm economic fundamentals ensure that the Singapore’s residential market is well-positioned to weather the storm.

On Liberation Day, 2 April 2025, President Donald Trump shook the world by unveiling a higher-than-expected Reciprocal Tariff Policy. In addition to a sweeping 10% baseline trade tariff on all imports, selected countries will face steeper trade tariffs under the policy.

The implementation of this tariff policy holds clear motivations. US manufacturing has declined from 28.4% of global output in 2001 to 17.4% in 2023, while United States goods trade deficit has reached US$1.2 trillion in 2024. Through this move, President Donald Trump aims to level the playing field on pricing, which in turn, could bring manufacturing jobs back to United States and boost domestic consumption.

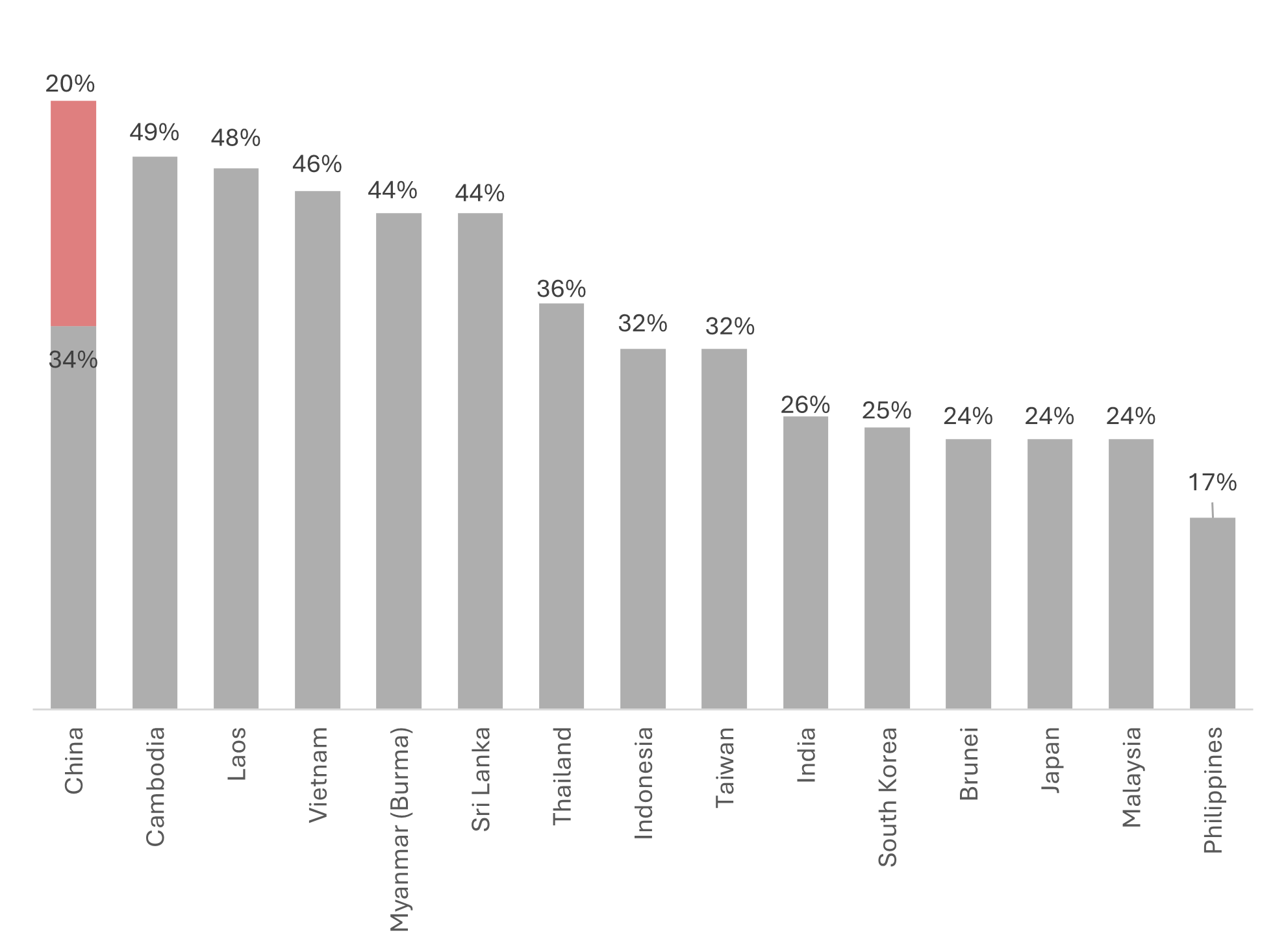

While China, the primary target in the deepening trade war faces a 34% tariff on top of the earlier imposed 20%, several smaller Southeast Asia Markets are also deeply impacted. Cambodia (49%), Laos (48%) and Vietnam (46%) are among the markets that are worst hit by the new tariffs. Despite not on the list of countries affected by higher tariffs, Singapore will still be subjected to the 10% baseline tariffs on our exports to the United States.

Chart 1: Asia Pacific Markets impacted by higher trade Tariffs imposed by United States

\

\

Source: The White House, ERA Research and Market Intelligence

Global stock markets plunge, while the United States could potentially face whiplash from rising inflation and retaliatory tariffs

As the trade war intensifies, uncertainty and fear among investors sent global stock markets plunging on the Monday following the implementation of the Reciprocal Tariff Policy on 5 April 2025. More importantly, these developments have sparked fears of a broader economic downturn.

This aggressive move by the United States could provoke retaliatory tariffs from trade partners, such as China, which almost instantaneously retaliated with a 34% levy on all US imports.

Meanwhile, domestically, rising import costs may fuel inflation and put further pressure on consumers and businesses in United States. Globally, this could spell slower trade demand, which could translate to slower growth.

For now, the market may be gripped by heightened volatility, but what can we expect for the Singapore residential market?

Singapore will face a moderate impact due to the lower baseline 10% trade tariff and has decided against retaliatory tariffs. However, other countries may choose to retaliate and further intensify the ongoing trade war. This heightened volatility will weigh on global economic growth, and on Singapore’s growth, given our heavy reliance on trade.

On a more positive note, residential homebuyers tend to be less speculative, often taking a medium- to long-term view of the market and are more likely to be driven by genuine housing needs.

Although uncertainty persists and the risk of an escalating trade war may dampen near-term demand in the residential market, ERA maintains a cautiously optimistic medium- to long-term outlook. ERA believes that Singapore’s residential sector is non-speculative and will continue to offer growth opportunities for investors with a medium- to long-term perspective, supported by several key fundamentals.

-

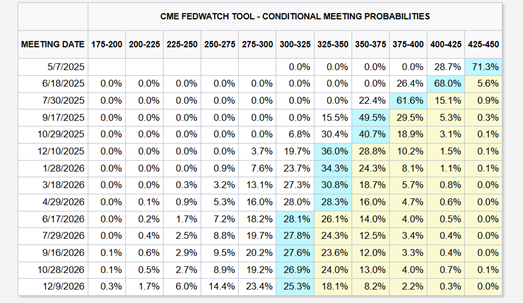

Fed could implement up to four rate cuts due to potentially “higher inflation and slower growth”

Analysts surveyed by CME Group suggest the Federal Reserve could implement up to four rate cuts in 2025, potentially driven by higher inflation and slower growth resulting from trade tariffs. Should this materialise, the federal funds rate could fall to between 3.25% and 3.50%. This could lead to a further moderation in mortgage interest rates which will help ease housing costs.

Chart 2: Analysts view on probabilities of changes to the Fed rates

Source: CME FedWatch

-

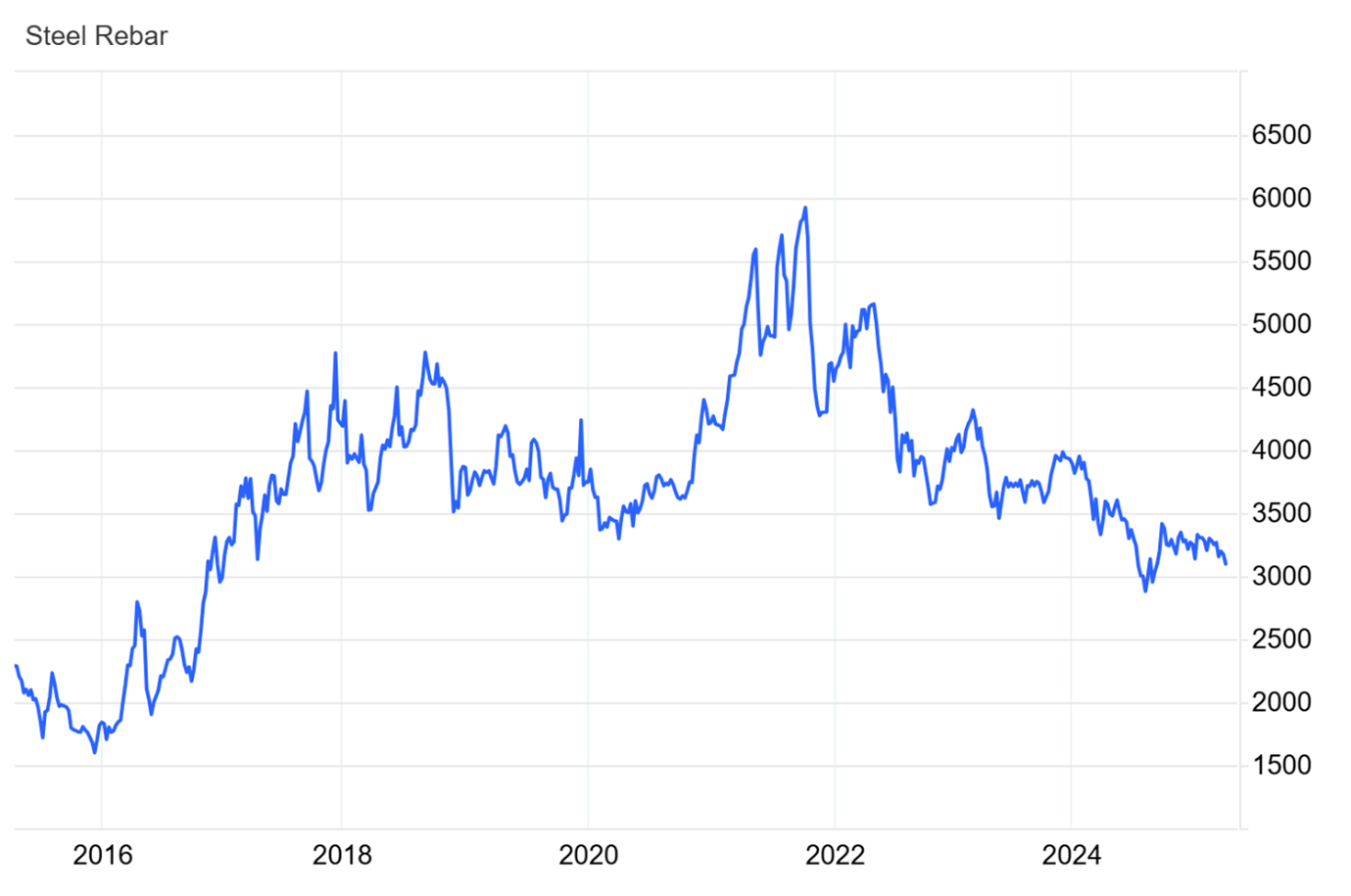

Construction cost may ease with cheaper imports ahead as demand slows

The region may face significant deflationary pressures if China decides to divert its export surpluses and flood the market with cheaper exports. Specific to the construction sector, the slowdown in China’s real estate market has led to weaker domestic demand and softer prices for steel rebar. The 25% US import tariffs are a double whammy on steel demand and could further dampen export demand for Chinese producers.

There could be a risk of a flood of cheaper steel exports in the region, driving down construction material costs. Could this mark the beginning of moderating construction material costs, thereby helping to ease housing prices? Although this might seem plausible, moderating construction costs ahead could have muted impact on housing prices, since Singapore home prices are influenced by a variety of factors including land and labour cost.

Chart 3: Steel Rebar Prices on a steady decline since late 2021 on the back of sluggish demand

Source: tradingeconomics.com

-

Singapore’s safe haven status could continue to attract foreign investments seeking growth in the region, ensuring job opportunities which can support driving housing demand

The imposition of trade tariffs is set to effectively curb the ‘China Plus One’ strategy, which is widely adopted by companies to reduce reliance on China and mitigate the impact of the trade war. Consequentially, many of the regional low-cost manufacturing hubs could face challenges due to higher trade tariffs.

Singapore, however, maintained a balanced and mutually beneficial partnership with the United States, as reinforced by the U.S. goods trade surplus with Singapore, which stood at US$2.8 billion in 2024. This underscores our position as a trusted trade ally and has likely shielded us from harsher tariff measures.

Investors in the region seeking safe havens and growth could look to Singapore, drawn by it’s relative stability, transparent and open economy. This could drive a steady influx of Foreign Direct Investment (FDI) which is instrumental in supporting job opportunities and contribute to the overall economic development of Singapore. This in turn could support demand for residential and commercial properties in Singapore. Singapore’s status as a financial hub and its robust legal framework further enhances its attractiveness in times of economic uncertainty.

Chart 4: Steady increase in Foreign Direct Investment

Source: Singstat, ERA Research and Market Intelligence

-

Singapore’s diversified economy and extensive multilateral trade partners can help mitigate economic shocks

Singapore’s diversified economy and broad network of trade partners will mitigate the impact of individual countries’ trade tariffs. Till date, Singapore has 27 free trade agreements and will continue to pursue and uphold open, fair, and free trade among like-minded countries.

-

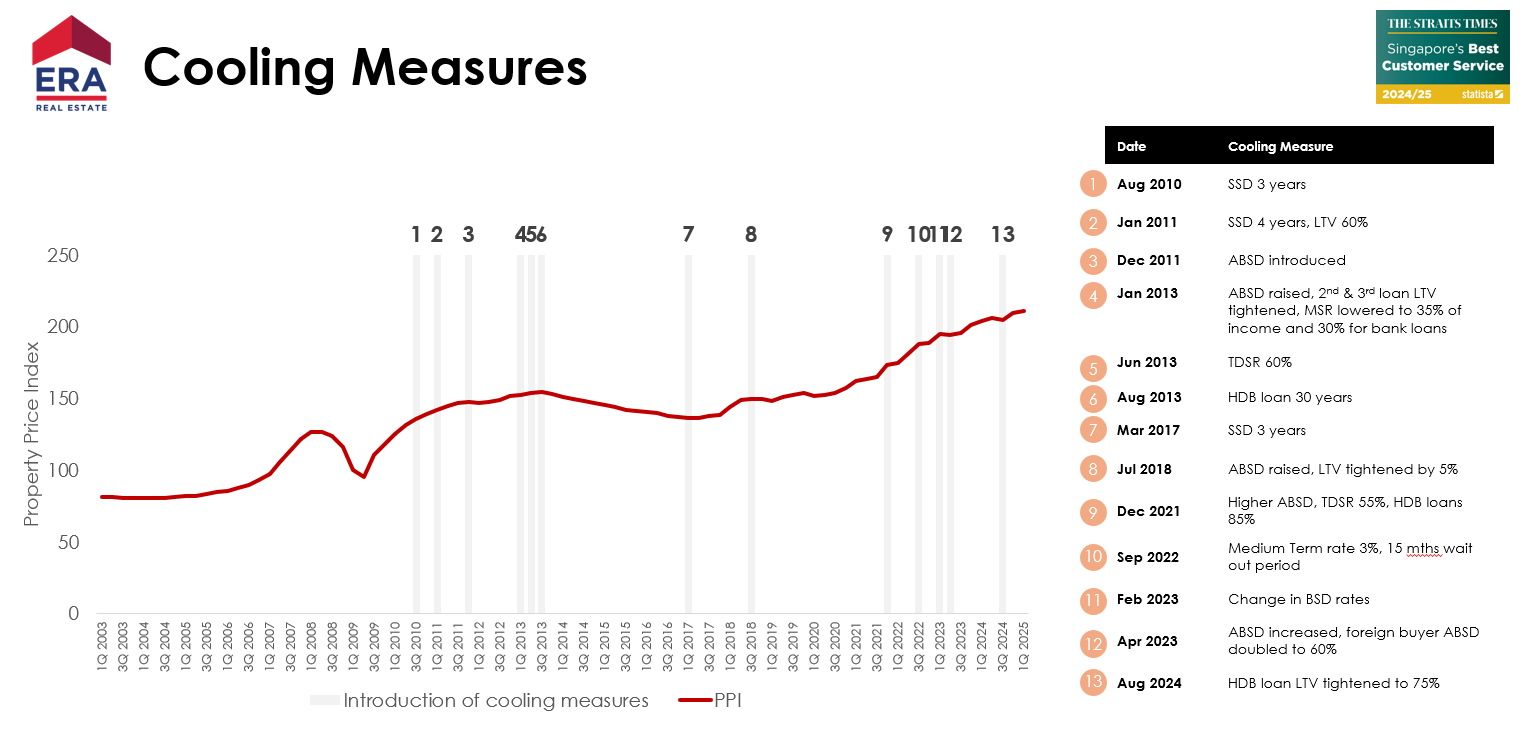

Proactive cooling measures in the residential market provide flexibility to navigate against external shocks

Between 2010 and 2024, the Singapore government introduced 13 rounds of cooling measures aimed at maintaining a stable residential market and ensuring sustainable price growth.

These measures included the significant 60% Additional Buyer’s Stamp Duty (ABSD) implemented in April 2023, targeting speculative investment from foreign buyers. Additionally, the higher Additional Buyer’s Stamp Duty (ABSD) on second homes is intended to discourage accumulation of multiple properties, helping to moderate home price growth and maintain market stability. All of this contributes to sustaining the intrinsic value of residential properties in Singapore.

Chart 5: Cooling Measures for Singapore Residential Market

Source: URA, HDB, MND, ERA Research and Market Intelligence

In conclusion

There you have it – and this is why ERA maintains a positive medium- to long-term outlook for Singapore’s residential market, even in the face of global headwinds.

Much of the groundwork has been laid by our government prior. This includes establishing extensive free trade agreements, developing sophisticated infrastructure, and nurturing a highly educated workforce. These efforts form a firm foundation that continues to attract sustained foreign investment, a key driver of Singapore’s long-term economic growth, as well as creating job opportunities.

When it comes to housing, the government takes a pragmatic approach to keep pace with demand, while being careful to discourage excessive accumulation of property assets for speculative purposes. Instead, the focus remains deeply rooted in ensuring that homes stay accessible for Singaporeans through sustainable price growth. Furthermore, the multiple rounds of cooling measures offer plenty of room for the government to respond swiftly should the property market face external shock.

In summary, Singapore’s property market is built on a foundation of resilience, foresight, and prudent governance. ERA believes that with sustained policy support and strong demand drivers, Singapore’s residential market will continue to present resilient growth potential and long-term value for both homeowners and investors.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.